VOL. 18, ISSUE NO. 8 | November 2025

Focus

Effective Strategy for Growth in the Engineering Sector

Engineering is the largest industrial sector in India. The country’s engineering sector comprises majorly manufacturing iron, steel, related products, non-ferrous metals, industrial machinery, automobiles, auto components, and other engineering products.

India’s engineering sector is witnessing a remarkable growth over the last few years, driven by increased investment in all important verticals. India exports engineering products to global regions like ASEAN, North-East Asia, Africa, EU, North America, CIS, Latin America, South Asia, Africa, Middle East, West Asia, etc. The engineering sector, being closely associated with the manufacturing and infrastructure sectors, is of huge strategic importance to India’s economy. The Government’s ‘Vision Plan 2030’ proposed an action plan to become a manufacturing and export hub for construction equipment and propel the development of world-class infrastructure in the country.

Subcontracting work to qualified partners continues to be an effective strategy for achieving growth in the engineering industry. Buyers and suppliers from all industry sectors need subcontracting partners to exchange and maintain international benchmark capabilities to remain competitive in a global market.

Subcontracting helps subcontractors to identify latest and potential projects of major organisations of India in every vertical of the industry to get first-hand information to evaluate every chance to get associated to take up projects. Subcontracting facilitates to engage works with prime contractors on workable rates & terms. The engineering sector is an important component of the broader manufacturing sector. The share of engineering products in overall manufacturing output is quite significant. It is also a highly organized sector dominated by large players employing over four million skilled and semi-skilled labourers.

Subcontracting facilitates growth of all related verticals of engineering sector. In the upcoming days, this sector is likely to witness a major transformation with respect to demand growth, R&D and market operations. Future investments will benefit from strong demand fundamentals, policy support and increasing government focus on engineering sector.

Subcontracting facilitates growth of all related verticals of engineering sector.

PRODUCTS

Industry Supplies & Services

India’s industrial supplies and service sector is vast, providing a wide array of products like machinery, tools, and safety equipment, as well as services such as maintenance, installation, and specialized support for various industries like manufacturing, oil and gas, and food processing. Key online platforms like IndiaMART and Tradeindia act as marketplaces connecting buyers and sellers for products like pumps, lubricants, and welding supplies.

Types of industrial supplies

-

Machinery and equipment

Includes a wide range of products such as air compressors, welding machines, various types of pumps, and machinery for food processing and garment printing.

-

Tools and hardware

Suppliers offer everything from power and hand tools to specialized items like torque wrenches and testing and measuring instruments.

-

Safety and protective gear

Includes safety equipment like safety gloves, helmets fire-fighting systems and personal protective equipment (PPE).

-

Chemicals and lubricants

A broad selection of chemicals, oils, greases and lubricants are available for various industrial and automotive applications.

-

Fasteners and hardware

Wide range of products such as nuts, bolts, screws, washers, and other hardware components.

-

Electrical supplies

Include electrical products like cables, wires, switchgears, and lighting solutions.

KEY SERVICES PROVIDED

-

Maintenance and repair

Companies provide essential services such as equipment maintenance, repair, and calibration.

-

Engineering and design

Some companies offer engineering and design services to support custom solutions for specific industrial needs.

-

Safety and protective gear

Specialized consulting services are available for various areas, including energy efficiency, process optimization and safety management.

-

Installation and commissioning

Companies offer services for the installation and commissioning of new equipment and systems.

-

Supply chain and logistics

Services to manage the supply chain, from raw material sourcing to final delivery are also a key offering.

LOCATING SUPPLIERS

-

Online marketplaces

Platforms like IndiaMART and Tradeindia serve as major online marketplaces for a wide range of industrial supplies and services..

-

Industry-specific websites

Dedicated online stores, such as Industry Buying and Industrykart, specialize in industrial and business supplies.

-

Industry directories

General directories like Justdial can help in finding local suppliers and service providers.

LOCATING SUPPLIERS

The Indian automotive industry has seen significant growth and is currently valued at over US$ 238 billion.. It contributes approximately 6.8% to India’s GDP and 14-15% to the GST. The industry is a major player in global markets, particularly in segments like Passenger Cars, Utility Vehicles, Vans and two Wheelers is expected to reach US$ 300 billion by 2026. The sector is also expected to become the third largest in the world by 2030.

India’s auto component industry is also an important sector driving macroeconomic growth and employment. The industry comprises players of all sizes, from large corporations to micro entities, spread across clusters throughout the country. Due to the high development prospects in all vehicle industry segments the Indian auto components industry is projected to record US$ 200 billion in revenue by 2026 the aftermarket of the industry is expected to reach US$ 30 billion. ( Source IBEF).

By FY28, the Indian auto industry aims to invest Rs. 58,000 crore (US$ 7 billion) to boost localization of advanced components like electric motors and automatic transmissions, reducing imports and leveraging ‘China Plus One’ trend.

