VOL. 17, ISSUE NO. 8 | November 2024

Spotlight

RAW materials are the backbone of any industry, and their availability at affordable prices is crucial for sustained growth and competitiveness. The primary raw material – steel – plays a crucial role in key industries like construction, infrastructure, automotive, engineering, and defence. The increase in steel prices is impacting the production costs for the engineering industry, making them less competitive globally. This poses a significant concern, requiring the industry to address rising costs strategically to maintain its global position.

India’s steel production and export trends

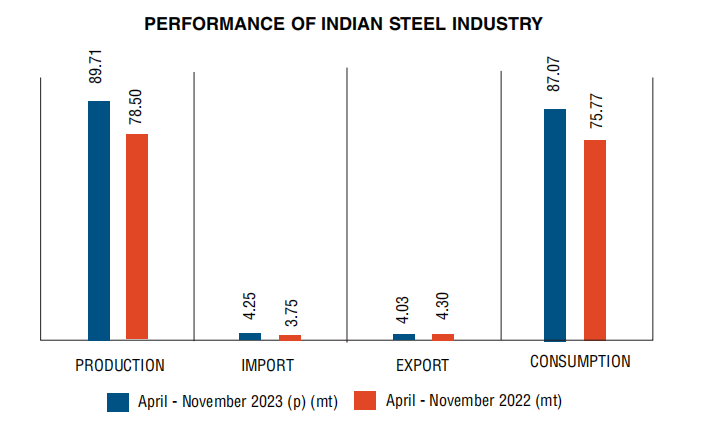

Over the years, the steel sector has seen tremendous growth, with India emerging as a global force in steel production and the world’s second-largest steel producer. The production performance of the steel sector in India during the first eight months of FY24 (April-November 2023) has been quite promising. The domestic finished steel production stood at 89.711 million tonne against 78.498 million tonne during the corresponding period the previous year, which is 14.3 percent higher. The domestic steel consumption stood at 87.066 million tonne, which is 14.9 percent higher than the previous period of 75.765 million tonne. Domestic crude steel production was 94.1+ million tonnes, with a growth of 14.7 percent when compared to the production of 82.072 million tonnes in the same period the previous year.

On the export front, India’s iron and steel and products of iron and steel during April-November 2023-24 touched $13.9 billion, constituting a share of 20 percent as a whole (11 percent share for iron and steel and 9 percent share for products of steel) out of India’s global engineering exports for the given period of $69.46 billion.

However, the industry has faced significant challenges, particularly the MSMEs, due to the global pandemic and the subsequent surge in raw material prices. This section examines the current raw material scenario, focusing on the rising steel prices and their adverse effects on the operating margins of engineering exporters in India.

Outlook

India’s steel industry is expected to grow substantially more than the global average, as per World Steel Association Outlook report. Steel demand in India is forecast to increase by 8.6 and 7.7 percent in 2023 and 2024, respectively, compared to just 1.8 and 1.9 percent globally. India was the second-largest producer of crude steel with an output of 128.15 mt in January-November 2023, showing a y-o-y growth of 12.1 percent. It accounted for 7.5 percent of world crude steel production during the January-November 2023 period, with China being the leader in world crude steel production, and Japan ranked as third-largest producer of crude steel. The healthy growth in India is driven by increased government infrastructure spending, recovering private investment, and continued momentum in the automotive sector. These factors will boost steel demand to support the construction, capital goods, and automotive industries in the country.

Industrialisation progressed and thrived due to the availability of metals. Steel occupied the top spot among 11 key infrastructure sectors. It serves major areas of economic development because it is a raw material, an intermediary product, and end product as well.

Sector-wise steel requirements

Steel finds extensive use in various sub-segments of the engineering sector, making it a critical component for many industries:

Some details on usage of steel in various sectors are mentioned here:

- Defence production: The range of manufactured products encompasses arms and ammunition, tanks, heavy vehicles, fighter aircraft, electronic equipment, earthmoving machinery, special alloys, and specialised purpose steels.

- Seamless steel pipes, tubes, and steel pipes: The extensive size range renders them suitable for various versatile applications. Approximately 60 percent of the total demand for seamless pipes comes from the oil sector, while the bearing and boiler sectors contribute to about 30 percent of the demand.

- Commercial and residential construction: It is anticipated that approximately 158 lakh mt of steel will be required for the construction of houses approved under the Pradhan Mantri Awas Yojana (Urban).

