VOL. 18, ISSUE NO. 7 | October 2025

Focus

INTRODUCTION

India is one of the fastest growing economies of the world and is poised to continue on this path, with aspirations to reach high middle income status by 2047, the centenary of Indian independence. This pace in growth combined with rising incomes along with a boost in infrastructure spending and increased manufacturing incentives, has accelerated the growth ofautomobile industry.

The Indian automotive industry has seen significant growth and is currently valued at over US$ 238 billion.. It contributes approximately 6.8% to India’s GDP and 14-15% to the GST. The industry is a major player in global markets, particularly in segments like Passenger Cars, Utility Vehicles, Vans and two Wheelers is expected to reach US$300 billion by 2026. The sector isalso expected to become the third largest in the world by 2030

This momentous in the Indian automobile sector has led India to develop and strengthen its expertise in automobiles and auto components. Thus the Indian automobile industry has had a considerable impact on the auto component industry.

India’s auto component industry is an important sector driving macroeconomic growth and employment. The industry comprises players of all sizes, from large corporations to micro entities, spread across clusters throughout the country. Due to the high development prospects in all vehicle industry segments the Indian auto components industry is projected to record US$ 200 billion in revenue by 2026the aftermarket of the industry is expected to reach US$ 30 billion.( Source IBEF)

By FY28, the Indian auto industry aims to invest Rs. 58,000 crore (US$ 7 billion) to boost localization of advanced components like electric motors and automatic transmissions, reducing imports and leveraging ‘China Plus One’ trend.

The auto component industry in India is composed of organized and unorganized sector. The organized sector refers to original equipment manufacturers (OEMs) and is engaged in the manufacture of high-value precision instruments. Whereas, the unorganized sectors comprise of low-valued products catering to after-market services. The growth of global original equipment manufacturers’ (OEM) sourcing from India & the increased indigenisation of global OEMs is turning India into a preferable designing and manufacturing base. This leads to 8% of India’s R&D expenditure getting invested in the automotive sector.

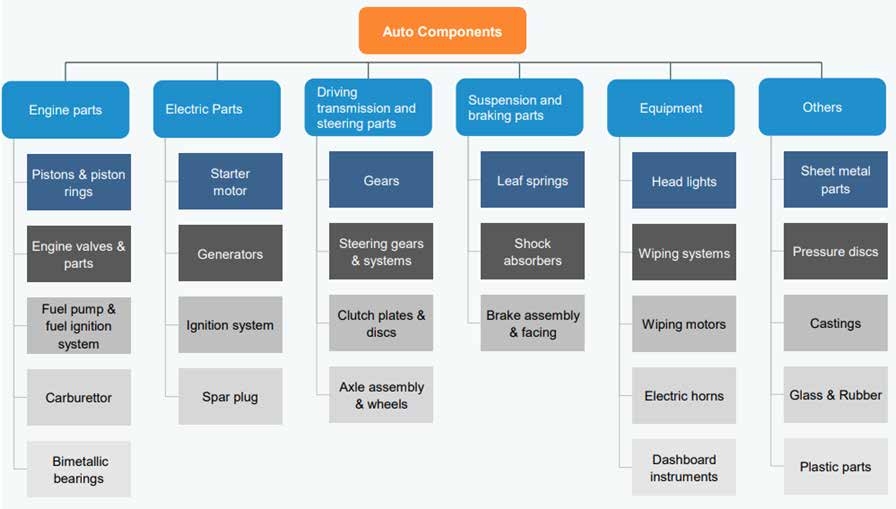

Various sub-sectors of the Auto components & parts industry in India are as follows:

I. ROBUST GROWTH OF INDIAN AUTO COMPONENTS & PARTS

- The automobile component industry turnover stood at Rs. 6.14 lakh crore (US$ 74.1 billion) during FY24, registering a revenue growth of 9.8% as compared to FY23.

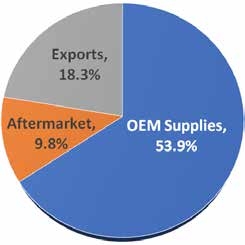

- Domestic OEM supplies contributed ~54% to the industry’s turnover, followed by domestic aftermarket (~10%) and exports (~18%), in FY24.