The auto component industry in India is composed of organized and unorganized sector. The organized sector refers to original equipment manufacturers (OEMs) and is engaged in the manufacture of high-value precision instruments. Whereas, the unorganized sectors comprise of low-valued products catering to after-market services. The growth of global original equipment manufacturers’ (OEM) sourcing from India & the increased indigenisation of global OEMs is turning India into a preferable designing and manufacturing base. This leads to 8% of India’s R&D expenditure getting invested in the automotive sector.

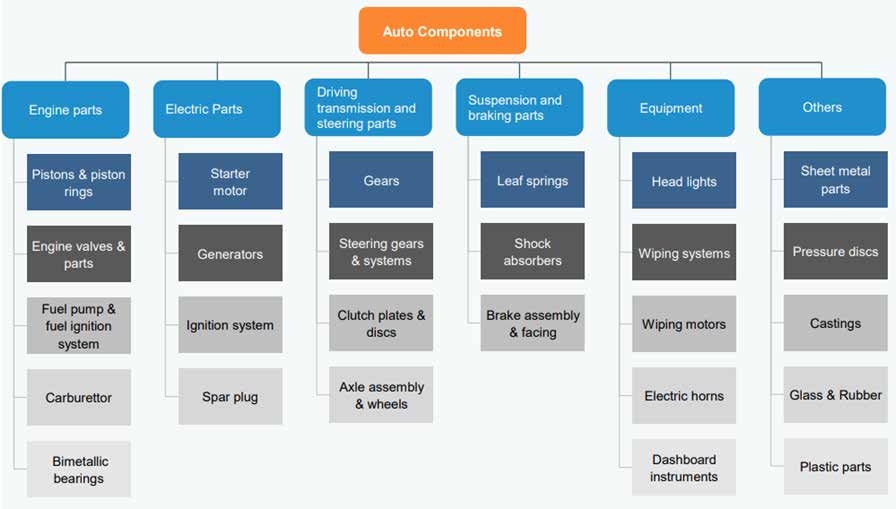

Various sub-sectors of the Auto components & parts industry in India are as follows:

I. ROBUST GROWTH OF INDIAN AUTO COMPONENTS & PARTS

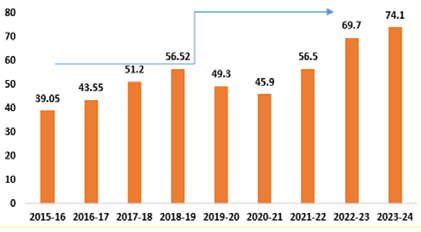

- The automobile component industry turnover stood at Rs. 6.14 lakh crore (US$ 74.1 billion) during FY24, registering a revenue growth of 9.8% as compared to FY23.

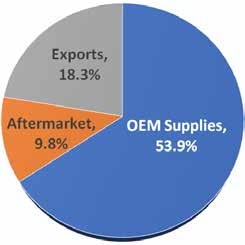

- Domestic OEM supplies contributed ~54% to the industry’s turnover, followed by domestic aftermarket (~10%) and exports (~18%), in FY24.

- The component sales to OEMs in the domestic market grew by 8.9% to Rs. 5.18 lakh crore (US$ 62.4 billion).

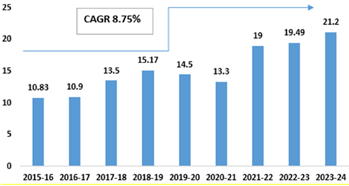

- During FY24, exports of auto components grew by 5.5% to US$ 21.2 billion. As per the Automobile Component Manufacturers Association (ACMA) forecast, automobile component exports from India are expected to reach US$ 30 billion by 2026. In FY22, India’s auto component Industry for the first time reached a trade surplus of US$ 700 million.

- The aftermarket for auto components grew by 10.0% during FY24 reaching Rs. 9.38 lakh crore (US$ 11.3 billion).

Aggregate Turnover (US$ billion)

Share in Turnover of the Auto Components Industry

II. EXPORT GROWTH

- Exports of automobile components from India increased, at a CAGR of 8.75%, from US$10.83 billion in FY16 to US$21.20 billion in FY23.

- During FY24, exports of auto components grew by 5.5% to US$ 21.2 billion. As per the Automobile Component Manufacturers Association (ACMA) forecast, automobile component exports from India are expected to reach US$ 30 billion by 2026. In FY22, India’s auto component Industry for the first time reached a trade surplus of US$ 700 million

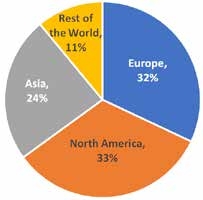

- In FY24, North America, which accounts for 32% of total exports, increased by 5%, while Europe and Asia, which account for 33% and 24% of total exports, increased by 12% and growth for Asia remained flat, respectively. The key export items included drive transmission and steering, engine components, body/chassis, suspension and braking etc.

