VOL. 18, ISSUE NO. 9 | December 2025

Focus

Africa is sometimes nicknamed the “Mother Continent” as it’s the oldest inhabited continent on Earth. It is the second largest continent after Asia covering about one-fifth of the total land surface of the Earth. The continent is bounded on the west by the Atlantic Ocean, on the north by the Mediterranean Sea, on the east by the Red Sea and the Indian Ocean to the south.

Africa’s total land area is approximately 11,724,000 square miles (30,365,000 square km), and the continent measures about 5,000 miles (8,000 km) from north to south and about 4,600 miles (7,400 km) from east to west. Its northern extremity is Al-Ghīrān Point, near Al-Abyad Point (Cape Blanc), Tunisia; its southern extremity is Cape Agulhas, South Africa; its farthest point east is Xaafuun (Hafun) Point, near Cape Gwardafuy (Guardafui), Somalia; and its western extremity is Almadi Point (Pointe des Almadies), on Cape Verde (Cap Vert), Senegal. In the northeast, Africa was joined to Asia by the Sinai Peninsula until the construction of the Suez Canal. Paradoxically, the coastline of Africa—18,950 miles (30,500 km) in length—is shorter than that of Europe, because there are few inlets and few large bays or gulfs.

Off the coasts of Africa are a number of islands associated with the continent. Of these Madagascar, one of the largest islands in the world, is the most significant. Oth-er, smaller islands include the Seychelles, Socotra, and other islands to the east; the Comoros, Mauritius, Réunion, and other islands to the southeast; Ascension, St. Helena, and Tristan da Cunha to the southwest; Cape Verde, the Bijagós Islands, Bioko, and São Tomé and Príncipe to the west; and the Azores and the Madeira and Canary islands to the northwest.

The origin of the name “Africa” is greatly disputed by scholars. Most believe it stems from words used by the Phoenicians, Greeks, and Romans. Important words include the Egyptian word Afru-ika, meaning “Motherland”; the Greek word aphrike, meaning “without cold”; and the Latin word aprica, meaning “sunny.”

Today, Africa is home to more countries than any other continent in the world. These countries are: Morocco, Algeria, Tunisia, Libya, Egypt, Sudan, South Sudan, Chad, Niger, Mali, Mauritania, Senegal, The Gambia, Guinea-Bissau, Guinea, Sierra Leone, Liberia, Côte d’Ivoire, Ghana, Burkina Faso, Togo, Benin, Nigeria, Cameroon, Central Africa Republic, Equatorial Guinea, Gabon, Congo, Democratic Republic of the Congo, Angola, Namibia, Botswana, South Africa, Lesotho, Eswatini, Mozambique, Zimbabwe, Zambia, Malawi, Tanzania, Rwanda, Burundi, Uganda, Kenya, Somalia, Ethiopia, Djibouti, Eritrea and the island countries of Cape Verde, Madagascar, Mauritius, Seychelles, and Comoros.

Cultural Geography of Africa

The African continent has a unique place in human history. Widely believed to be the “cradle of humankind,” Africa is the only continent with fossil evidence of human beings (Homo sapiens) and their ancestors through each key stage of human evolution.These include the Australopithecines, our earliest ancestors; Homo habilis, our tool-making ancestors; and Homo erectus, a more robust and advanced relative to Homo habilis that was able to walk upright.

These ancestors were the first to develop stone tools, to move out of trees and walk upright, and, most importantly, to explore and migrate.While fossils of Australopithecines and Homo habilis have only been found in Africa, examples of Homo erectus have been found in the Far East, and their tools have been excavated throughout Asia and Europe. This evidence supports the idea that the species of Homo erectus that originated in Africa was the first to successfully migrate and populate the rest of the world.

This human movement, or migration, plays a key role in the cultural landscape of Africa. Geographers are especially interested in migration as it relates to the way goods, services, social and cultural practices, and knowledge are spread throughout the world.

Migration Patterns From Africa & Their Impact On Skill Development & Economy

Other than the two pre-historic migrations, the Bantu Migration and the African slave trade, helped define the cultural geography of the continent.