- The component sales to OEMs in the domestic market grew by 8.9% to Rs. 5.18 lakh crore (US$ 62.4 billion).

- During FY24, exports of auto components grew by 5.5% to US$ 21.2 billion. As per the Automobile Component Manufacturers Association (ACMA) forecast, automobile component exports from India are expected to reach US$ 30 billion by 2026. In FY22, India’s auto component Industry for the first time reached a trade surplus of US$ 700 million.

- The aftermarket for auto components grew by 10.0% during FY24 reaching Rs. 9.38 lakh crore (US$ 11.3 billion).

II. EXPORT GROWTH

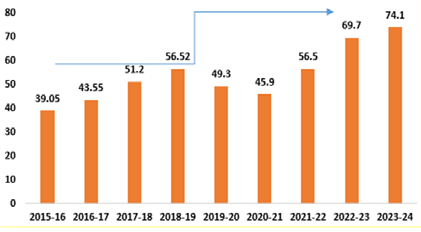

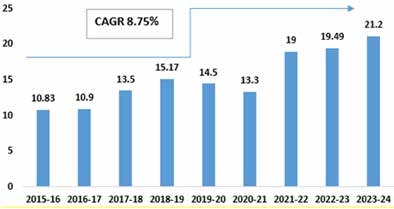

- Exports of automobile componentsfrom India increased, at a CAGR of 8.75%, from US$10.83 billion in FY16 to US$21.20 billion in FY23.

- During FY24, exports of auto components grew by 5.5% to US$ 21.2 billion. As per the Automobile Component Manufacturers Association (ACMA) forecast, automobile component exports from India are expected to reach US$ 30 billion by 2026. In FY22, India’s auto component Industry for the first time reached a trade surplus of US$ 700 million

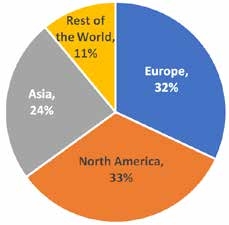

- In FY24, North America, which accounts for 32% of total exports, increased by 5%, while Europe and Asia, which account for 33% and 24% of total exports, increased by 12% and growth for Asia remained flat, respectively. The key export items included drive transmission and steering, engine components, body/chassis, suspension and braking etc.

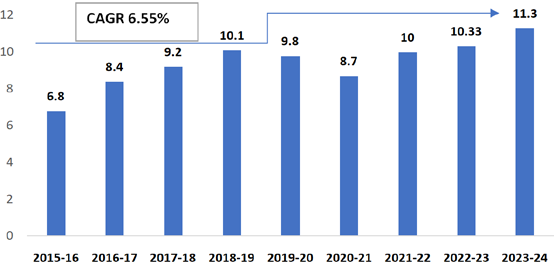

Value of Auto Component Export (US$ billion)

Share of Export by Geography (FY24)

INDIA’S TOP FIVE EXPORT DESTINATIONS IN THE LAST 3 YEARS

USA ranks as the numero uno destination of India’s export of Auto components & parts importing 27 percent of India’s export of the same in 2023. The share of other top nations are Turkey (6.7%), Germany (5.6%), Mexico (5.4%) and Brazil (4%).

