VOL. 18, ISSUE NO. 10 | January 2026

Focus

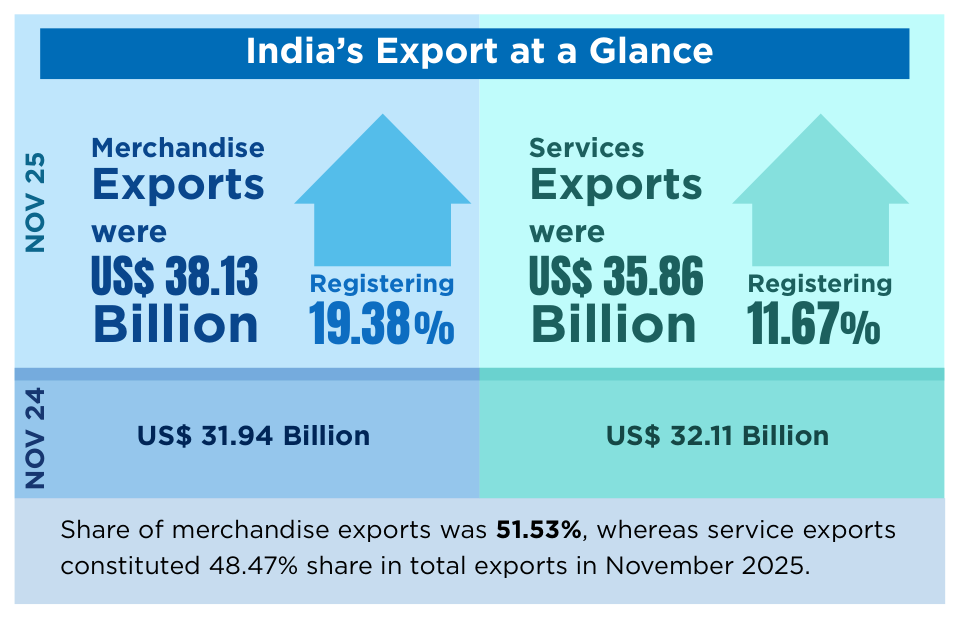

India’s exports recorded year‑on‑ year growth in November 2025, reflecting sustained momentum in external trade. The increase was supported by higher export values across key merchandise and ser‑ vices sectors, alongside steady de‑ mand from major partner countries. This performance underscores the resilience of India’s export sector amid evolving global trade conditions.

EXPORT SEGMENTS THAT PERFORMED BEST

Readymade Garments of all Textiles

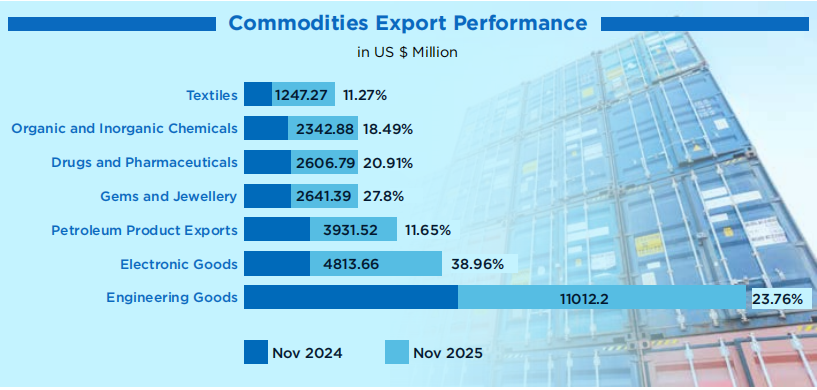

- A labour‑intensive sector, that continues to contribute positive‑ ly. Exports rose to USD 1247.37 Million with 11.27% increase in November 2025 compared to last year.

- Some of the large export markets for India showing growth were UAE (14.5%), UK (1.5%), Japan (19.0%), Germany (2.9%), Spain (9.0%) and France (9.2%).

- Some markets that recorded higher growth rates were Egypt (27%), Saudi Arabia (12.5%), Hong Kong (69%) etc.

Organic and Inorganic Chemicals

- Exports grew by 18.49% over the year in November 2025.

- India’s drugs and pharmaceutical sector recognised as the Pharmacy of the World, experienced 20.19% growth in exports over the year.

- Indian pharma exports are destined to more than 200 countries around the globe including highly regulated markets of US, West Europe, Japan and Australia indicating diversification in this sector.

Gems and Jewellery

- Growth of 27.8% in November, 2025.

- Indian jewellery is admired for its craftsmanship, design, and cul‑ tural richness.

- Demand is growing in key mar‑ kets such as the United States, United Arab Emirates, Hong Kong, and Europe, especially for gold, diamond, and coloured gemstone jewellery.

Petroleum Product Exports

- India is the seventh‑largest ex‑ porter of refined petroleum products and ranks among the top five refining nations globally, due to its robust infrastructure and strategic geographic loca‑ tion.

- The export growth in November 2025 was 11.65%

- Key export destinations were South Asian, African, and Euro‑ pean nations.

Engineering Goods

- A traditional pillar of India’s exports, have recorded steady growth, with the US as the top destination, followed by the UAE, Germany, the UK, and Saudi Arabia.

- To sustain momentum, the government has rolled out measures such as Zero Duty EPCG and the Market Access Initiative (MAI) to support exporters and boost overseas revenues.

- With a target of building a $500 billion domestic electronics ecosystem by 2030‑31, India is

now firmly on track to become a global leader in electronic design, manufacturing, and exports.

- Leading the way are mobile phones from just ₹1,500 crore in 2014‑15, mobile phone exports reached ₹2 lakh crore in 2024‑ 25, growing 127 times in a single decade.