The Bantu Migration was a massive migration of people across Africa about 2,000 years ago, that occurred since the first human ancestors left Africa more than a million years ago. Lasting for 1,500 years, the Bantu Migration involved the movement of people whose language belonged to the Kongo-Niger language group. The common Kongo-Niger word for human being is Bantu.

The exchange of skills and ideas as a result of this migration, greatly advanced Africa’s cultural landscape, especially in the eastern, central,

and southern regions of the continent. Today, most of the population living in these regions are descendants of Bantu migrants or from mixed Bantu-indigenous origins.

Another massive human migration in Africa was the African slave trade. Between the 15th and 19th centuries, more than 15 million Africans were transported across the Atlantic Ocean to be sold as slaves in North and South America. Millions of slaves were also transported within the continent, usually from Central Africa and Madagascar to North Africa and the European colony of South Africa.

The impact of slavery on Africa are widespread and diverse. Computerized calculations have projected that if there had been no slave

trade, the population of Africa would have been 50 million instead of 25 million in 1850. While Africans suffered greatly during the slave trade, their influence on the rest of the world expanded. Slave populations in North and South America made tremendous economic, political, and cultural contributions to the societies that enslaved them.

The standard of living in North and South America—built on agriculture, industry, communication, and transportation—would be much lower if it weren’t for the hard, forced labour of African slaves. Furthermore, many of the Western Hemisphere’s cultural practices, especially in music, food and religion are a hybrid of African and local customs.

Contemporary Cultures

Contemporary Africa is incredibly diverse, incorporating hundreds of native languages and indigenous groups.

The majority of these groups blend traditional customs and beliefs with modern societal practices and conveniences. Three groups that demonstrate this are the Maasai, Tuareg, and Bambuti.

Political Geography

frica’s history and development have been shaped by its political geography.

Political geography is the internal and external relationships between various governments, citizens, and territories.

Historical African Trade Destinations

The great kingdoms of West Africa developed between the 9th and 16th centuries.

- The Kingdom of Ghana (Ghana Empire) became a powerful empire through its gold trade, which reached the rest of Africa and parts of Europe. Ghanaian kings controlled gold-mining operations and implemented a system of taxation that solidified their control of the region for about 400 years.

- The Kingdom of Mali (Mali Empire) expanded the Kingdom of Ghana’s trade operations to include trade in salt and copper.The Kingdom of Mali’s great wealth contributed to the creation of learning centers where Muslim scholars from around the world came to study. These centers added to Africa’s cultural and academic enrichment.

- The Kingdom of Songhai (Songhai Empire) combined the powerful forces of Islam, commercial trade and scholarship.Songhai kings expanded trade routes, set up a new system of laws, expanded the military, and encouraged scholarship to unify and stabilize their empire. Their economic and social power was anchored by the Islamic faith.

Colonization of Africa

Colonization dramatically changed Africa. From the 1880s to the 1900s, almost all of Africa was exploited and colonized, a period known as the “Scramble for Africa.” European powers saw Africa as a source of raw materials and a markets for manufactured goods.Important European colonizers included Britain, France, Germany, Belgium and Italy.

The legacy of colonialism haunts Africa even today. Colonialism forced environmental, political, social and religious changes in Africa. Natural resources, including diamonds and gold, were over-exploited. European business owners benefitted from trade in these natural resources, while Africans laboured in poor conditions without adequate pay.

European powers drew new political borders that divided established governments and cultural groups.These new boundaries also forced different cultural groups to live together. This restructuring process brought out cultural tensions, causing deep ethnic conflict that continues even today. In Africa, Islam and Christianity grew with colonialism. Christianity spread through the work of European missionaries, while Islam consolidated its power in certain undisturbed regions and urban centers.

World War II (1939-1945) empowered Africans to confront colonial rule. Africans were inspired by their service in the Allies’ forces and by the Allies’ commitment to the rights

of self-government. Their belief in the possibility of independence was further supported by the independence of India and Pakistan in 1947.