Table No.1: India’s top 5 Export Destinations in the last 3 years

| Values in US$ million | |||

|---|---|---|---|

| Top 5 Export Destinations of India | 2021 | 2022 | 2023 |

| World | 5969.4 | 6461.0 | 6684.0 |

| USA | 1586.5 | 1737.4 | 1777.8 |

| Turkey | 360.0 | 359.5 | 447.1 |

| Germany | 339.0 | 333.8 | 374.1 |

| Mexico | 296.0 | 295.7 | 361.7 |

| Brazil | 251.4 | 322.6 | 264.5 |

GLOBAL MAJOR SUPPLIERS OF AUTO COMPONENTS & PARTS IN THE WORLD MARKET AND VIZ-A-VIZ INDIA’S RANK IN 2023

Table No.2: India’s rank as a global supplier of Auto components & Parts in 2023

| Rank | Global suppliers | Share in value in world's exports, % in 2022 |

|---|---|---|

| 1 | Germany | 14.5 |

| 2 | China | 11.6 |

| 3 | USA | 10.3 |

| 4 | Mexico | 8.3 |

| 5 | Japan | 6 |

| 6 | Korea Rep | 4.4 |

| 7 | Czech Republic | 3.8 |

| 8 | Poland | 3.6 |

| 9 | France | 3.3 |

| 10 | Italy | 3.2 |

| Rank | Global suppliers | Share in value in world's exports, % in 2022 |

|---|---|---|

| 11 | Canada | 3 |

| 12 | Spain | 2.6 |

| 13 | Hungary | 1.9 |

| 14 | Belgium | 1.8 |

| 15 | Thailand | 1.8 |

| 16 | Slovakia | 1.7 |

| 17 | Romania | 1.7 |

| 18 | Turkey | 1.6 |

| 19 | India | 1.5 |

Source: ITC Trade Database

AFTERMARKET GROWTH

- The aftermarket for auto components grew by 10.0% during 2023-24 reaching Rs. 93,886 crore (US$ 11.3 billion)

- By 2028, the domestic automotive aftermarket segment in India is expected to reach US$14 billion.

- Aftermarket turnover in Aftermarket turnover increased at a CAGR of 6.55% from US$ 6.80 billion in FY16 to US$ 11.30 billion in FY24 and is expected to reach US$ 32 billion by FY2026.

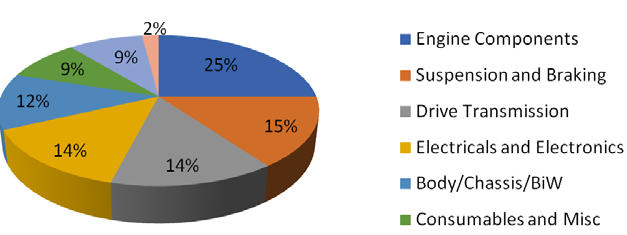

- The ‘Drive Transmission and Steering’ product category accounted for 21% of the aftermarket share followed by ‘Engine Components’, and ‘Electricals and Electronic Components’ with 19% and 18%, respectively.

- To support local auto parts suppliers, the auto component sector has tied up with Tesla to manufacture electric vehicles in August 2021.

Value of Aftermarket Turnover (US$ billion)

Product-wise Share in Aftermarket Turnover (FY22)

GOVERNMENT INITIATIVES

From the above table no.2, we see that India’s ranks as the 17th global supplier of auto components & parts globally which is not a very significant rank, catering 1.6% of the total global supply of auto components & parts.

In order to make a significant mark in the global arena and help India’s automobile sector embark on a road to success, the Govt. has been providing a comprehensive support to the Automobile and Auto Components & Parts sector. The Government of India’s Automotive Mission Plan (AMP) 2006-26 has been instrumental in ensuring growth for the sector. The favourable policy measures aiding growth are as follows:

1. Union Budget 2023-24

- The Government has reaffirmed its commitment towards EVs and its mission for 30% electric mobility by2030.

- Budget announced customs duty exemption on the import of capital goods and machinery required for the manufacture of lithium-ion batteries that typically power EVs.

- BHEL has successfully manufactured and tested India’s highest rating 500 MVA 400/220/33 kV Auto Transformer, at the National High Power Test Laboratory (NHPTL) at Bina in Madhya Pradesh- a new benchmark in the global transformer industry..

- The ‘Drive Transmission and Steering’ product category accounted for 21% of the aftermarket share followed by ‘Engine Components’, and ‘Electricals and Electronic Components’ with 19% and 18%, respectively.

2. National Electric Mobility Mission Plan (NEMMP) 2020

- NEMMP aims to bring the transformational paradigm shift in the Automotive and Transportation industry by promoting hybrid and electrical mobility in India.