- Indian electronics goods are now exported to major markets, with the top five destinations in FY 2024‑25 being the United States, United Arab Emirates, Netherlands, the United Kingdom, and Italy.

EXPORT DIVERSIFICATION: A STRATEGIC APPROACH

Export diversification has emerged as a deliberate policy strategy. It helps navigate uncertain global trade environments marked by geopolitical tensions, demand volatility, and supply chain disruptions. By expanding across products and markets, countries reduce overdependence on limited partners and build resilience against external shocks. This approach strengthens trade stability, competitiveness, and longterm economic security amid global uncertainties.

How does it help?

Avoiding export instability and reducing dependency

Commodity dependent exports are inherently exposed to sharp price fluctuations, which can lead to instability in export earnings if countries rely on a narrow set of products. Such volatility may heighten macroeconomic uncertainty and dampen longterm investment decisions. Export diversification offers a pathway to greater stability by spreading risk across products and markets, thereby supporting sustained export growth and longterm economic resilience.

Building resilience against global demand shocks

Building resilience against global demand shocks is crucial, as limited export diversification can leave economies vulnerable to sudden downturns in global demand. Diversifying exports enhances the ability to absorb such economic shocks by spreading risk across sectors and markets, thereby ensuring greater stability in export performance.

Encouraging knowledge spillover Expanding Global Ties:

Export diversification fosters flow of ideas, skills, and information by encouraging adoption of new production techniques, management practices, and marketing capabilities that can diffuse across industries. By expanding the range of export products, economies strengthen learning, innovation, and productivity, supporting higher per capita income growth over long term.

Strengthening macroeconomic stability

Exports alone accounted for 21.2% of India’s GDP in 2024. Limited diversification can expose the economy to global uncertainties and export shortfalls, affecting macroeconomic stability. Export diversification strengthens stability by broadening economic activity, reducing vulnerability to external shocks, and supporting sustainable growth and improved living standards.

Expanding Global Ties: Unlocking Trade Opportunities for India

As India’s economic footprint continues to expand worldwide, it has emerged as a preferred partner for deeper trade and economic collaboration.

CEPA Between India and Oman India’s 2nd FTA after UK in a span of 6 months

Oman is a key pillar of India’s West Asia Policy and India’s oldest strategic partner in the region. The strong economic partnership is reflected in 6,000+ India–Oman joint ventures operating in Oman. India signed a Comprehensive Economic Partnership Agreement (CEPA) with Oman on 18 December 2025, marking a significant step in strengthening economic engagement with the Gulf region, as the two countries commemorate 70 years of diplomatic relations. The agreement underscores India’s growing stature as a trusted and dependable global trade partner.

The agreement opens new export opportunities for India’s labour‑intensive sectors‑ such as agriculture, textiles, leather, gems and jewellery, engineering, pharmaceuticals, and automobiles‑ supporting job creation and empowering artisans, women‑led enterprises, and MSMEs.

India held a 10.24% share in Oman’s agricultural imports in 2024, ranking second among suppliers. Major export items include Basmati rice, parboiled rice, bananas, potatoes, onions, meal of soyabean, sweet biscuits, cashew kernels, mixed condiments, butter, fish body oil, prawn & shrimps feed, frozen boneless bovine meat, and fertilized eggs. Duty free access to boneless meat of bovine animals, other fresh eggs, sweet biscuits, cashew kernels, other fats & oils derived from milk, other mixed condiments & seasonings, prepared/preserved potatoes, other egg yolks not dried, guar gum, kabuli chana and other cheese provide a competitive edge over other countries exporting to Oman.

Elimination of tariff from butter, sugar confectionery, bakery products, poultry meat & offal, mixed condiments & mixed seasoning, other fruit squash prepared/preserved, natural honey strengthens India’s position in Oman’s market. CEPA offers unprecedented market access for Indian goods with zero‑duty access on 98.08% of Oman’s tariff lines, covering 99.38% of India’s exports by value.

It marks the first‑ever commitment by any country on traditional medicine across all modes opening significant opportunities for India’s wellness sectors and AYUSH, which anchors India’s traditional medicine sector through a comprehensive institutional framework.

For the first time, Oman has offered commitments across key mode 4 categories, high quality temporary entry and temporary stay commitments for intra‑corporate transferees, and contractual service suppliers, business visitors and independent professionals and liberalised entry and stay for professionals in accountancy, taxation, architecture, medical and allied sectors.

18 l INDIAN ENGINEERING EXPORTS l JANUARY 2026

INDIA-NEW ZEALAND FTA

REINFORCING INDIA’S PRESENCE IN THE INDO - PACIFIC REGION

India and New Zealand an‑ nounced the negotiation of an FTA in March 2025. Following several rounds of negotiation the FTA was finally concluded in De‑ cember 2025. In this article we look into the growing significance of New Zealand as a member of In‑ do‑Pacific region and the potential it has to offer to India in terms of trade especially with respect to the engineering sector.