Value of Auto Component Export (US$ billion)

A. INDIA’S TOP FIVE EXPORT DESTINATIONS IN THE LAST 3 YEARS

USA ranks as the numero uno destination of India’s export of Auto components & parts importing 27 percent of India’s export of the same in 2023. The share of other top nations are Turkey (6.7%), Germany (5.6%), Mexico (5.4%) and Brazil (4%).

Share of Export by Geography (FY24)

Table No.1: India’s top 5 Export Destinations in the last 3 years

| Values in US$ million | |||

|---|---|---|---|

| Top 5 Export Destinations of India | 2021 | 2022 | 2023 |

| World | 5969.4 | 6461.0 | 6684.0 |

| USA | 1586.5 | 1737.4 | 1777.8 |

| Turkey | 360.0 | 359.5 | 447.1 |

| Germany | 339.0 | 333.8 | 374.1 |

| Mexico | 296.0 | 295.7 | 361.7 |

| Brazil | 251.4 | 322.6 | 264.5 |

Source: ITC Trade Database

B. GLOBAL MAJOR SUPPLIERS OF AUTO COMPONENTS & PARTS IN B THE WORLD MARKET AND VIZ-A-VIZ INDIA’S RANK IN 2023

Table No.2: India’s rank as a global supplier of Auto components & Parts in 2023

| Rank | Global suppliers | Share in value in world's exports, % in 2022 |

|---|---|---|

| 1 | Germany | 14.5 |

| 2 | China | 11.6 |

| 3 | USA | 10.3 |

| 4 | Mexico | 8.3 |

| 5 | Japan | 6 |

| 6 | Korea Rep | 4.4 |

| 7 | Czech Republic | 3.8 |

| 8 | Poland | 3.6 |

| 9 | France | 3.3 |

| 10 | Italy | 3.3 |

| Rank | Global suppliers | Share in value in world's exports, % in 2022 |

|---|---|---|

| 11 | Canada | 3 |

| 12 | Spain | 2.6 |

| 13 | Hungary | 1.9 |

| 14 | Belgium | 1.8 |

| 15 | Thailand | 1.8 |

| 16 | Slovakia | 1.7 |

| 17 | Romania | 1.7 |

| 18 | Turkey | 1.6 |

| 19 | India | 1.5 |

Source: ITC Trade Database

III. AFTERMARKET GROWTH

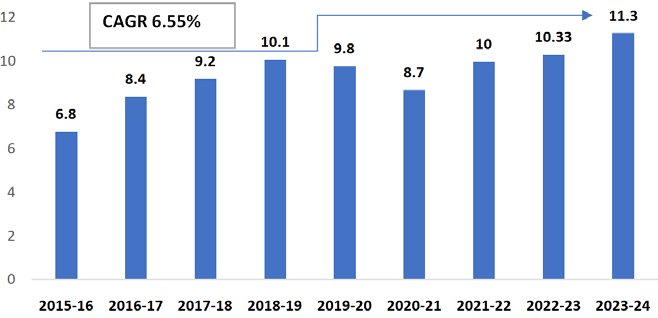

- The aftermarket for auto components grew by 10.0% during 2023-24 reaching Rs. 93,886 crore (US$ 11.3 billion)

- By 2028, the domestic automotive aftermarket segment in India is expected to reach US$ 14 billion.

- Aftermarket turnover increased at a CAGR of 6.55% from US$ 6.80 billion in FY16 to US$ 11.30 billion in FY24 and is expected to reach US$32 billion by FY2026.

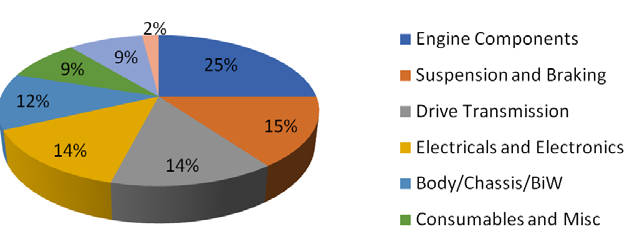

- The ‘Drive Transmission and Steering’ product category accounted for 21% of the aftermarket share followed by ‘Engine Components’, and ‘Electricals and Electronic Components’ with 19% and 18%, respectively.

- To support local auto parts suppliers, the auto component sector has tied up with Tesla to manufacture electric vehicles in August 2021.

Product-wise Share in Aftermarket Turnover (FY22)

Value of Aftermarket Turnover (US$ billion)

IV. MAJOR PLAYERS BY SEGMENT

Engine & Engine Parts

- Pistons - Goetze, Shriram Pistons & Rings, India Pistons, Anand I- Power Ltd.