Mahatma Gandhi, an Indian independence leader who began his career in South Africa, said: “I venture to think that the Allied declaration that the Allies are fighting to make the world safe for the freedom of the individual and for democracy sounds hollow so long as India, and for that matter Africa, are exploited by Great Britain.”

By 1966, all but six African countries were independent nation-states.Funding from the Soviet Union and independent African states was integral to the success of Africa’s in-dependence movements. Regions in Africa continue to fight for their political independence. Western Sahara, for instance, has been under Moroccan control since 1979. The United Nations is currently sponsoring talks between Morocco and a Western Sahara rebel group called the Polisario Front, which supports independence.

The whole of Africa can be considered as a vast plateau rising steeply from narrow coastal strips and consisting of ancient crystalline rocks.The plateau’s surface is higher in the southeast and tilts downward toward the northeast and is divided into a southeastern and a northwestern portion. The northwestern part, which includes the Sahara Desert, is known as the Maghrib, with two mountainous regions—the Atlas Mountains in northwestern Africa, which are believed to be part of a system that extends into southern Europe, and the Ahaggar (Hoggar) Mountains in the Sahara.The southeastern part of the plateau includes the Ethiopian Plateau,the East African Plateau, and—in eastern South Africa, where the plateau edge falls downward in a scarp—the Drakensberg range. One of the most remarkable features in the geologic structure of Africa is the East African Rift System, which lies between 30° and 40° E. The rift itself begins northeast of the continent’s limits and extends southward from the Eritrean Red Sea coast to the Zambezi River basin.

Rich Mineral Resources

Africa contains an enormous wealth of mineral resources, including some of the world's largest reserves of fossil fuels, metallic ores, gems and precious metals. This richness is matched by a great diversity of biological resources that includes the intensely lush equatorial rainforests of Central Africa and the world-famous populations of wildlife of the eastern and southern portions of the continent.

Although agriculture (primarily subsistence) still dominates, the exploitation of these resources became the most significant economic activity in Africa in the 20th century.

Climatic and other factors have exerted considerable influence on the patterns of human settlement in Africa. While some areas appear to have been inhabited more or less continuously since the dawn of humanity, enormous regions—notably the desert areas of northern and southwestern Africa are largely unoccupied. So despite Africa being the second largest continent, it has only about 10 percent of the world’s population and can be said to be underpopulated. Other than the original ‘Black’ inhabitants, there has been major immigrations from both Asia and Europe. Of all foreign settlements in Africa, that of the Arabs has made the greatest impact. The Islamic religion, which the Arabs carried with them, spread from North Africa into many areas south of the Sahara, so major populations in western Africa follow Islam.

Economy of Africa

Africa’s economic performance improved in 2024, but growth remains fragile amidst multiple shocks and rising global uncertainty. Average real gross domestic product (GDP) growth picked up marginally from 3.0 percent in 2023 to 3.3 percent in 2024, buoyed by strong government spending and private consumption.The growth uptick in 2024 was evident in 29 of 54 African countries.In addition, 10 African countries, including Angola, Ghana, Niger, and Uganda, saw growth increases of more than 1.0 percentage points from 2023 to 2024. However, this slight improvement was overshadowed by persistent inflationary pressures, currency depreciations and high debt service costs. Deepening geopolitical fragmentation, regional conflicts, and rising global uncertainty spurred by emerging trade policies in several countries further cloud the outlook for the short and medium terms.

Africa’s real GDP per capita growth is estimated at 0.9 percent in 2024, up from 0.7 per-cent in 2023. Even so, this was 0.5 percentage points lower than that for Latin America and the Caribbean, and 2.9 percentage points lower than that of Asia, the best performing region. Africa’s real GDP per capita growth is projected at 1.5 percent in 2025 and could reach 1.7 percent in 2026. But relative to the February 2025 projections, these represent downgrades of 0.3 and 0.5 percentage points, respectively.

The economic performance and prospects conceal cross-regional variations as the tariff shock and its attendant uncertainty could have asymmetric effects on countries and regions, depending on the strength of existing macro economic buffers and degree of integration into global trade.