Growing significance of Indo-Pacific region in India’s trade

Owing to the presence of strate‑ gically important waterways and trade routes over the time the In‑ do‑Pacific region has emerged as a vital region in terms of both geo‑ politics and geo‑economics. The strategic importance of the region has led to some major regional economic frameworks in the re‑ gion including the Comprehensive and Progressive Agreement for Trans‑Pacific Partnership (CPTPP), the Regional Comprehensive Eco‑ nomic Partnership (RCEP), and the Indo‑Pacific Economic Framework (IPEF). As a part of this region, In‑ dia’s approach to the Indo‑Pacific is important for regional stability. However, India’s participation in the regional frameworks have been limited mostly due to concerns of threat to the domestic industry– for instance, despite being one of the earliest countries advocating the need for RCEP and actively par‑ ticipating in the negotiations, India ultimately refused to sign the same citing concerns regarding threat to the domestic industry from RCEP partners particularly China. This notwithstanding the fact that the FTA, world’s largest one, represent‑ ed a combined GDP of USD 26 tril‑ lion and a total export value of USD 5.2 trillion.Similarly, in case of IPEF which is a US led economic initia‑ tive economic initiative for regional cooperation, India joined Pillars 2 (supply chains), 3 (clean economy) and 4 (fair economy) but refused to sign the first pillar that was on trade due to concerns regarding the possibility of binding conditionality linking the same to issues like envi‑ ronment and labour.

While India limited its presence in IPEF and withdrew from RCEP, the Indo‑Pacific region remained signif‑ icant for India due to its strategic importance and the huge market it commands. This was further re‑ inforced following the consecutive shocks of the COVID 19 pandem‑ ic, the rising geopolitical tensions across the globe and increasing protectionist policy making by the developed countries in the West. The need to increase its presence resulted in India forging three con‑ secutive FTAs with ASEAN, Japan and South Korea in 2010‑11. Follow‑ ing these, there was a period of lull, however, the Economic and Trade Agreement (ECTA) signed between India and Australia in 2022 marked India’s second initiative to strength‑ en its presence in the region. With the conclusion of the New Zealand FTA, India now has trade agree‑ ments with 14 out of 15 RCEP na‑ tions barring China and 12 out of 14 nations in the IPEF barring USA and Fiji. It needs to be mentioned here that India does share a limited agreement with China – Asian Pa‑ cific Trade Agreement and is also negotiating a bilateral trade agree‑ ment with USA.

- Benefits of trade with Indo-Pacific partners: The Indo‑Pacifi‑ cregion commands a large mar‑ ket with significant production base and can be termed as a centre of global trade and com‑ merce. It accounts for 63 percent of global GDP and 46 percent of global merchandise trade. Trade Agreements with Indo‑Pacif‑ ic members give India access to the large integrated markets. Furthermore, many of the In‑ do‑Pacific countries, especially China, Japan, South Korea and few ASEAN countries are most‑ ly members of significant glob‑ al value chains. Therefore, FTAs with them can help Indian busi‑ nesses to also become part of large value chains and help them expand their business. Addition‑ ally, Indian manufacturers and exporters can also benefit from technical cooperation with high‑ tech members including Japan, South Korea, Australia and New Zealand. This will help them to produce better and more com‑ petitive products. Finally, these FTAs can also act as a counter against the RCEP/ IPEF led trade diversion.

The importance of Oceania in India’s trade diversification journey:

Australia and New Zealand are also part of the Oceania region which has not been a traditional export destination for the Indian export‑ ers. However the need to increase our presence in these marketsis am‑ plified by rising protectionist mea‑ sures globally:

- USA’s Section 232 tariffs on steel, aluminium, steel derivatives, and autos, coupled with reciprocal tariff actions, have created un‑ certainty for Indian exporters, re‑ ducing competitiveness in a tra‑ ditionally strong market.

- Mexico’s recent tariff imposition on nearly 1,400 products (as per news reports) signals a shift to‑ ward protectionism, compelling exporters to explore alternative destinations.

- EU’s Carbon Border Adjustment Mechanism (CBAM) and safe‑ guard measures on steel and other products further restrict market access and increase com‑ pliance costs for Indian firms.

These developments underscore a global trend of protectionist trade policies, making diversification im‑ perative. On the other hand, Ocea‑ nia is a fairly new market for Indian exporters and the FTA with Austra‑ lia has produced significant gains. Since 2022, India’s exports to Oce‑ ania increased from around USD 7.6 billion to USD 8.51 billion regis‑ tering a growth of 5.4 percent. An FTA with New Zealand will not only boost exports but also enhance product diversification, mitigating risks from concentrated market de‑ pendence and also strengthen our position in the Oceania region.

India’s trade with New Zealand

With this background, we look into the potential that New Zealand has to offer to India in terms of exports after the conclusion of the FTA:

India’s bilateral trade with New Zealand has been rising in the re‑ cent years. In FY 2024‑25, the two countries shared a bilateral trade of USD 1.3 billion. During the same period, India’s total exports to New Zealand, increased by more than 32% on a y‑o‑y basis to reach USD 711 million.