- Engine Valves - Rane Engine Valves, Shriram Pistons and Rings, SSV Valves

- Carburetors - UCAL Fuel Systems and Spaco Carburetors & Escorts Auto Components

- Diesel - Based fuel-injection systems-MICO, Delphi-TVS Diesel System and Tata Cummins

Transmission & Steering Parts

- Steering Systems - Sona Koya Steering Systems, Rane NSK Steering Systems and Rane TRW Systems

- Gears - Bharat Gears, Gajra Bevel Gears, ZF Steering Gear (India) Ltd, Eicher, Graziano Trasmissioni and SIAP Gears India

- Clutch - Clutch Auto, Ceekay Daikain, Amalgamations Repco, LuK Clutches

- Driveshafts - Gkn Driveshafts, Spicer India Private Ltd., Delphi and Sona Koyo Steering Systems

Suspension & Braking Parts

- Brake Systems - Brakes India, Kalyani Brakes, Mando India Ltd. & Automotive Axles and GNA Axles Limited

- Brake Lining - Rane Brake Lining, Sundaram Brake Lining, Hindustan Composites and Allied Nippon

- Leaf springs - Jamna Auto & Jai Parabolic

- Shock Absorbers - Gabriel India, Delphi, Mando India Ltd. and Munjal Showa, rane Holdings Limited

Electrical

- Lucas TVS, DENSO, Delco Remy Electricals, Varroc Group and Nippon Electricals are key players in this segment

Equipment

- Headlights - Lumax, Autolite and Phoenix Lamps

- Dashboard - Premiere Instruments & Controls

- Sheet metal parts - Jay Bharat Maruti, Omax Auto and JBM Tools

- Sensors - Pricol Limited

V. GOVERNMENT INITIATIVES

From the above table no.2, we see that India’s ranks as the 17th global supplier of auto components & parts globally which is not a very significant rank, catering 1.6% of the total global supply of auto components & parts.

In order to make a significant mark in the global arena and help India’s automobile sector embark on a road to success, the Govt. has been providing a comprehensive support to the Automobile and Auto Components & Parts sector. The Government of India’s Automotive Mission Plan (AMP) 2006-26 has been instrumental in ensuring growth for the sector. The favourable policy measures aiding growth are as follows:

1. Union Budget 2023-24

- The Government has reaffirmed its commitment towards EVs and its mission for 30% electric mobility by 2030.

- Budget announced customs duty exemption on the import of capital goods and machinery required for the manufacture of lithium-ion batteries that typically power EVs.

- BHEL has successfully manufactured and tested India’s highest rating 500 MVA 400/220/33 kV Auto Transformer, at the National High Power Test Laboratory (NHPTL) at Bina in Madhya Pradesh- a new benchmark in the global transformer industry.

2. National Electric Mobility Mission Plan (NEMMP) 2020

- NEMMP aims to bring the transformational paradigm shift in the Automotive and Transportation industry by promoting hybrid and electrical mobility in India.

- There has been a cumulative outlay of USD 2.15 Bn for building such a roadmap. It is a composite scheme involving demand-side incentives to facilitate the acquisition of hybrid/electric vehicles along with the provision of supply-side incentives.

3. National Automotive Testing and R&D Infrastructure Project (NATRiP)- the largest and most significant initiative by the Government of India, in the Automobile component industry in India

- The chief aim of the project is:

- To generate core global competencies - state-of-art testing and R&D infrastructure.( 7 R&D centres - Chennai, Manesar, Indore, Raebareli, Silchar,Ahmednagar, Pune)

- To enable seamless integration by driving the automobile component industry in India into global automotive excellence.

- A total of USD 573 Mn investment has been done to adopt and implement global performance standards.

- The key focus lies in providing low-cost manufacturing and product development solutions.

4. Department of Heavy Industries & Public Enterprises

- Created a US$ 200 million fund to modernize the auto components industry by providing interest subsidy on loans & investments in newplants & equipment.

- Provided export benefits to intermediatesuppliers of auto components against Duty-Free Replenishment Certificate (DFRC).

5. Automotive Mission Plan 2016-26 (AMP 2026)

- AMP 2026 targets a fourfold growth in the automobile sector in India, which includes manufacturers of automobiles, auto components & tractors over the next 10 years. The government’s AMP 2016-26 will help the automotive industry grow and will benefit the economy in the following ways:

- The auto industry’s GDP contribution will rise to over 12%.

- Additional ~65 million direct and indirect jobs will be created.

- End-of-life policy will be implemented for old vehicles.

6. FAME Scheme

- Aimed at incentivising all vehicle segments - two wheelers, three wheelers, four wheelers, LCVs and buses. It covers hybrid & electric technologies like Mild Hybrid, Strong Hybrid, Plug in Hybrid & Battery- Electric Vehicles.

- In March 2023, centre approved US$ 97.85 million for 7,432 public fast charging stations under the FAME SchemePhase II.