- There has been a cumulative outlay of USD 2.15 Bn for building such a roadmap. It is a composite scheme involving demand-side incentives to facilitate the acquisition of hybrid/electric vehicles along with the provision of supply-side incentives.

3. National Automotive Testing and R&D Infrastructure Project (NATRiP)- the largest and most significant initiative by the Government of India, in the Automobile component industry in India

- The chief aim of the project is:

- To generate core global competencies - state-of-art testing and R&D infrastructure.(7 R&D centres - Chennai, Manesar, Indore, Raebareli, Silchar,Ahmednagar, Pune)

- To enable seamless integration by driving the automobile component industry in India into global automotive excellence.

- A total of USD 573 Mn investment has been done to adopt and implement global performance standards.

- The key focus lies in providing low-cost manufacturing and product development solutions.

4. Department of Heavy Industries & Public Enterprises

- Created a US$ 200 million fund to modernize the auto components industry by providing interest subsidy on loans & investments in newplants & equipment.

- Provided export benefits to intermediatesuppliers of auto components against Duty- Free Replenishment Certificate (DFRC).

5. Automotive Mission Plan 2016-26 (AMP 2026)

- AMP 2026 targets a fourfold growth in the automobile sector in India, which includes manufacturers of automobiles, auto components & tractors over the next 10 years. The government’s AMP 2016-26 will help the automotive industry grow and will benefit the economy in the following ways:

- The auto industry’s GDP contribution will rise to over 12%.

- Additional ~65 million direct and indirect jobs will be created.

- End-of-life policy will be implemented for old vehicles.

6. FAME Scheme

- Aimed at incentivising all vehicle segments - two wheelers, three wheelers, four wheelers, LCVs and buses. It covers hybrid & electric technologies like Mild Hybrid, Strong Hybrid, Plug in Hybrid & Battery-Electric Vehicles.

- In March 2023, centre approved US$ 97.85 million for 7,432 public fast charging stations under the FAME SchemePhase II.

- In February 2019, the Government of India approved FAME-II scheme with a fund requirement of US$ 1.39 billion for FY20-22.

- Department of Heavy Industries has sanctioned 2,636 charging stations in 62cities across 24 States/UTs under FAME II.

7. Production-Linked Incentive (PLI) Scheme in the Automobile and Auto Components (2021)

- Outlay of USD 3.5 Bn for the automobile sector proposes financial incentives of up to 18% to boost domestic manufacturing of advanced automotive technology products andattract investments in the automotive manufacturing value chain.

8. Production Linked Incentive (PLI) Scheme for Advanced Chemistry Cell (ACC) Battery Storage (2021)

- Aims at achieving manufacturing capacity of 50 GWh of ACC for enhancing India’s manufacturing capabilities with a budgetary outlay of USD 2.3 Bn. This scheme was oversubscribed by 2.6 times (130 gwh).

9. FDI Policy

- 100% Foreign Direct Investment (FDI) is allowed under the automatic route in the Automobile component industry in India, subject to all the applicable regulations and laws.

10. Vehicle Scrappage Policy

- The Vehicle Scrappage Policy, launched on August 13, 2021, is a government-funded programme to replace old vehicles with modern & new vehicles on Indian roads. The policy is expected to reduce pollution, create job opportunities and boost demand for new vehicles.

11. Battery Waste Management Policy

- The Battery waste management rule, published in August 2022 is a government programme to help reduce the dependency on new raw materials. The policy is expected to save natural resources, create new business & job opportunities.

12. State Incentives

- Apart from the mentioned, each state in India offers additional incentives for industrial projects. Incentives are in areas like subsidized land cost, relaxation in stamp duty exemption on sale and lease of land, power tariff incentives, concessional rate of interest on loans, investment subsidies, tax incentives, backward areas subsidies and special incentive packages for mega projects. Few examples are: Andhra Pradesh, Gujarat and Jharkhand.

VI GROWTH DRIVERS

A. DEMAND-SIDE DRIVERS

- Growing working population and expanding middle class are expected to remain the key demand drivers. India is the fifth-largest automobile market globally.