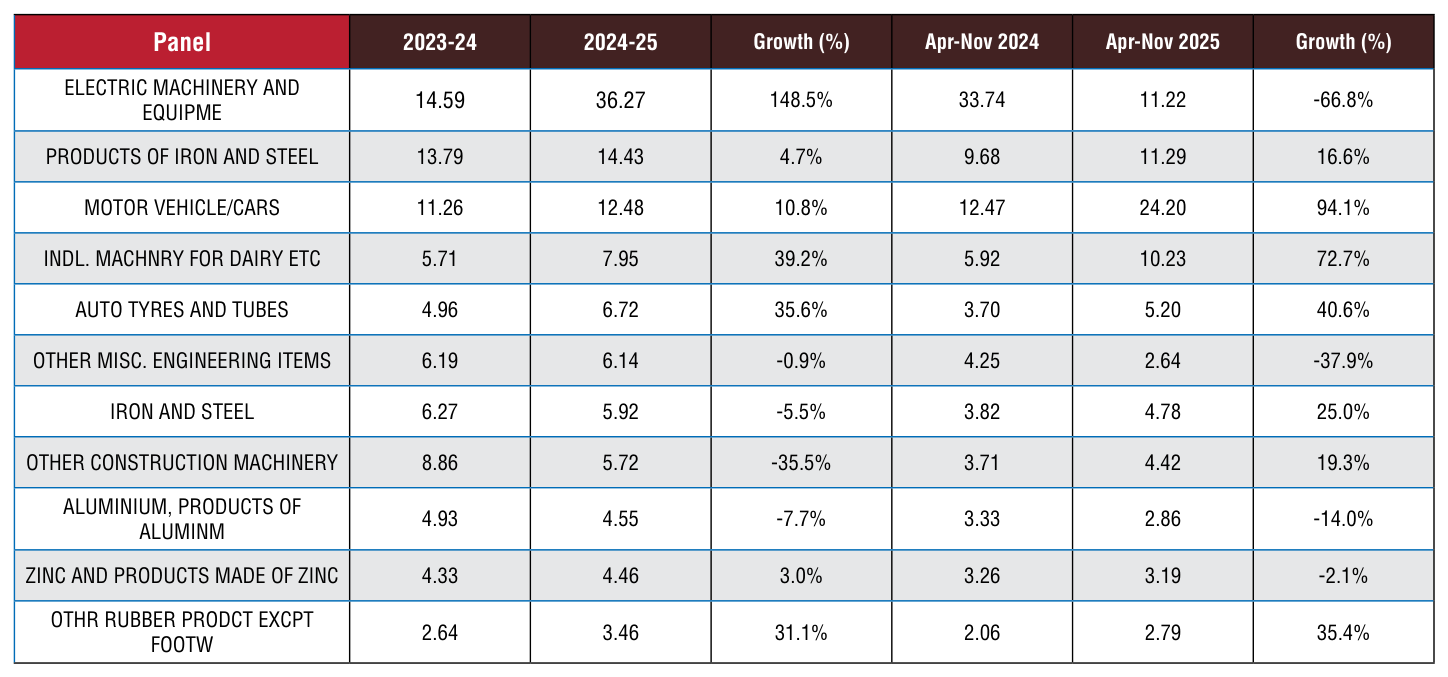

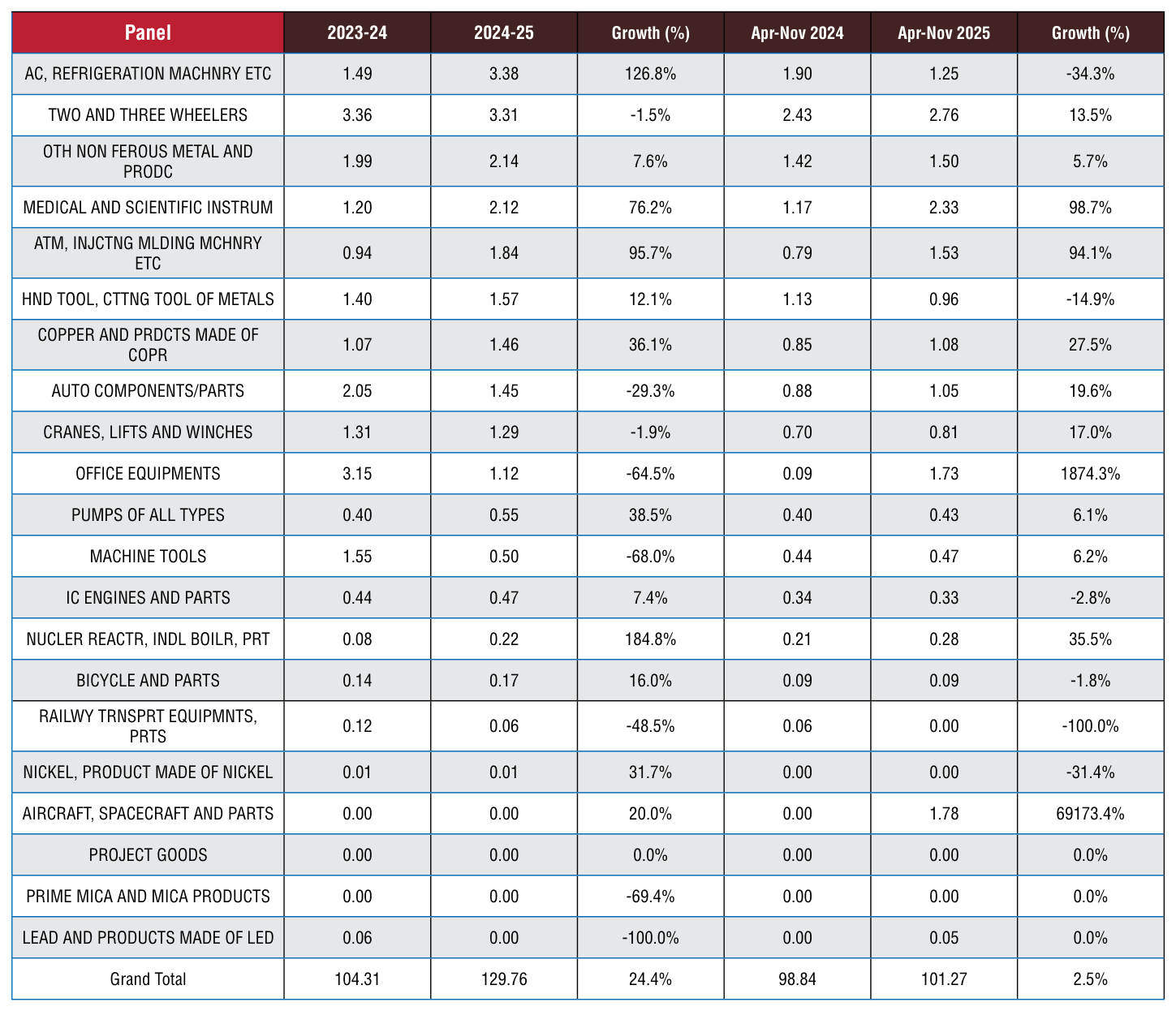

Within engineering, India’s major exports to New Zealand include electric machinery, motor vehicles, products of iron and steel, etc. In FY 2024‑25, India’s engineering ex‑ ports to New Zealand increased by more than 24% to reach USD 130 million. In the current fiscal too, In‑ dia’s engineering exports to New Zealand is on a steady growth path in April‑November 2025‑26, India’s total engineering exports to New Zealand stood at USD 101.26 million recording a growth of more than 2%.

While the trade between the two countries have been growing, In‑ dia’s engineering exports to New Zealand still remain miniscule and has not reached its potential. In FY 2024‑25, New Zealand’s share in India’s total engineering exports remained at around 0.1%. However, engineering export’s share in In‑ dia’s total exports to New Zealand is more than 18% signifying the im‑ portance of the sector in New Zea‑ land’s import basket.

Table 1: India’s engineering exports to New Zealand (USD Mn.)

Source: DGCI&S

Major engineering sectors

1.Electric machinery and equipment

India’s exports in FY 2024‑25 stood at USD 36.27 million, re‑ cording a growth of more than 100%. Currently, New Zealand imposes an average tariff of around 0.6% on electrical ma‑ chinery products imported from India. A duty free access would imply better opportunities for a large number of products in this sector including high val‑ ue products such as turbojets and turbo propellers, electrical transformers and static con‑ verters.

2. Products of iron and steel

In FY 2024‑25, India’s exports to New Zealand stood at USD 14.43 million recording a growth of around 5% in y‑o‑y terms. Duty free access for this sector may benefit exporters in a large number of products of iron and steel including tubes, pipes and hollow profiles, screw, nuts and bolts and even table and kitch‑ en utensils and cookers.

3. Motor vehicles/cars

In FY 2024‑25, India exported motor vehicles and cars worth of USD 12.48 million to New Zealand which is a major mar‑ ket for automobiles. Therefore duty free access under the FTA will be a great booster for the industry.

4. Industrial machinery (including food processing, textiles, chemicals)

Exports to New Zealand surged to USD 7.95 million in 2024‑25. Removing duty will make Indi‑ an machinery more attractive for New Zealand especially for products such as refrigerators, washers and dryers, air or vacuum pumps, etc.

5. Auto Tyres and Tubes

Exports climbed to USD 6.72 million in FY 2024‑25 from USD 4.96 million. A duty free market access in New Zealand will ben‑ efit products including pneu‑ matic tyres of various kind, solid or cushion tyres, etc.

• The significant untapped potential offered by New Zealand:

Currently, India is among the top 20 suppliers to New Zealand with a share of around 1% in its engineering import bas‑ ket. The major partners of New Zealand include majorly RCEP partners apart from USA, Ger‑ many, UK, France and Italy. With the FTA and Early Implementa‑ tion Framework, all engineering items will have duty‑free access to the New Zealandwhich will be a significant boost for the exporting community. It will also boost India’s share in New Zealand’s engineering import basket.

The Principal Outcomes of the India-New Zealand FTA:

The FTA provides a transparent framework for the exporters in both countries in terms of expand‑ ing market access and enhance trade services and also encourage long‑term investment partnerships. Some of the outcomes favourable for Indian businesses include:

- 100% Duty free access to all Indian exports ensuring imme‑ diate competitiveness for Indi‑ an products across labour‑in‑ tensivemanufacturing and in pharmaceutical, chemical, en‑ gineering, and agri‑processed sectors,reducing landed costs and expanding export opportu‑ nities

- New Zealand has committed to facilitating USD 120 billion in investments in India over the next 15 years supporting areas including manufacturing, infra‑ structure, innovation and job creation – joint strategies to promote investmentparticular‑ ly in high‑value sectors such as renewable energy, digital ser‑ vices, and modern infrastruc‑ ture are covered

- The FTA establishes a new TemporaryEmployment Entry (TEE) Visa pathway for Indian professionals in skilled occupa‑ tions,with a quota of 5,000 vi‑ sas at any given time and a stay of up to three years

- India’s Intellectual Property to be accorded recognition

- Fast track mechanism for im‑ ports used for export manufac‑ turing, CustomsProcedure and Trade Facilitation ‑ This mod‑ ernizes customs procedures to ensurepredictability, transpar‑ ency and consistency in trade between trade partners

- The FTA offers opportunities for bothsides to engage in co‑ operation and collaborative activities in various thematic agricultureand non‑agriculture areas of interest

- Sector‑wise, the FTA is expect‑ ed to boost medical devices and pharma through faster reg‑ ulatory process

To conclude….

The strategic benefits of an India– New Zealand FTA are multifaceted and critical for strengthening In‑ dia’s engineering export base. The FTA will significantly improve price competitiveness for high‑potential sectors, enabling Indian exporters to offer cost competitive prod‑ ucts in New Zealand’s market. The agreement will also foster market diversification, reducing India’s dependence on traditional destina‑ tions like the US, EU, and Mexico— markets increasingly constrained by protectionist measures such as Section 232 tariffs, Mexico’s new duties on 1,400 products, and the EU’s CBAM and safeguard actions.