- In February 2019, the Government of India approved FAME-II scheme with a fund requirement of US$ 1.39 billion for FY20-22.

- Department of Heavy Industries has sanctioned 2,636 charging stations in 62 cities across 24 States/UTs under FAME II.

7. Production-Linked Incentive (PLI) Scheme in the Automobile and Auto Components (2021)

- Outlay of USD 3.5 Bn for the automobile sector proposes financial incentives of up to 18% to boost domestic manufacturing of advanced automotive technology products andattract investments in the automotive manufacturing value chain.

8. Production Linked Incentive (PLI) Scheme for Advanced Chemistry Cell (ACC) Battery Storage (2021)

- Aims at achieving manufacturing capacity of 50 GWh of ACC for enhancing India’s manufacturing capabilities with a budgetary outlay of USD 2.3 Bn. This scheme was oversubscribed by 2.6 times (130 gwh).

9. FDI Policy

- 100% Foreign Direct Investment (FDI) is allowed under the automatic route in the Automobile component industry in India, subject to all the applicable regulations and laws.

10. Vehicle Scrappage Policy

- The Vehicle Scrappage Policy launched on August 13, 2021, is a government-funded programme to replace old vehicles with modern & new vehicles on Indian roads. The policy is expected to reduce pollution, create job opportunities and boost demand for new vehicles.

11. Battery Waste Management Policy

- The Battery waste management rule, published in August 2022 is a government programme to help reduce the dependency on new raw materials. The policy is expected to save natural resources, create new business & job opportunities.

12. State Incentives

- Apart from the mentioned, each state in India offers additional incentives for industrial projects. Incentives are in areas like subsidized land cost, relaxation in stamp duty exemption on sale and lease of land, power tariff incentives, concessional rate of interest on loans, investment subsidies, tax incentives, backward areas subsidies and special incentive packages for mega projects. Few examples are: Andhra Pradesh, Gujarat and Jharkhand.

VI. GROWTH DRIVERS

A. DEMAND-SIDE DRIVERS

- Growing working population and expanding middle class are expected to remain the key demand drivers. India is the fifth-largest automobile market globally.

- Increase in investment in road infrastructure.

- With the Self-Reliant India mission, the auto industry is looking to half its Rs. 1 trillion (US$ 13.6 billion) worth of auto component imports over the next 4-5 years. This will provide significant opportunities for existing and new auto components players to scale up.

B. SUPPLY-SIDE DRIVERS

- A cost-effective manufacturing base keeps costs lower by 10-25% relative to operations in Europe and Latin America.

- Second-largest steel producer globally, hence a cost advantage.

- India has a competitive advantage in auto components categories such as shafts, bearings and fasteners due to large number of players. This factor is likely to result in higher exports in coming years.

- India is emerging as a global auto component sourcing hub due to its proximity to key automotive markets such as ASEAN, Europe, Japan and Korea.

- Technological shift and focus on R&D- India retained the 40th position in Global Innovation Index among the top innovative economies globally as per Global Innovation Index (GII) 2023.

C. POLICY SUPPORT

- Visionary Govt. policies: Policies such as Automotive Mission Plan 2016-26, Faster Adoption & Manufacturing of Electric Hybrid Vehicles (FAME, April 2015) and NMEM 2020 are likely to infuse growth in the auto component sector of the country are likely to infuse growth in the auto component sector of the country.

- PLI schemes has been extended to the automobile sector with an aim of creating an incremental output of Rs. 2,31,500 crore (US$31.08 billion).

- The Government announced National Mission on Transformative Mobility and Battery Storage based on phased manufacturing program (PMP) until 2024.

- Lower excise duty on specific parts of hybrid vehicles.

- Establishing special auto parks & virtual SEZs for auto components.

New opportunities in the sector are as follows:

- New technological changes in Engine & Exhaust partsinclude introduction of turbo chargers and common rail systems.

- The trend of outsourcing may gain traction in this segment in the short to medium term.

- Share of replacement market in subsegments such as clutches is likely togrow due to rising traffic density.

- The entry of global players is expected to intensify competition in subsegments such as gears & clutches.

- Suspension & braking parts segment is estimated to witness high replacement demand with players maintaining a diversified customer base in thereplacement & OEM segments besides the export market.

- The entry of global players is likely to intensify competition insub-segments such as shock absorbers.

- Metal part manufacturers are likely to benefit from rising demand for body & chassis, pressure die castings, sheet metal parts, fan belts, and hydraulic pneumatic instruments, primarily in the two wheelers industry.

- Prominent companies in this business are constantly working towardsexpanding their customer base.

- In October 2021, Sona BLW Precision Forgings Limited, through its wholly owned subsidiary company, Sona Comstar eDrive Private Limited (Sona Comstar), entered a collaboration agreement with IRP Nexus Group Ltd., Israel, to develop, manufacture and supply magnet-less drive motors and matching controller systems for electric twoand three-wheelers.