Central African Economy

Real GDP growth for this region averaged 4.0 percent in 2024, a decline from 4.4 percent the previous year. It is projected to fall to 3.2 percent in 2025 and 3.9 percent in 2026, below the 2025 MEO forecast by 0.7 and 0.2 percentage points for 2025 and 2026, respectively. The downward revision for the region in 2025 is broad-based across all countries. In addition to the trade uncertainty, growth in the region is also being hampered by the ongoing conflict in the eastern part of the Democratic Republic of Congo, and that of Equatorial Guinea by the decline in hydrocarbon production and exports.

East African Economy

Growth in this region is projected to accelerate from 4.3 percent in 2024 to 5.9 percent in 2025 and 2026.Compared with the projection of 5.3 percent in the 2025 MEO, growth for the region is revised upward by 0.6 percentage point in 2025 and downward by 0.2 percentage points in 2026. This reflects resilience in Ethiopia, Rwanda, Djibouti, Uganda, and Tanzania, all expected to attain an average growth rate of 6 percent or higher in 2025–26, supported by continued public investments to deepen domestic value chains in the agriculture sector and domestic energy infrastructure.

North African Economy

Following the moderate growth rate of 2.6 percent in 2024, the region is projected to grow by 3.6 percent in 2025 and 3.9 percent in 2026. But these forecasts reflect downward revisions of 0.2 percentage points each from the 2025 MEO projections for both years. Among the region’s economies, the forecast in Egypt is revised downwards respectively, by 0.3 percentage point in 2025 and 0.5 percentage points in 2026; in Libya, it is downgraded by 0.6 and 0.2 percentage points for the same years. These downgrades are mainly due to a potential decline in export revenues.

Southern African Economy

Growth in the region is estimated at 1.9 percent in 2024 and is projected to grow by 2.2 percent in 2025 and 2.5 percent the following year.Compared to the 2025 MEO, these forecasts represent 0.9 and 0.6 percentage point downgrades, respectively. Despite the low regional growth outlook, a few countries (eSwatini, Zambia, and Zimbabwe) could grow by 6 percent or higher in 2025. Growth in South Africa, the United States’ largest trading partner in Africa, is projected at 0.8 percent in 2025 before recovering slightly to 1.2 percent in 2026. The country’s ongoing efforts to address the global trade shocks and implement projected structural reforms could improve South Africa’s medium-term growth outlook.

Real GDP growth in the region, estimated at 4.5 percent in 2024, could decline slightly to 4.3 percent in 2025–26, 0.3 percentage points and 0.2 percentage points lower than the 2025 MEO forecasts. Except for Ghana, Nigeria and Sierra Leone, all countries are expected to grow by 5 percent or higher in 2025. The shift in demand from Nigeria’s trading partners, including the United States of America and China, coupled with global supply chain disruptions and increased volatility in financial markets, will further cloud its growth outlook, projected at 3.2 percent in 2025 and 3.1 percent in 2026. This represents a downward revision of 0.3 and 0.5 percentage points from the 2025 MEO projections

Future Potential of African Economy

Africa has the potential to become the world’s growth pole, but this depends on countries undertaking deep reforms and transforming their resources into development benefits. With the continent accounting for an estimated 13 of the world’s top 20 fastest growing economies in 2025, prospects for a resurgence in Africa could not be more favourable. In several countries, structural policies and macroeconomic stability have been gaining ground, underpinning Africa’s resilience amidst an increasingly

difficult global economic environment. There is evidence of productivity gains in manufacturing, estimated to be 3.8 times the economy wide productivity.

Higher productivity is important for the competitiveness of domestic economies. Countries undertaking strategic investments in key areas— infrastructure and human capital— to speed up structural transformation and economic diversification will reap the benefits of these actions.