- Low-cost mass housing: In order to encourage the utilisation of steel in affordable housing, in prefab constructions, the Ministry is actively working on revising the BIS codes related to the design of prefab steel structures.

Automotive sector, roads, tower fabrication, bridges, etc are other sectors where steel is in demand.

Rise in steel prices rooted in escalating raw material costs

Despite being a beacon of hope in the global steel sector, the Indian steel industry is grappling with escalating raw material costs, particularly coking coal and alloy grades, posing significant challenges to its growth trajectory. This comprehensive analysis delves into the intricacies of the situation, examining the factors driving the price surge, its impact on steel production, and the strategic measures being adopted by industry stakeholders to navigate these hurdles.

The Indian steel industry is heavily reliant on imported raw materials, primarily coking coal, which accounts for nearly 60 percent of the production cost. The global supply of coking coal has been constrained by geopolitical tensions, supply chain disruptions, and rising demand from other steel-producing nations. This has led to a sharp increase in coking coal prices, reaching record highs in recent months. Compounding this challenge, the prices of various grades of alloying elements, such as nickel, manganese, and chromium, have also witnessed a significant uptick. These alloying elements are crucial for enhancing the strength, durability, and corrosion resistance of steel, making them essential inputs for the production of high-quality steel products.

EEPC INTERVENTIONS IN STEEL PRICING

Steel has always been a big issue for manufacturers and exporters, especially of engineering products. It was as early as the 1980s that the Engineering Export Promotion Council focused on making quality steel at international prices more easily available to manufacturer exporters.

At the 24th AGM of the Council held on 26 July 1980, then Chairman GD Shah, raised the issue of the challenges facing the exports of steel from India. The domestic price of steel was much higher than the international price and, therefore, Indian engineering goods were not competitive in international markets.

The Chief Guest at the AGM, former President Pranab Mukherjee, who was then the Union Steel and Commerce Minister, had an abiding interest in export growth as exports contributed valuable foreign exchange, and he directed GD to work on the issue in consultation with then Commerce Secretary PK. Kaul. GD worked relentlessly, and the International Price Reimbursement Scheme (IPRS), 1981, was the outcome, which the government introduced on 23 July 1981, towards making Indian engineering goods competitive.

How IPRS worked

For reimbursement purposes, the domestic price was fixed by the JPC (Joint Plant Committee), consisting of representatives of all major producers of steel along with the government representative who controlled the steel price) – plant price for those categories where JPC price control existed, and SAIL price for other items prevailing on the date of exports. After the export was effected, the price difference between its domestic price and the relevant international price was reimbursed to the exporter. Contracts eligible for reimbursement under this scheme (including fresh contracts) had to be registered with the concerned Regional Office of the EEPC within 45 days from the date of the contract.

However, some exporters misused the reimbursement scheme, and subsequently EEPC refused to recognise the exporters’ entitlement to avail of the benefit of the scheme.