VII INDIA IS POISED TO EMERGE AS AN OUTSOURCING HUB

- In March 2024, Tata Motors Group has signed a facilitation Memorandum of Understanding (MoU) with the Government of Tamil Nadu to explore setting-up of a vehicle manufacturing facility in the state. The MoU envisages an investment of Rs. 9,000 crores (US$ 1,081.6 million) over 5-year.

- Tata Motors, in April 2024, announced the inauguration of a new commercial vehicle spare parts warehouse in Guwahati.

- In December 2023, Tata Passenger Electric Mobility Ltd. (TPEM) and Bharat Petroleum Corporation Limited (BPCL) signed an MoU to jointly establish 7,000 public charging stations nationwide to enhance customer satisfaction.

- In April 2024, Maruti Suzuki India Limited, commissioned another vehicle assembly line at its Manesar facility.

- In January 2024, at the Vibrant Gujarat Global Summit, Maruti Suzuki announced the investment plans in Gujarat with a New Greenfield plant and a fourth line in SMG.

- In December 2023, Maruti Suzuki India Limited entered into an agreement with the Government of Haryana to establish the second Japan-India Institute for Manufacturing (JIM) as part of its corporate social responsibility (CSR) initiative. The company will invest Rs. 5.8 crore (US$ 698 thousand) to upgrade the existing ITI Kansala into a JIM.

- In May 2023, Maruti Suzuki India plans to invest over US$ 5.5 billion to double capacity by 2030.

- The Renault-Nissan alliance is stepping up its investments in India plans to invest US$ 600-700 million at its Chennai-based facility to step up platform localisation and improve sophistication levels in manufacturing.

- In July 2023, Renault Nissan to invest Rs. 1.4 crore (US$ 1,68,762.86) to upgrade infrastructure at eight schools near Chennai.

- In February 2023, Nissan and Renault plan to invest US$ 600 million in India over the next 3-5 years to expand their market share in passenger cars and electric vehicles.

- In July 2021, Nissan initiated a feasibility study to manufacture electric vehicles in India. If the study is positive when it is concluded in a year, Nissan may end up producing EVs in India for local sales and exports.

- In February 2024, company has announced it will invest over Rs. 32,000 crore (US$ 3.85 billion) from 2023 to 2033 in expanding its EV range and enhancing its current car and SUV platforms.

- In January 2024, Hyundai Motor India Limited announced Rs. 6,180 crore (US$ 743.8 million) investment plans in the state of Tamil Nadu including Rs. 180 crore (US$ 21.7 million) towards a dedicated ‘Hydrogen Valley Innovation Hub,’ in association with IIT- Madras.

- In January 2024, Hyundai Motor India Ltd. finalized the acquisition and transfer of specified assets at General Motors India’s Talegaon Plant in Maharashtra and inked an MoU with the Government of Maharashtra committing to an investment of Rs. 6,000 crore (US$ 722 million) in the state.

- In May 2023, Hyundai Motor announced that it will invest over Rs. 20,000 crore (US$ 2.41 billion) in Tamil Nadu over the next 10 years to bolster its EV production.

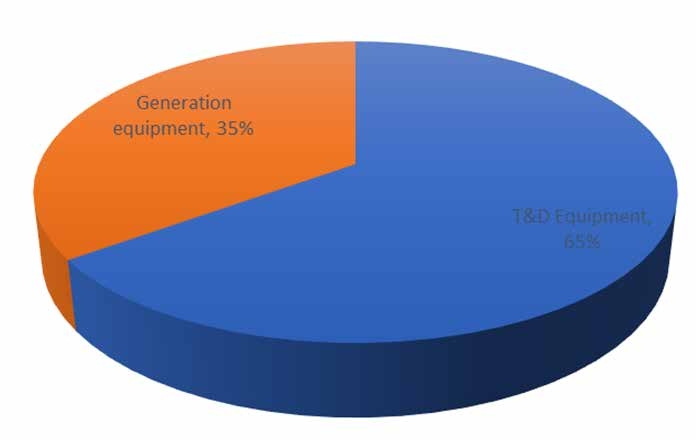

India’s electrical equipment industry is highly diverse and manufactures a wide range of high and low technology products. The industry directly employs around half million persons and provides indirect employment to another one million people. The industry can be broadly classified into two sectors – generation equipment (boilers, turbines, generators) and transmission & distribution (T&D) equipment & Allied Equipment like (transformers, cables, transmission lines, switch gears, capacitors, energy meters). Although higher imports still plague the industry but policy changes and various initiatives undertaken by the Government and industry are eventually showing signs of revival for the sector.

The industry is forecasted to double in size over the next seven years reaching USD 130 billion by 2030 as per IEEMA. During the same time exports are expected to grow 2.5 times. India also stands 4th globally in renewable energy installed capacity, 4th in wind power capacity and 4th in solar capacity. India is the third-largest producer and consumer of electricity worldwide.