India’s exports to New Zealand has been growing in the last few years. Implementing an India–New Zealand Free Trade Agreement (FTA) has the potential to further boost the current trend. Projections in‑ dicate that exports could almost double by 2028, largely due to tariff elimination and enhanced market access. These measures would facil‑ itate new trade opportunities while strengthening India’s competitive‑ ness within the Oceania region.

India has signed a series of major Free Trade Agreements (FTAs) with global economies, strengthening its position in international trade and opening new markets for Indian businesses

• Comprehensive Economic and Trade Agreement (CETA):

With United Kingdom in 2025. CETA provides an unprecedented duty‑free access to 99% of India’s exports to the UK, covering nearly 100% of the trade value, benefiting sectors such as textiles, leather, marine products, gems, engineering goods, chemicals, and auto components.

- Notably, the agreement goes beyond goods and addresses services, a core strength of India’s economy. India exported over US$ 19.8 billion in services to the UK in 2023, and CETA promises to expand this further.

- Additionally, in a first by UK, mobility for professionals across IT, healthcare, finance, and education is being eased with CETA. This offers streamlined entry for contractual service suppliers, business visitors, intra‑corporate transferees, independent professionals.

- Another major breakthrough is the Double Contribution Convention‑ that will save Indian firms and workers ₹4,000+ crore by removing the need for dual social security contributions.

First FTA with four developed European nations:

- India signed a trade and economic partnership agreement with the EFTA countries‑ Switzerland, Norway, Iceland, and Liechtenstein‑ in 2024. The agreement improves market access for Indian pharmaceuticals, engineering goods, and services, backed by strong investment commitments, including USD 100 billion in investment and the creation of one million jobs in India.

• Economic Cooperation and Trade Agreement (ECTA)

with Australia was concluded by India in 2022, eliminating or reducing tariffs on most traded goods. The agreement has opened the Australian market to Indian textiles, pharmaceuticals, chemicals, and agriculture.

• Comprehensive Economic Cooperation and Partnership Agreement (CECPA):

With Mauritius in 2021. In Africa, India signed its first trade pact with the continent that enables easier market access for Indian exporters while strengthening Mauritius’ role as a gateway to African markets.

Besides these concluded agreements, several major economies are currently engaged in active negotiations with India to deepen trade and investment ties through FTAs and comprehensive economic partnerships.

LIST OF AGREEMENTS/ ONGOING DISCUSSIONS WITH NATIONS

- India and Israel signed the Terms of Reference for an FTA in November 2025. The proposed pact is expected to deepen cooperation in sectors such as fintech, agri‑tech, artificial intelligence, quantum computing, machine learning, pharmaceuticals, space and defence.

- India and the United States continue discussions on a bilateral trade agreement, with rounds of talks held in 2025. Under the ambitious “Mission 500”, both countries aim to more than double US‑India trade to $500 billion by 2030 to be achieved by deepening the trade relationship across multiple sectors.

- India is also in discussion with European Union (EU) for an FTA. Technical discussions on key chapters of the FTA such as market access for goods, rules of origin, services, technical barriers to trade, trade and sustainable development etc. took place in December 2025.

- Discussions for the ASEAN‑India Trade in Goods Agreement (AITIGA) is also underway, which holds potential to unleash the full economic potential of the member countries and further strengthen regional cooperation.

- India‑Australia Comprehensive Economic Cooperation Agreement (CECA) negotiations are advancing, covering a wide range of areas including goods, services and mobility, digital trade, rules of origin, legal and institutional provisions, environment, labour, and gender, bringing greater understanding for convergence in the remaining provisions.

- India and Mexico meetings have been centered on strengthening bilateral trade and investment relations, with discussions focused on expanding trade, investment, expanding economic cooperation, fostering business collaborations, and exploring opportunities across diverse sectors.

- With Canada, India continues discussions on a Comprehensive Economic Partnership Agreement, supported by agreed terms of reference. The proposed agreement aims to raise bilateral trade to around $50 billion by 2030 through tariff reductions and clearer frameworks for services and investment.

- India is actively negotiating an FTA with the Gulf Cooperation Council (GCC) and exploring a similar arrangement with Qatar, with the objective of strengthening ties across trade, energy, investment, and security.

Looking back at a year marked by a capricious and discriminatory use of trade policy instruments, the following trends stand out.

Reciprocal tariffs came and stayed:

Reciprocal tariffs came and stayed: True to his campaign promise, President Donald Trump announced reciprocal tariffs on “Liberation Day.” With some modi‑ fications, several exceptions and ex‑ emptions, the reciprocal tariffs were implemented in August. The power of the President to impose recipro‑ cal tariffs has since been challenged before the United States Supreme Court. However, the fact that some trade deals (US‑South Korea, for ex‑ ample) have in‑built provisions for protection against potential substi‑ tute tariffs (under section 232, for example) indicates acceptance of the fact that unfair trade policy uni‑ lateralism set in motion by the US may be here to stay.

The much‑feared, widespread re‑ taliation by other countries has not been evident thus far. Mexico’s announcement, earlier this month, that it will impose up to 50 per cent tariffs on a broad range of imports from its non‑free‑trade agreement trade partners (in Asia, effectively the non‑Comprehensive and Pro‑ gressive Agreement for Trans‑Pacif‑ ic Partnership (CPTPP) trade part‑ ners such as Thailand, Indonesia, South Korea, India and China) could spur a trend of unilateral, retaliato‑ ry trade policy action from affect‑ ed countries. This is especially so as the World Trade Organization (WTO), whose primary objective is to promote freer and fairer trade, has so far been a quiet bystander.