Price scenario – global

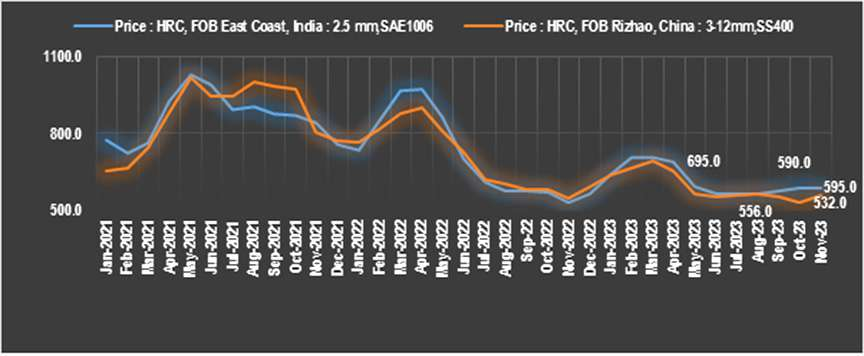

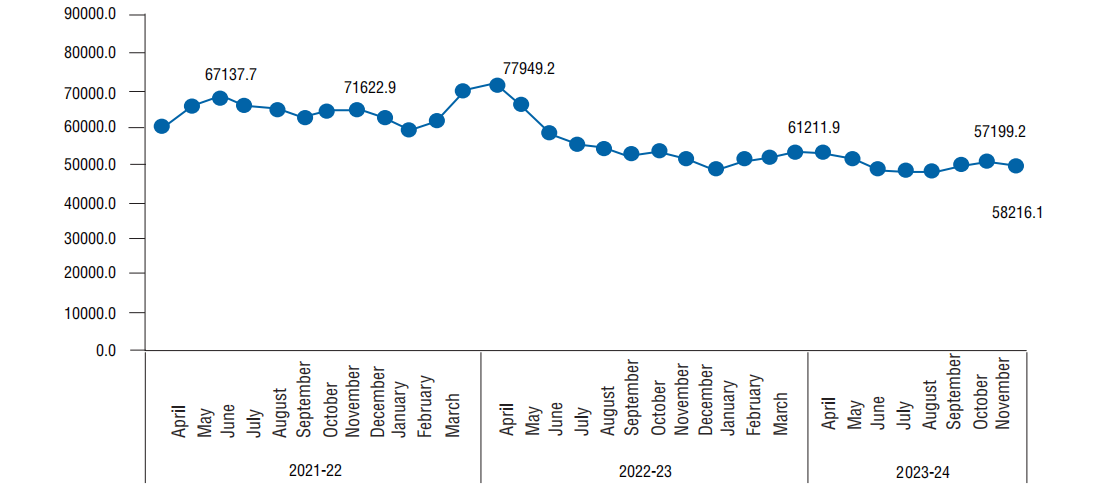

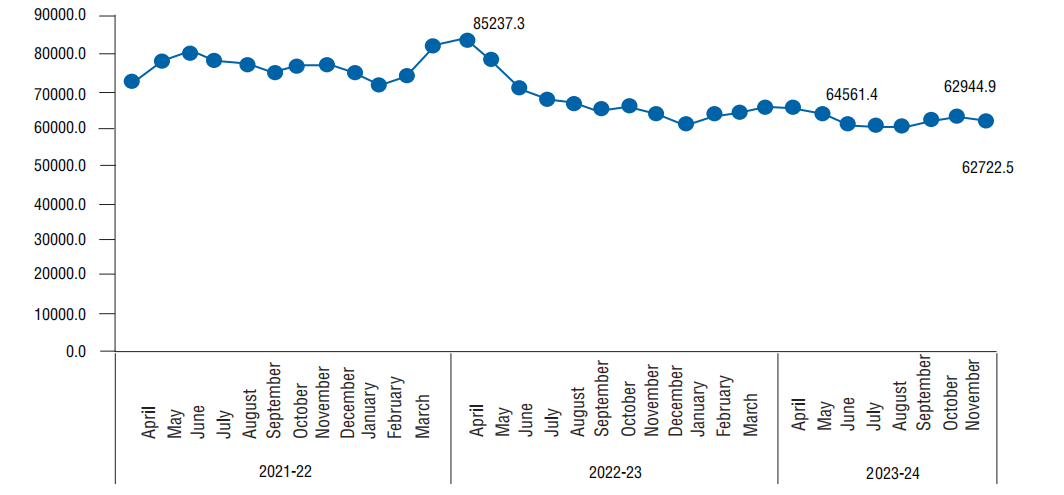

Taking a global perspective, it is evident that since February 2022, the price trend of India’s fob HRC products is on a higher side compared to China’s fob HRC prices. While India’s export fob price of HRC is almost at par with Japan and Korea, the international price gap between India and China varies within the range of 0 to 85. The international price trend of other countries including Japan and South Korea has also been compared.

The global steel industry is currently navigating a complex interplay of local and global factors that are shaping steel price trends. While prices in India and China have shown a modest downward bias month-on-month, the United States and Europe have witnessed an upward trajectory in steel prices over the same period. Rising energy costs and geopolitical tensions have further exacerbated the upward pressure on steel prices in these regions. Russia’s war of aggression against Ukraine, growing export restrictions on raw materials, soaring energy prices and their impacts on mining of raw materials, and other supply chains, while the Eurozone manufacturing sector remained stuck in contraction at the end of 2023. The entire continent struggled through a period of economic turmoil that began in late 2022. On the other hand, China’s spiralling property downturn and the government’s usage of stimulus to lift the sector is posing risk to the Chinese economy. China’s proposed production cuts and higher domestic demand, however, expected to push up steel prices.