- Increase in investment in road infrastructure.

- With the Self-Reliant India mission, the auto industry is looking to half its Rs. 1 trillion (US$ 13.6 billion) worth of auto component imports over the next 4-5 years. This will provide significant opportunities for existing and new auto components players to scale up..

B. SUPPLY-SIDE DRIVERS

- A cost-effective manufacturing base keeps costs lower by 10-25% relative to operations in Europe and Latin America.

- Second-largest steel producer globally, hence a cost advantage.

- India has a competitive advantage in auto components categories such as shafts, bearings and fasteners due to large number of players. This factor is likely to result in higher exports in coming years.

- India is emerging as a global auto component sourcing hub due to its proximity to key automotive markets such as ASEAN, Europe, Japan and Korea.

- Technological shift and focus on R&D- India retained the 40th position in Global Innovation Index among the top innovative economies globally as per Global Innovation Index (GII) 2023.

C. POLICY SUPPORT

- Visionary Govt. policies: Policies such as Automotive Mission Plan 2016-26, Faster Adoption & Manufacturing of Electric Hybrid Vehicles (FAME, April 2015) and NMEM 2020 are likely to infuse growth in the auto component sector of the country are likely to infuse growth in the auto component sector of the country.

- PLI schemes has been extended to the automobile sector with an aim of creating an incremental output of Rs. 2,31,500 crore (US$ 31.08 billion).

- The Government announced National Mission on Transformative Mobility and Battery Storage based on phased manufacturing program (PMP) until 2024.

- Lower excise duty on specific parts of hybrid vehicles.

- Establishing special auto parks & virtual SEZs for auto components.

VII INVESTMENT OPPORTUNITIES IN ENGINEERING PRODUCTS

The Indian automobile sector received a cumulative equity FDI inflow of about US$ 36.268 billion between April 2000 - March 2024. As per Economic Survey 2023-24, the production linked incentive scheme (PLI) for automobile and auto components has so far attracted a proposed investment of Rs. 67,690 crore (US$ 8.18 billion).With the launch of the “Make in India” initiative, the Government isexpected to vitalise substantial investment in the auto components sector.

Some of the Government Support in infrastructure and investment are mentioned below:

Under Electric Mobility Promotion Scheme 2024 government aims to support 3,72,215 EVs including e-2W (3,33,387) and e-3W (38,828 including 13,590 rickshaws & ecarts and 25,238 e-3W in L5 category).

Under phase-II of FAME India Scheme, subsidy amounting to US$ 696.8 million (Rs. 5790 crores) has been awarded to EV manufacturers on sale of 13,41,459 number of electric vehicles till January 31, 2024.

Ola Electric IPO to be the first auto company in India to launch an IPO in over two decades (20 years). It has an expected size of Rs. 8,500 crore (US$ 1.01 billion).

In April 2023, Power Finance Corporation Ltd (PFC) approved a Rs. 633 crore (US$ 76.39 million) loan for 5,000 passenger EVs and 1,000 cargo EVs.

In March 2023, the Central Government sanctions Rs. 800 crore (US$ 72.41 million) under FAME India Scheme Phase II to Indian Oil (IOCL), Bharat Petroleum (BPCL), and Hindustan Petroleum (HPCL), for setting up 7,432 public fast charging stations across the country. (Source IBEF Reports).

The new opportunities in the sector are as follows:

- New technological changes in Engine & Exhaust partsinclude introduction of turbochargers and common rail systems.

- The trend of outsourcing may gain traction in this segment in the short to medium term.

- Share of replacement market in subsegments such as clutches is likely togrow due to rising traffic density..

- The entry of global players is expectedto intensify competition in subsegments such as gears & clutches.

- Suspension & braking parts segment is estimated to witness high replacement demand with players maintaining a diversified customer base in thereplacement & OEM segments besides the export market.

- The entry of global playersis likely to intensify competition insub-segments such as shock absorbers.

- Metal part manufacturers are likely to benefit from rising demand for body & chassis, pressure die castings, sheet metal parts, fan belts, and hydraulic pneumatic instruments, primarily in the two wheelers industry.