US trade deals happened, unravelled, happened again:

The US is redefining the trade agree‑ ment landscape with its trade deals. Finalised under Executive Orders, bilateral trade deals negotiated by the US have largely been non‑re‑ ciprocal in nature. Reduction in re‑ ciprocal tariffs by the US has been made conditional upon partner country commitments in areas oth‑ er than trade and concessional mar‑ ket access provisions. Since these trade deals are not legally binding, they are also being frequently un‑ done by the US. Eg: The US‑China trade deal, had several false starts, first in Geneva in May and then in London in June. A framework deal was finalised only at the end of October after several months of negotiations. This framework deal includes, inter alia, a reduction in reciprocal and the so‑called fentan‑ yl tariffs in return for a pause from China on export controls on rare earth elements (REEs) and assured purchase of soybeans. However, the concessions have been extended for only one year, reflecting a possi‑ bly short‑lived US‑China trade truce with significant unpredictability.

The US‑Japan trade deal was an‑ nounced in July but it unravelled in the face of implementation am‑ biguities regarding the stacking of Most‑Favoured Nation tariffs with reciprocal tariffs. The provision relating to a ceiling of 15 per cent tariff on US imports from Japan came through only in September, although with retrospective effect. The US‑European Union (EU) deal, accomplished in July, has been un‑ der constant threat of unravelling, with the US openly expressing its concerns over what it considers “discriminatory” regulations impacting American tech companies operating in the EU.

Pax silica: New alliance for GVC diversification:

The glob‑ al value chain (GVC) diversifica‑ tion process, which has long been in motion, acquired a new kind of salience with China’s worldwide im‑ plementation of export restrictions on REEs. In response to Trump’s tar‑ iffs, China enforced export restric‑ tions on REEs and related technol‑ ogies and equipment (magnets) in two phases — in April and October. Given China’s near‑monopoly hold on REE processing capabilities, the export control measures had a crip‑ pling effect on major defence, ener‑ gy and automobile firms in the US. In an attempt to secure the supply chain from critical mineral mines to semiconductors to frontier artificial intelligence (AI) models, the US has initiated

China remains the top global exporter:

Data for the first 11 months of 2025 shows that despite being confronted with numerous challenges — including multiple, overlapping high tariffs and tech barriers imposed by the US and do‑ mestic market limitations — China continues to be the largest export‑ er in the world with an increasing proportion of high‑tech, AI and sus‑ tainability‑driven products in its ex‑ port basket. Asean remains the top importer for China followed by the US, though with a lower share than in previous years.

Asean also continues to be the pre‑ dominant indirect trans‑shipment route for Chinese exports to the US. The lack of well‑defined rules of origin (RoOs) has clearly rendered the higher tariffs announced by the US ineffective (40 per cent in the trade deal with Vietnam, for exam‑ ple) on goods rerouted from China. While the new 50 per cent tariffs announced by Mexico on imports from Asian countries will block the trans‑shipment channel for some Asean members (Thailand and In‑ donesia) from the start of next year, it will leave it open for those that are CPTPP members, such as Vietnam.

CPTPP --- The sought-after mega-regional trade agreement:

With diminished relevance of the WTO in its present form, the CPTPP seems to be emerging as an alternative platform for rules‑based trade. The CPTPP members decid‑ ed to commence the accession pro‑ cess for new members — Uruguay, followed by Indonesia, the Philip‑ pines, and the UAE in 2026. Trade and Investment Dialogues with Ase‑ an and the EU were also launched.

The shared high standard (WTO++) trade and investment commitments of the two blocs —the EU and the CPTPP — can provide potential convergence possibilities to create an appropriate rule‑book for global trade in the near future. If combined with flexible and extended cumu‑ lation of RoOs, the dialogue part‑ nerships can significantly enhance the scope for GVC integration, re‑ silience, and security for member economies. This would be hugely beneficial in a world likely to see continued and heightened trade policy uncertainty.

BOOSTING INDIA’S EXPORT COMPETITIVENESS

Indian Government has implemented a comprehensive set of policy and institutional measures to strengthen India’s export ecosystem.

Export Promotion Mission

The Export Promotion Mission, was approved on 12 November, 2025, with a total outlay of Rs.25,060 crore for FY 2025–26 to FY 2030– 31. The mission operates through two integrated sub-schemes, Niryat Protsahan and Niryat Disha. Niryat Protsahan focuses on improving access to affordable trade finance for MSMEs through a range of instruments. Niryat Disha focuses on non-financial enablers that enhance market readiness and competitiveness, such as export quality and compliance support, assistance for international branding, packaging and others.

Labour Reforms

Integration of 29 labour laws into four Labour Codes has streamlined compliance, enhanced industrial efficiency, and strengthened worker protection. The reforms provide export-oriented industries with simplified regulations, flexible hiring provisions, unified registrations and returns, and expanded social security coverage, while ensuring occupational safety and welfare. At the same time, workers benefit from universal minimum wages, timely and transparent wage payments, mandatory appointment letters, grievance redressal mechanisms, and comprehensive social security protection.

Next Gen GST 2.0 Reforms

Since 22 September 2025, Next Gen GST 2.0 reforms have come into effect. 90% provisional refunds for zero rated supplies and inverted duty structure claims are being provided on a system driven, riskbased basis. The removal of valuebased threshold limits for GST refunds on exports supports small exporters by enabling refund claims on low-value consignments. GST rate reductions across packaging materials, textiles, leather, wood, trucks, delivery vans, toys, and sports goods lower production, freight, and logistics costs, enhance export competitiveness, and support domestic manufacturing.

Further, revised place of supply rules for “intermediary services” enables Indian service exporters to claim export related benefits, while correction of inverted duty structures in textiles and food processing eases working capital pressures and reduces refund dependency.