Impact on engineering industry

The engineering industry is currently facing challenges in maintaining its competitiveness in the international market and fulfilling export obligations. To delve further into the matter, it is crucial to examine the utilisation of different categories of steel, such as hot rolled coils (HRC) and cold rolled coils (CRC), in various sub-segments of engineering. These segments primarily include automotive, railways, construction, pipes and tubes, among others. By analysing the prices of HRC and CRC, as illustrated in the following figures, we can understand the cost dynamics affecting the industry. This comprehensive evaluation will help in understanding the impact of raw material prices on the engineering sector’s overall performance and export capabilities.

Price scenario – India

Rising domestic demand and increasing raw material costs are pushing steel prices upwards. According to SteelMint, flat steel list prices had risen Rs750-2000 per tonne for October 2023 deliveries, while long steel prices saw an increase of Rs1500 per tonne in late September 2023. Trade and spot prices were also trending up. The monthly average price for hotrolled coil (HRC) – a flat steel benchmark – was Rs57,900 per tonne in September (Mumbai) but reached Rs58,950 per tonne on 6 October. Meanwhile, the average rebar price for long products in Mumbai rose from Rs56,740 per tonne in September to Rs58,100 per tonne on 9 October. Globally, higher iron ore and coking coal costs are impacting producers worldwide. This poses a major challenge, especially for steelmakers relying on imported coking coal.

The escalating raw material prices have exerted immense pressure on the profitability of steel producers in India. Steel mills are compelled to absorb the rising costs or pass them on to consumers through higher steel prices, both of which can have adverse consequences. Absorbing the increased costs erodes the margins of steel producers, potentially leading to financial distress and reduced investments in capacity expansion and technological upgrades. This can hinder the industry’s long-term growth and competitiveness. Passing on the higher costs to consumers, on the other hand, may dampen demand for steel, as end-users become more price-sensitive. This could lead to a slowdown in steel consumption, particularly in sectors such as construction and infrastructure, which are major consumers of steel.

Rising costs of steel raw materials: Concern for industry

The steel industry in India faces a pressing concern: the relentless rise in the prices of raw materials st the beginning of 2024. This surge sent shockwaves through the

industry, affecting stakeholders at every level. The industry’s ability to navigate this challenge will be pivotal in shaping its trajectory in the coming months. The surge in steel raw material prices has created a perplexing scenario for industry experts and stakeholders alike. Burstiness in pricing has created a volatile environment, leading to uncertainty and apprehension. The industry is grappling with the task of balancing these fluctuations while ensuring continued operations and profitability.

• Impact on production and operations

The repercussions of rising raw material prices have permeated every aspect of the industry. From manufacturing to logistics, the surge has disrupted established norms, compelling stakeholders to re-evaluate their strategies. The burstiness in pricing has led to challenges in planning and resource allocation, further exacerbating the situation.

• Embracing resilience

Ultimately, the industry’s ability to weather the storm of rising raw material prices hinges on its resilience and adaptability. Embracing a mindset that welcomes change and uncertainty can pave the way for sustainable growth and success. By harnessing the power of innovation and collaboration, stakeholders can navigate the perplexing landscape of fluctuating prices with confidence and tenacity.

Government initiatives

Due to hike in the price of steel, the Ministry of Commerce and Industry, along with ISA formulated a policy on Steel at Export Parity Price via Office Memorandum Ministry of Steel dated 24.06.2020. Under this scheme domestic steel producers would provide steel to the user industry (availed by only the MSME members of EEPC India) at an export parity price. These sales will be considered as deemed export and the steel producer can avail duty drawback on steel supplied through their premises, service centres, distributors, dealers or stockyards. The Steel at Export Parity Price scheme was made applicable on four product categories – HRC, CRC, wire rods, and alloy bars (https://content.dgft.gov.in/Website/dgftprod/7413adb6-54ce-41e4-93d5-7fdb8068e332/notificationon%20no.%2035%20dt%201.10.2020%20Eng.pdf). As per the notification, only six primary steel producers are included in the Export Parity Price scheme.