The Government of India has de-licensed the Electrical Machinery industry and has allowed 100% foreign direct investment (FDI) in the sector. EEPC India, under the aegis of Ministry of Commerce and Industry, Government of India, has identified the Electrical Machineries &Equipment sector as one of the four focus sectors under ‘Brand India Engineering.’

‘Brand India Engineering’ is an initiative being implemented by EEPC India under the aegis of the Ministry of Commerce and Industry, Government of India, in close cooperation with the industry to enhance Indian engineering exports, by highlighting and showcasing Made in India products and their capabilities in the global market. The initiative involves a 360-degree approach in promoting the branding of Indian engineering products. It is expected to catapult India’s status in engineering capabilities, by highlighting India’s competitiveness, credibility & service commitments in engineering sector.

India Brand Equity Foundation (IBEF), a Trust established by the Department of Commerce, Indian Electrical & Electronics Manufacturers’ Association (IEEMA) and EEPC India are steering the campaign in coordination with national associations & industry stakeholders in the Electrical Equipment sector.

Fig.1: Composition of Electrical machinery & equipment industry

Source: IEEMA.org

SOME INTERESTING FACTS ABOUT THE ELECTRICAL MACHINERY SECTOR

- The industry represents about 7.2% of India’s total manufacturing output and 45% share in the capital goods sector

- The industry also accounts for 2.2 million jobs in the country

- The industry has grown at about 9.5% CAGR over the past 5 years

- Incentives for capacity addition in power generation will increase the demand for electrical machinery.

- Within the sector, high domestic output sub sectors are cables, transmission line towers, and LT switchgears (including panels), having industry size worth US $7 billion, US $2.7 billion and US$2.3 billion respectively.

- Renewable energy options to become more popular for power generation - India has set a target to reduce the carbon intensity of the nation’s economy by less than 45% by the end of the decade.

- There is also a target to achieve 50 percent cumulative electric power installed by 2030 from renewables, and achieve net-zero carbon emissions by 2070

- India aims for 500 GW of renewable energy installed capacity by 2030

ELECTRICAL MACHINERY EXPORTS ON THE RISE

India’s exports of Electrical Machinery and Equipment rose to USD 12.37 billion in 2023-24 from USD 5.3 billion in 2013-14 with a CAGR of 10%. The following diagram depicts the year-on-year growth in India’s export of electrical machinery &equipment.

The below table exhibits the performance of electrical machinery sub-sectors in the last five years. The table indicates that in the last five years export of transformers, cables & conductors, and generators.

Fig. 2: India’s Export of Electrical machinery &equipment(US$ billion)

Source: DGCI & S, Government of India

INDIA’S GLOBAL EXPORT OF ELECTRICAL MACHINERY -SUB SECTOR WISE

| Category | Sub-sectors | 2019-20 | 2020-21 | 2021-22 | 2022-23 | 2023-24 | CAGR (5 Years) |

|---|---|---|---|---|---|---|---|

| Generation Equipment | Boiler | 482.4 | 239.4 | 189 | 212.93 | 199.84 | -19.8% |

| Turbine | 440 | 453.3 | 384.2 | 308.48 | 315.6 | -8.0% | |

| Generator | 1027.3 | 984.2 | 1550.2 | 1593.49 | 1549.11 | 10.8% | |

| T&D Equipment | Transformers | 539.8 | 501.1 | 688.2 | 821.5 | 1070.35 | 18.7% |

| Capacitors | 114 | 119.6 | 150.4 | 153.38 | 165.74 | 9.8% | |

| Switch gear | 114.3 | 137.1 | 147.3 | 162.83 | 167.44 | 10.0% | |

| Cables & Conductors | 909.2 | 702 | 969.6 | 1264.39 | 1426.84 | 11.9% | |

| Transmission lines | 326.4 | 329.9 | 270.1 | 511.32 | 405.08 | 5.5% | |

| Energy meters | 51.9 | 38 | 46 | 43.26 | 45.34 | -3.3% | |

| Others | 7873.6 | 6831.5 | 8365.5 | 9262.2 | 10499.95 | 7.5% |

Source: DGCI&S, Government of India

INDIA’S TOP FIVE EXPORT DESTINATION IN THE LAST 3 YEARS SUB SECTOR WISE

USA ranks as the numero uno destination of India’s export of Generation Equipment, importing almost 19% of India’s export of the same in 2023. The share of other top nations are Germany (7.6%), UK (6.3%), France (3.7%), and Finland (3.6%).