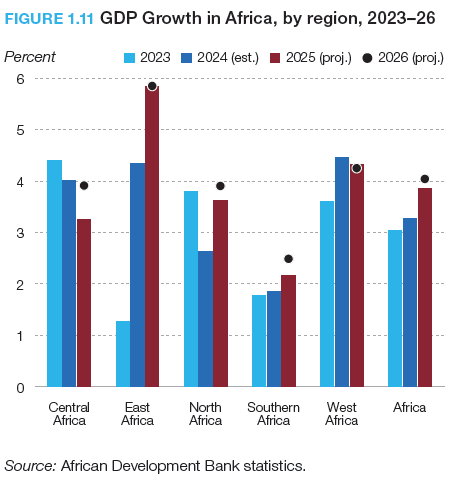

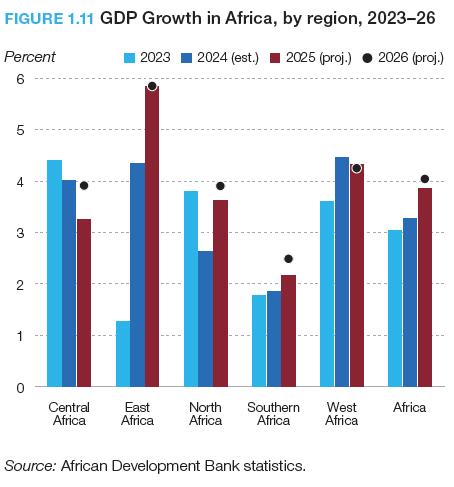

Differences in current and projected growth rates across Africa’s regions (figure 1.11) and country groupings (figure 1.12) reflect these efforts.

The tariff shock and its attendant uncertainty could have an asymmetric impact on regions and countries, depending on the strength of existing macroeconomic buffers and degree of integration into global trade. Economic performance and prospects thus mask cross-regional variations.Real GDP growth in Central Africa

averaged 4.0 percent in 2024, a decline from 4.4 percent the previous year. It is projected to fall to 3.2 percent in 2025 and 3.9 percent in 2026, below the February MEO forecast by 0.7 percentage points in 2025 and 0.2 in 2026. The broadbased downgrade for the region in 2025, across all countries, largely reflects deceleration in oil and mining production and restrained public investment due to growing uncertainty and weak prospects for global trade. Real GDP in the Democratic Republic of Congo is projected to

decelerate to 4.8 percent in 2025, from the estimated 6.2 percent in 2024. The outlook is subject to significant headwinds, including the raging conflict in the eastern part of the coun-try and global uncertainty, which could weaken demand for its mineral exports. Economic performance in Equatorial Guinea continues to weigh on the region. Its real GDP is projected to contract by 4 percent in 2025, worse than the contraction of 2 percent projected in the February MEO. The projected recession reflects limited economic

diversification to compensate for losses resulting from a decline in hydrocarbon production and exports.

East Africa, long established as Africa’s fastest growing region, is an embodiment of commit-ment to reforms and public infrastructure development to catalyze private sector investment. In 2024, the region’s real GDP growth averaged an estimated 4.3 percent, and is projected to expand further to 5.9 percent in 2025 and 2026 (see figure 1.11).

Compared with the projection of 5.3 percent in the February 2025 MEO, growth for the region is revised upward by 0.6 percentage point in 2025 but slightly downward by 0.2 percentage points in 2026. This reflects the resilience of growth in

Ethiopia, Djibouti, Rwanda, Uganda and Tanzania, all expected to grow by an average rate of 6 per¬cent or higher in 2025–26, supported by contin¬ued public investments to deepen domestic value chains in agriculture and energy infrastructure.

East Africa’s resilience to shocks may be explained by the fact that the region is home to some of the most diversified economies in Africa with a growing share of manufactured goods in intraregional trade

and relatively strong regional trade penetration. For instance, in 2023, the regional bloc’s total trade grew by 13.1 percent to $12.1 billion with the percentage share of intra-EAC trade to EAC total trade increasing to 15 percent.11 Rwanda’s projected growth rate of 7.8 percent in 2025 is not atypical and sustains a strong post-Covid-19 recovery. It can be attributed to continued strong public expenditure on mega projects as well as improvements in tourism infra¬structure and investment to enhance technology innovation and mobility. Growth in Ethiopia is also underpinned by massive public and private invest-ment. The country’s projected growth of 8 percent in 2025 is 1.6 percentage points higher than fore¬cast in the February 2025 MEO. The country has undertaken important financial sector reforms, allowing for some degree of exchange rate flexibil¬ity and assigning a greater role to the private sector in the economy. These measures have been com¬plemented by efforts to boost trade and tourism and modernization strategies to enhance produc¬tivity in agriculture and agro-processing to boost exports of high-value crops. Ethiopia is one of few countries in Africa to post growth during Covid-19, signifying its growing resilience to shocks. Perfor-mance of other countries in East Africa shows the benefits of public sector–facilitated private invest¬ment to build economic resilience.