Figure2: International HRC price trend – India, China, Japan, South Korea

Figure3: International HRC price trend – India, China, Japan, South Korea

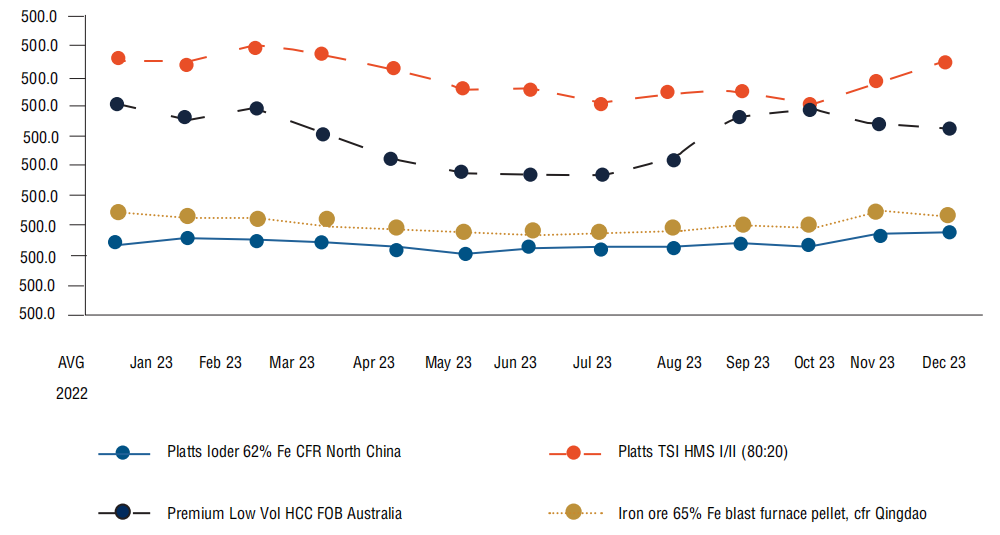

TRENDS IN GLOBAL PRICES OF MAJOR RAW MATERIALS FOR STEEL (S/T)

Figure1: Performance of steel industry

| Industry segment | Flat | Long |

|

Automotive |

• HR Coil • CR Coil • Coated sheet • Plates |

• Billets • Blooms |

|

Engineering |

• Electrical Sheet • HR Coil • CR Coil • Plates |

• Billets • Blooms • Wires • Rods • Bars |

|

Railways |

• HR Coils • Plates |

• Billets • Blooms • Wires • Bars |

|

Energy |

• Plates |

• Billets • Blooms • Wires • Bars |

|

Packaging & Appliances |

• HR Coil • CR Coil • Coated sheet • Plates |

|

|

Pipes & Tubes |

• HR Coils • Plates |

• Billets |

Source: EEPC India Analysis

Members suggested that the steel companies who supply steel at the Export Parity Price should be given all the benefits under the Export Parity Price scheme as they get for physical exports to make the scheme more active and useful for the user industry.

Furthermore, it was suggested that the DGFT should provide the Export Parity Price based on DGCI&S fob data for all the four products (HRC/CRC/wire rods/bars) at present. In addition, all major steel producers should be included in the Export Parity Price scheme as currently only six primary steel producers are under the scheme. It was also suggested that apart from these four products, other steel products like billets, which are used by the MSME sector should be covered under the scheme.

Other initiatives

The government acts as a facilitator by creating conclusive policy environment for development of the steel sector. Some of the important policies and initiatives of the Government of India for the steel sector are:

- Government of India notified National Steel Policy, 2017, which envisages development of a technologically advanced and globally competitive steel industry that provides environment for attaining self-sufficiency in steel production by providing policy support and guidance to steel producers.

- Production linked incentive (PLI) scheme for Specialty Steel was approved by the Union Cabinet on 22.07.2021, with total financial outlay of Rs6322 crore to promote the manufacturing of ‘Specialty Steel’ within the country by attracting capital investment, generating employment, and promoting technology up-gradation in the steel sector. The scheme was notified in the official Gazette on 29.7.2021 and detailed scheme guidelines were published on 20.10.2021. On 17.03.2023, the Ministry of Steel signed an MoU with the 27 selected companies having 57 applications. This scheme will attract total investment commitment of Rs29,530 crore with capacity addition of 24,780 thousand tonnes.

- Steel Quality Control Order (QCO): Ministry of Steel has introduced Steel Quality Control Order (QCO) thereby banning substandard/defective steel products both from domestic producers and imports to ensure the availability of quality steel to the industry, users, and public at large. As per the Order, it is ensured that only quality steel conforming to the relevant BIS standards are made available to the end-users. As on date 145 Indian Standards have been notified under the Quality Control Order covering carbon steel, alloy steel and stainless steel. Out of these, QCO on 144 Indian Standards have been enforced.