- Prominent companies in this business are constantly working towardsexpanding their customer base.

- In October 2021, Sona BLW Precision Forgings Limited, through its wholly owned subsidiary company, Sona Comstar eDrive Private Limited (Sona Comstar), entered a collaboration agreement with IRP Nexus Group Ltd., Israel, to develop, manufacture and supply magnet-less drive motors and matching controller systems for electric two and three-wheelers.

VIII INDIA IS POISED TO EMERGE AS AN OUTSOURCING HUB

- In March 2024, Tata Motors Group has signed a facilitation Memorandum of Understanding (MoU) with the Government of Tamil Nadu to explore setting-up of a vehicle manufacturing facility in the state. The MoU envisages an investment of Rs. 9,000 crores (US$ 1,081.6 million) over 5-year.

- Tata Motors, in April 2024, announced the inauguration of a new commercial vehicle spare parts warehouse in Guwahati.

- In December 2023, Tata Passenger Electric Mobility Ltd. (TPEM) and Bharat Petroleum Corporation Limited (BPCL) signed an MoU to jointly establish 7,000 public charging stations nationwide to enhance customer satisfaction.

- In April 2024, Maruti Suzuki India Limited, commissioned another vehicle assembly line at its Manesar facility.

- In January 2024, at the Vibrant Gujarat Global Summit, Maruti Suzuki announced the investment plans in Gujarat with a New Greenfield plant and a fourth line in SMG.

- In December 2023, Maruti Suzuki India Limited entered into an agreement with the Government of Haryana to establish the second Japan-India Institute for Manufacturing (JIM) as part of its corporate social responsibility (CSR) initiative. The company will invest Rs. 5.8 crore (US$698 thousand) to upgrade the existing ITIKansala into a JIM.

- In May 2023, Maruti Suzuki India plans to invest over US$ 5.5 billion to double capacity by 2030.

- The Renault-Nissan alliance is stepping up its investments in India plans to invest US$ 600-700 million at its Chennai-based facility to step up platform localisation and improve sophistication levels in manufacturing.

- In July 2023, Renault Nissan to invest Rs. 1.4 crore (US$ 1,68,762.86) to upgrade infrastructure at eight schools near Chennai.

- In February 2023, Nissan and Renault plan to invest US$ 600 million in India over the next 3-5 years to expand their market share in passenger cars and electric vehicles.

- In July 2021, Nissan initiated a feasibility study to manufacture electric vehicles in India. If the study is positive when it is concluded in a year, Nissan may end up producing EVs in India for local sales and exports.

- In February 2024, company has announced it will invest over Rs. 32,000 crore (US$3.85 billion) from 2023 to 2033 in expandingits EV range and enhancing its current car and SUV platforms.

- In January 2024, Hyundai Motor India Limited announced Rs. 6,180 crore (US$ 743.8 million) investment plans in the state of Tamil Nadu including Rs. 180 crore (US$ 21.7 million) towards a dedicated ‘Hydrogen Valley Innovation Hub,’ in association with IIT- Madras.

- In January 2024, Hyundai Motor India Ltd. finalized the acquisition and transfer of specified assets at General Motors India’s Talegaon Plant in Maharashtra and inked an MoU with the Government of Maharashtra committing to an investment of Rs. 6,000 crore (US$ 722 million) in the state.

- In May 2023, Hyundai Motor announced that it will invest over Rs. 20,000 crore (US$ 2.41 billion) in Tamil Nadu over the next 10 years to bolster its EV production.

CONCLUSION

India’s automobile industry has been propelled forward by a growing consumer class, improved ease of doing business, expanding infrastructure, and other favorable factors. Over the years, the industry has undergone a paradigm shift, creating new verticals and opportunities for auto component manufacturers. The future of the auto OEM and auto component industry is being shaped by multiple trends, policies, and disruptions. Keeping pace with these changes, India’s auto component industry has been flourishing. The Indian automotive OEM industry is already in a strong position and is at the forefront of many segments globally. However, despite its impressive achievements, its share in global exports remains modest. Therefore, it is crucial for each auto component player to aggressively pursue export opportunities that are most suited to them. Significant opportunities lie ahead, driven by India’s expected strong economic progress. Auto component manufacturers need to capitalize on these opportunities to leap forward and achieve global eminence.