In North Africa, following moderate growth rate of 2.6 percent in 2024, the region is projected to grow by 3.6 percent in 2025 and 3.9 percent in 2026. However, these forecasts reflect downward revisions of 0.2 percentage points apiece from the February MEO projections for both years. Among the region’s economies, the forecast in Egypt is revised down, by 0.3 percentage points in 2025 and 0.5 in 2026; in Libya, it is downgraded by 0.6 and 0.2 percentage points. These downgrades are mainly due to a potential decline in export revenues. Despite the downgrades, Libya’s projected growth of 6.9 percent in 2025 will reverse the economy’s contraction of 3.1 percent in 2024, thereby contrib¬uting to North Africa’s average growth rate for this year. Its growth rate often tracks dynamics in its prolonged conflict and prospects in the oil sector. Elsewhere in the region, growth will remain below 5 percent. With increasing global uncertainty, slower growth in key tourism source markets such as the European Union and China and flagging global demand could interrupt the recovery in the region.

Southern Africa emerged strongly from the impact of a devastating drought in 2024, but the recovery is likely to be disrupted by heightened uncertainty due to trade shocks. Fiscal risks in South Africa could further weigh on the region’s growth outlook in 2025 and beyond. Growth in the region is forecast at 2.2 percent in 2025 and 2.5 percent in 2026, from an estimated 1.9 percent in 2024. This marks the first time since 2021 that growth has exceeded 2 percent. Compared with the February MEO forecasts, these

growth rates represent 0.9 and 0.6 percentage point down¬grades for the same periods. Despite the low regional growth outlook, projections for eSwatini, Zambia, and Zimbabwe point to sustained recovery, and their real GDPs could expand by 6 percent or more in 2025. Favorable rainfall in 2025 is expected to aid a strong recovery in agriculture output and improve energy production from Lake Kariba, a key source of hydropower generation shared by Zambia and Zimbabwe. Zambia could also benefit from investment in exploration and commissioning of new mines for copper and nickel production. Its economy is projected to grow by 6.2 percent in 2025, unchanged from the MEO forecast, reflecting the benefits of sustained reform efforts and debt restructuring. In Zimbabwe, growth is projected to be at 6 percent in 2025, 0.7 percentage point higher than the February 2025 MEO forecast.Tariff-induced uncertainty will have the largest adverse growth impact in Botswana and Lesotho in 2025– 26. The former has struggled to rekindle its growth as the price of diamonds has suffered from multiple global shocks, and current uncer¬tainty could further depress them. For the latter, the tariffs will have a direct impact on trade in apparel and other exports to the United States, which accounts for 45 percent of its exports. While improved energy production had provided a respite to South Africa’s struggling economy, fiscal risks could mount due to the suspended increase in the rate of value added

tax which could affect revenue and budget execution. Its economy is projected to grow by 0.8 percent in the medium term, half the rate projected in the MEO. Growth could recover to 1.2 percent in 2026 if the country navigates current fiscal challenges and trade disruptions.