- Research and development (R&D): Ministry of Steel is providing financial assistance for pursuing R&D to address the technological challenges faced by the iron and steel sector. In this regard, in May 2023, Ministry of Steel sought R&D project proposals in joint collaborative mode from reputed academic institutions, research laboratories and steel companies for pursuing R&D projects on the identified thrust areas, for providing financial assistance under the R&D scheme for the financial year 2023-24.

- Domestically Manufactured Iron and Steel Products (DMI&SP) policy for promoting procurement of Made in India steel by government and public sector projects.

- Notification of Steel Scrap Recycling policy to enhance the availability of domestically generated scrap.

Thus, the Indian government has recognised the challenges faced by the steel industry and has taken steps to provide support. This includes measures such as reducing import duties on raw materials and providing subsidies to steel producers. The government is also working on Production Linked Incentive (PLI) scheme 2.0 as well as looking at ways to ensure adequate raw material supply for the steel sector in 2024. India has set a target of having an installed steel manufacturing capacity of 300 MT by 2030. At present, the country has a capacity of around 161 MT. The government is also focusing on promoting the usage of scrap.

Further, the government has focused on efforts to be made for the use of artificial intelligence and new-age technologies among the industry players to boost steel output while also looking at reducing carbon emissions. The government had already approved the PLI scheme 1.0 to boost the production of speciality steel that would help create additional capacity of around 25 MT. It is expected that the production and demand for steel will improve in 2024 on the back of infrastructure projects.

Figure4: JPC prices of HR coils 2 mm (Rs/tonne)

Figure5: JPC prices of CRC 1.0 mm (Rs/tonne)

Prices of Iron Ore

Recommendations

- Establishment of an Independent Steel Regulator: To address the disparities in pricing between domestic and export markets, it is crucial to establish an independent steel regulator. The body would ensure domestic price parity with export prices and protect interests of steel user industries as well. This will also help in resolving distortions in pricing (export vs domestic), which may provide undue benefits to one segment of the industry at the cost of another.

- Encouraging specialised steel production: Overall, India has limited presence in tool steel, super duplex, super austenitic, and high alloyed varieties of stainless steel for stringent end use applications. For certain steel categories (or components), which have limited production in India, reduction of import duties may be considered till the time those are produced in India cost effectively

- Addressing cost-related challenges: Steel is an important material in the engineering sector. High logistic, finance cost, power cost, cess, royalty is making India’s steel industry commercially non-competitive. In order to strengthen steel, the government should provide benefits to the steel industry and simultaneously the user industry needs to be protected. The government should maintain a balanced approach to protect the interest of the user industry as well as to support the steel industry.

Conclusion

Creating a conducive ecosystem for both the steel industry and user industries is very important. The government intervention plays a crucial role in ensuring a balanced approach that enables the availability of affordable raw materials for the steel industry and related sectors. A thriving steel industry holds immense significance for any economy, and concerted efforts are required to bolster its competitiveness in the global market.

A competitive steel industry positively impacts the user engineering industry as well, leading to an overall enhancement of the engineering sector’s competitiveness. To achieve this, the government must remain focused on implementing measures that support the steel industry’s growth and global standing.

A critical aspect that demands government attention is the availability of specialised steel in the country. By fostering domestic production of specialised steel varieties, the government can reduce reliance on imports, address trade deficits, and empower user industries with access to critical raw materials.

The introduction of the Steel at Export Parity Price policy was a commendable step by the government. To ensure its success, greater emphasis is needed to streamline its operational implementation. Effective policy execution, along with continued support from the government, will significantly contribute to the steel industry’s success and, consequently, the success of the engineering sector.

The Indian steel industry is facing significant headwinds due to rising raw material prices. However, the industry is demonstrating resilience and adaptability in responding to these challenges. A well-coordinated effort between the government, the steel industry, and user industries is imperative to build a robust and competitive engineering sector. By prioritising the steel industry’s growth, ensuring affordable raw materials, and promoting specialised steel production, India can strengthen its position in the global engineering market.

Overall, in order to promote ease of doing business all industry players need to adopt artificial intelligence and modern technology to increase production and simultaneously reduce carbon emissions within the industry. Thus, by implementing innovative strategies and seeking government support, the industry can navigate these hurdles and continue to play a vital role in India’s economic growth and development.

© Copyright , All rights reserved. Design by Andreal