In case of Transmission & Distribution (T&D) equipment also USA ranks as the numero uno destination of India’s export of the same, importing 28% of India’s export of the T&D equipment. The shares of other top nations are UK (7%), UAE (4.7%), Germany (3.6%) and Australia (3.4%).

| Values in US$ million | Generation Equipment | ||

|---|---|---|---|

| Top 5 Export Destinations of India | 2021 | 2022 | 2023 |

| World | 3620.64 | 4014.52 | 3799.98 |

| USA | 974.54 | 1026.19 | 701.80 |

| Germany | 253.24 | 254.93 | 289.77 |

| UK | 133.64 | 135.86 | 241.10 |

| France | 120.22 | 160.67 | 140.63 |

| Finland | 26.45 | 76.96 | 138.13 |

| Values in US$ million | T & D Equipment | ||

|---|---|---|---|

| Top 5 Export Destinations of India | 2021 | 2022 | 2023 |

| World | 3741.56 | 4747.34 | 5311.93 |

| USA | 784.72 | 1231.15 | 1491.61 |

| UK | 216.36 | 273.57 | 372.31 |

| UAE | 147.55 | 180.80 | 250.47 |

| Germany | 156.92 | 196.39 | 193.78 |

| Australia | 104.42 | 115.09 | 178.28 |

GLOBAL MAJOR SUPPLIERS OF ELECTRICAL MACHINERY & EQUIPMENTS IN THE WORLD MARKET AND VIZ-A-VIZ INDIA’S RANK IN 2021 SUB SECTOR WISE

Indian electrical and machinery equipment boasts of a diversified, matured and strong manufacturing base backed by a robust supply chain. Rugged performance design of equipment to meet tough network demand and presence of major foreign players, either directly or through technical collaborations with Indian manufacturers is a testimony of unique advantages India holds in this sector.

With state-of-the-art technology in most sub-sectors at par with global standards, Indian electrical equipment is exported globally. The major export products are Rotating Machines (Motors, AC Generators and Generating Sets) & Parts, Switchgear and Control gear, Transformers & Parts, Cables, Industrial Electronics, Boilers & Parts, and Transmission Line Towers etc.

The following tables show the rank of India as a global supplier of Generation equipment and T&D equipment in 2023.

STRATEGIES ADOPTED

The Government of India has adopted the following strategies to boost the Electrical machinery and equipment industry:

- New technologies – High-voltage technology is being developed in the Electrical Equipment industry, for economic power transmission. Firms are diversifying into the nuclear reactor business, as the government wants to increase its nuclear power base

- Capacity addition – India plans to increase investment in infrastructure (including electricity), as it lags behind other countries. With more capacity addition in the power sector, demand for electrical machinery would rise, prompting the companies to increase their production capacity

- Promotion of R&D – The Government is helping companies enhance the level of research to match the best in the world. The Government has relieved customs duties on some equipment. Companies, too, are enhancing their R&D departments to take advantage of the situation

- Skill upgradation and incentives – Skill upgradation is necessary as firms need to have the desired talent pool. The Government plans to set up the Electrical Equipment Skill Development Council (EESDC), which would focus on identifying critical manufacturing skills required for the electrical machinery industry. It is enhancing export incentives by removing export barriers

OIL & GAS SECTOR

India’s oil and gas sector is characterized by high and growing demand, significant import dependence (especially for crude oil), and a strategic focus on expanding domestic exploration, natural gas infrastructure, and refining capacity to improve energy security. The government is actively encouraging investment and policy changes to boost domestic production, develop strategic reserves, and increase natural gas consumption in the energy mix.

KEY ASPECTS OF INDIA’S OIL AND GAS SECTOR

- Demand and production – India is the world’s third-largest energy consumer, with demand projected to double by 2040. Despite this, its domestic crude oil production of around 29.4 million metric tons in FY2023-2024 falls far short of its consumption, leading to an import dependence of over 85%.

| Values in US$ billion | Generation Equipment | |

|---|---|---|

| Rank | Exporters | 2023 |

| World | 152.24 | |

| 1 | China | 28.65 |

| 2 | USA | 17.44 |

| 3 | Germany | 14.61 |

| 4 | Italy | 8.65 |

| 5 | Japan | 7.83 |

| 6 | Mexico | 5.94 |

| 7 | France | 5.69 |

| 8 | UK | 5.19 |

| 9 | Hungary | 3.89 |

| 10 | India | 3.79 |

| Values in US$ billion | T & D Equipment | |

|---|---|---|

| Rank | Exporters | 2023 |

| World | 360.4 | |

| 1 | China | 72.8 |

| 2 | Germany | 27.7 |

| 3 | Mexico | 25.03 |

| 4 | USA | 23.3 |

| 5 | Hong Kong, China | 14.5 |

| 6 | Japan | 13.2 |

| 7 | Italy | 10.6 |

| 8 | Korea, Republic of | 10.5 |

| 9 | Viet Nam | 9.9 |

| 10 | Poland | 9.6 |

| 11 | India | 5.3 |

© Copyright , All rights reserved. Design by Andreal