In West Africa, real GDP growth is estimated at 4.5 percent in 2024 but could decline to an aver¬age of 4.3 percent in 2025–26, 0.3 percentage points and 0.2 percentage points lower than the February 2025 MEO forecasts. With the excep¬tions of Ghana, Nigeria, and Sierra Leone, all other countries are expected to grow by 5 percent or higher in 2025, thanks to full commencement of oil and gas production (in Senegal and Niger), and combined effects

of strong domestic-demand– sustained public and private investments—and increased value addition in key agricultural prod¬ucts (in Côte d’Ivoire, Gambia, Mali, and Togo). Senegal’s growth is gaining speed, estimated at 6.9 percent in 2024, after a slowdown in 2022 and 2023, and the country will retain its position as Africa’s fastest-growing economy. Real GDP growth is projected at 10.3 percent in 2025, down just 0.2 percentage points from the February 2025 MEO forecast. Projected growth in Senegal will be buoyed by the commencement of oil and gas exports from the Greater Tortue Ahmeyim LNG project. Niger is also benefitting from ramping up oil production and increased financing of infra¬structure. These efforts will steady Niger’s growth rate

at 7 percent. Other countries with growth rates exceeding 5 percent include Benin (6.6 per¬cent), Côte d’Ivoire (6.3 percent), and Gambia (5.8 percent), driven by strong domestic demand, sustained investment, and increased value addi-tion of key agricultural products. The shift in demand in Nigeria’s trading partners, including the United States and China, coupled with global supply chain disruptions and increased volatility in financial markets, could further affect the country’s growth outlook, which is projected at 3.2 percent in 2025 and 3.1 percent in 2026. This represents a downward revision of 0.3 and 0.5 percentage points from the February 2025 MEO projections

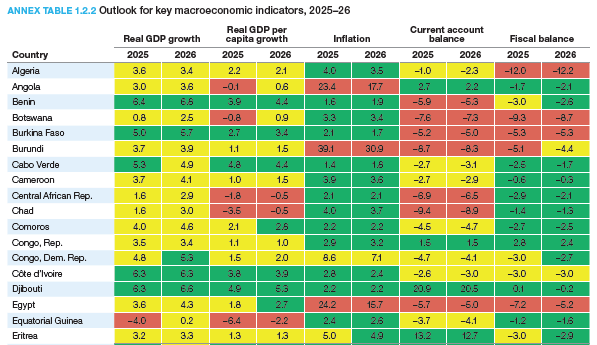

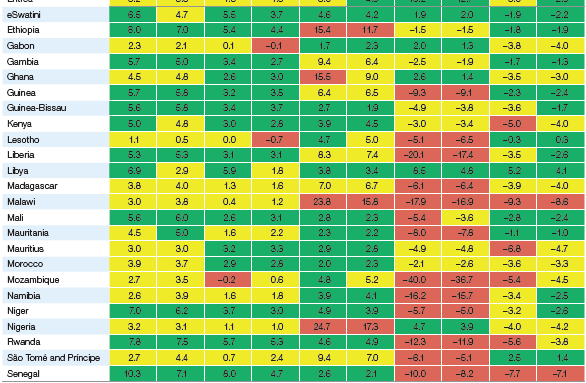

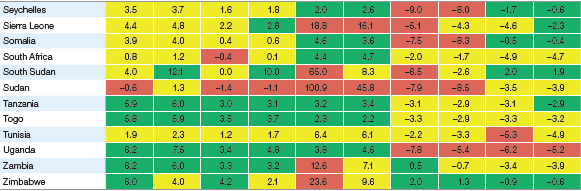

Note: GDP growth and inflation are in percent, while the current account balance and fiscal balance are in percent of GDP. Countries are categorized according to three criteria: “green” for good performance, “yellow” for average performance, and “red” for poor performance. Real GDP growth of 5 percent or higher is colored green, 0–4.99 percent is colored yellow, and negative is colored red. Real GDP per capita of 2.6 percent or higher is colored green, 0–2.59 percent is colored yellow, and negative is colored red. Inflation rates below 5 percent are colored green, 5–9.9 percent are colored yellow, and double-digit inflation is colored red. Current account surplus is colored green, deficits below 5 percent are colored yellow, and above 5 percent are colored red.

Budget deficits below 3 percent are colored green, 3–5 percent are colored yellow, and above 5 percent are colored red. Source:AfDB statistics.

???? Image 18: focus_p30_img0.jpg

Replace REPLACE_WITH_CDN_URL_18

???? Image 19: focus_p31_img0.jpg

Replace REPLACE_WITH_CDN_URL_19

© Copyright , All rights reserved. Design by Andreal