EEPC India has a dedicated panel on Auto Components and partakes in leading Auto Industry show - Automechanika in Dubai and Frankfurt played a pivotal role as the Coordinating Agency for Bharat Mobility Global Expotheleading global mobility show in India for two editions- 2024 and 2025 by facilitating industry collaboration and ensuring seamless participation from key stakeholders across the global mobility ecosystem. Hosted by Industry associations and supported by Ministry of Commerce & Industry, Government of India, Bharat Mobility Global Expos in 2024 and in 2025 emerged as one-of-its kind confluence covering the entire mobility ecosyste.

AUTOMECHANIKA DUBAI 2025

9 – 11 December 2025, Dubai, UAE

Automechanika Dubai is the MEA region’s largest international trade exhibition for the automotive aftermarket industry. It serves as a vital platform for professionals to connect, source products, and discover the latest innovations. The event continues to fuel growth and foster collaboration within the global automotive aftermarket sector.

Automechanika Dubai is the largest international automotive aftermarket trade show in the Middle East, Automechanika Dubai acts as the central trading link for markets that are difficult to reach connecting the wider Middle East, Africa, Asia and key CIS countries.

Economic scenario of UAE

The economic performance of the UAE has been robust with non-oil sectors and structural reforms playing the role of strong driving force. Economic diversification towards non-oil sectors contributed significant share of UAE’s GDP in the recent years. Key growth areas include transportation, financial services, construction and information and communication technology. Increasing investment in renewable energy and technology sectors are expected to further boost the economy. Overall there is a positive outlook for the country in the coming years underpinned by strategic diversification and investment initiative. The economy rebounded well since its negative growth during the COVID-19 crisis and is expected to stabilise. In 2024, UAE’s real GDP growth rate reached around 3.8% and is expected to reach 4% in 2025 as per IMF

The below figure indicates the Real GDP growth rate of UAE in the last five years:

UAE is an important trading partner for India. The two countries share a Comprehensive Economic partnership Agreement (CEPA) which completed three years after its signing in February 2022. Since the signing of the agreement, the bilateral trade between the two countries have increased significantly. As per latest data available, since the signing of CEPA, bilateral merchandise trade has nearly doubled from USD 43.3 billion in FY 2020-21 to USD 83.7 billion in 2023-24

In engineering sector, UAE has been one of the top three export destinations for India. In 2024- 25, India’s engineering exports to the UAE stood at USD 8.3 billion which is 40.3% higher than the same period last year.

The product profile of Automechanika Dubai 2025 consists of Parts & Components, Electrics & Electronics, Connectivity & Autonomous Driving, Accessories & Customising, Tyres & Batteries, Car Wash, Care & Detailing, Oils, Lubricants & Fuels, Diagnostics & Repair, Body & Paint, Digital Solutions & Services and other related products.

In auto-components sector, India’s exports to UAE stood at USD 291 million in 2024-25, which is 29.2% greater than the same period last year. India’s share in UAE’s import basket in auto components sector is around 2.6% and it ranks within the top 10 suppliers to the UAE.

Opportunity for Indian Auto components and parts in UAE

UAE is home to the global leaders in the automobile market and is also a leading hub of automobile export and re-export especially in the Middle East and North Africa region. Additionally Dubai being home to significantly higher income class is also a significant market for automobile. Already a number of big auto and allied manufacturers have established themselves in Dubai to cater to the international and local demand. Ease of doing business conducive policies, available industrial space and geographical location have also driven these companies to settle in Dubai. Given this background, UAE has the potential to become one of the most sought-after market for Indian auto component manufacturers and the FTA has paved the way further. Hence events such as Automechanika Dubai are extremely important for the Indian auto part exporters.

© Copyright , All rights reserved. Design by Andreal