Targeted Government Initiatives

Targeted government initiatives reduce costs, strengthen infrastructure, improve quality standards, and enhance export competitiveness. The Foreign Trade Policy 2023 provides incentivebased support, promotes market diversification, and enables closure of legacy authorisations, while the RoDTEP (Remission of Duties and Taxes on Exported Products) scheme reimburses embedded duties and taxes, with ₹58,000 crore disbursed up to March 2025.

Strengthening Export Ecosystems

Export ecosystems are being strengthened through the initiatives like Districts as Export Hubs which are making states and districts active players in trade. 734 districts have been identified with export potential while District Export Action Plans (DEAP) has been prepared for 590 districts. The role of Special Economic Zones is also significant in the trade promotion, as it recorded exports of ₹14.56 lakh crore in FY 2024–25.

Trade Infrastructure for Export Scheme (TIES)

Infrastructure and manufacturing competitiveness are being enhanced through the Trade Infrastructure for Export Scheme (TIES), PM GatiShakti, the National Logistics Policy. The Production Linked Incentive (PLI) scheme, launched in 2020 is boosting manufacturing across 14 sectors, has attracted ₹1.76 lakh crore investments, generated ₹16.5 lakh crore in output, and created over 12 lakh jobs by March 2025. Further support is being provided through ease of doing business reforms and digital trade platforms such as the National Single Window System, Trade Connect e‑Platform, E‑Commerce Export Hubs, and ICEGATE.

2026 POSSIBLE ROCKY YEAR FOR GLOBAL TRADE

The global trading system, which is finishing up one of its most trans‑ formational years of the past centu‑ ry, heads into another facing more challenges to stability and growth.

Merchandise trade across the world held up relatively well through 2025, even as US President Donald Trump started erecting a tariff wall around the world’s largest econo‑ my. Data cited by shipping industry veteran John McCown show global container volumes grew 2.1 per cent in October from a year earlier. Yet beneath the overall resilience area shifting undercurrents: The US saw an 8% contraction in inbound vol‑ umes, while imports into Africa, the Middle East, Latin America and In‑ dia all showed robust growth.

“World container supply chains have already begun to adapt and reconfigure trading patterns,” Mc‑ Cown wrote in a research note on Monday. After the US in 2024 saw a 15.2 per cent gain in container im‑ ports for the full year, “to say that the annual total for 2025 will be in diametric contrast is an understatement.”

Trump’s trade threats were among the chief reasons for the rewiring of shipments, according to Mc‑ Cown. If 2025 was the year of the tariff, he wrote in a LinkedIn post, then 2026 will be the year of tar‑ iff consequences. Other experts in recent weeks have said they an‑ ticipate more trade turmoil in the year ahead. The US, Canada and Mexico are about to start review‑ ing the North American free‑trade deal that took effect in 2020. The negotiations will take the three na‑ tions into “new territory” given the novelty of the provision allowing for an update after just six years, ac‑ cording to comments by US Trade Representative Jamieson Greer to lawmakers this month. Greer said the government received more than 1,500 responses during the public comment period ahead of the com‑ ing review.

“Many stakeholders expressed sup‑ port for the USMCA and many ex‑ plicitly called or the agreement to be extended,” Greer said. “At the same time, virtually all stakehold‑ ers also called for some sort of im‑ provement to the agreement.”

But any “improvement” for one of the three members of the trade bloc risks coming at the expense of another. And that sets the stage for a tough round of talks for the larg‑ est US trading partners, whose in‑ dustries are struggling amid Amer‑ ican import taxes. Ties are already strained between the US and Can‑ ada, after Trump terminated trade talks with the northern neighbor in October — in response to anti‑tariff ads featuring Ronald Reagan.

For container ships and other work‑ horses of global trade, the year ahead may bring two shocks that sound like welcome developments but could actually snarl global sup‑ ply chains in ways seen during the Covid pandemic, according to ex‑ perts including Lars Jensen, the CEO of the consultancy Vespucci Maritime.

The first change would be a return of the world’s cargo fleet to using the Red Sea, rather than the longer route around southern Africa that vessels have had to resort to for the past two years. Houthi attacks in the Red Sea have largely subsid‑ ed since the Gaza peace plan took effect in October, making the old route more appealing. Carriers in‑ cluding France’s CMA CGM SA and Denmark’s AP Moller‑Maersk A/S are already sending a small number of ships through. But a full return to the Red Sea and the Suez Canal shortcut between Asia and Europe will “flood the market with a lot more capacity” and create “massive port congestion issues in Europe,” Jensen said during a Flexport webi‑ nar in November.

The second blow could be more demand driven, according to Jen‑ sen. High on the White House’s list of 2025 accomplishments are trade deals with several major economies, most of which bent to Trump’s de‑ mands ranging from investment pledges to better market access for US exports. In exchange for their submissiveness, their goods were smacked with a tariff rate that was lower than the duty they would’ve gotten if they retaliated.

But these aren’t traditional, binding trade deals with enforcement provi‑ sions and fine print spelling out the rules, and there’s only a one‑year truce with China rather than a full agreement — leaving out the US’s most unbalanced trading relation‑ ship. That’s left concern that pacts could yet come undone, especial‑ ly given the potential for pressure from Beijing against any nation open to working with Washington at China’s expense. Even the UK has seen fresh difficulties crop up. Last week, Greer singled out the EU and India, saying that contentious talks aimed their respective trade deals are set to spill into the new year.

Among the biggest unknowns in trade circles heading into 2026 is a pending US Supreme Court ruling on the legality

© Copyright , All rights reserved. Design by Andreal