VOL. 18, ISSUE NO. 5 | August 2025

Focus

Bringing a revolution in the Pharma and Lab equipment Manufacturing sector,India hostsPharma Machtech Expo 2025 and LabNext Expo 2025. EEPC India Chairman Pankaj Chadha said around 35% of pharmaceutical machinery and equipment produced in the country are exported. “India is rapidly emerging as a leading manufacturer and exporter of high-quality laboratory equipment. From precision glassware to cutting-edge analytical devices, Indian products are meeting global standards at cost-effective prices,” Mr Chadha noted.

Seeking to tap the immense opportunity in the pharmaceutical equipment sector, EEPC India has announced two premier shows, Pharma Machtech Expo 2025 and LabNext Expo 2025, which will be co-located with iPhex 2025 to beheld from September 4-6 at Bharat Mandapam, New Delhi.

“It will create an unprecedented opportunity to discover the latest innovations and the most advanced, high-quality machinery that are shaping the future of pharmaceuticals. By bringing together the full spectrum of the industry, we aim to accelerate the development of world-class quality pharmaceutical products and services,” Mr Chadha said about the upcoming mega shows.

Pharma Machtech

This show will showcase the entire supply chain of pharmaceutical machinery and equipment, including pharmaceutical packaging materials and equipment, process plants and machinery, monitoring and inspection, cold chain, clean rooms, and quality control technology, as well as the latest innovations in sustainability, software, automation, and startups.

Lab Next Expo

This show will showcase laboratory and analytical instruments, scientific instruments, biotechnology and life sciences, lab fine chemicals and reagents, process instruments, as well as the latest innovations in laboratory automation, software, analytical testing, calibration, and research instruments, including diagnostics and point-of-care testing, among others.

In addition to the above, two key conferences on topics covering regulation and exports in Pharma Machinery and Industry 5.0 are also scheduled during the pharma trade shows.

As per industry estimates: India’s laboratory equipment market is projected to reach $3.35 billion by 2030, growing at a 6.7% CAGR.

Pharma MachTech Expo 2025 and Labnext Expo 2025 offer:

- Opportunities to connect with key decision-makers

- Hold B2B meetings

- Buyer-seller meets

- Roundtables

Pharmaceutical & Lab Machinery: Industrial Overview

The Pharmaceutical industry in India is the 3rd largest in the world in terms of volume and14th largest in terms of value. The Pharma sector currently contributes to around 1.72% of the country’s GDP. Pharmaceutical is one of the top ten attractive sectors for foreign investment in India.

Visible Trends showing interest of Indian machinery manufacturers:

- Machine makers are going for CNC machine to get quality output

- Using more and more gadgets in the machine, like, VFD, PLC etc.

- Many firms are getting ISO approval

- Importing of prototype machines

- Getting CF approvals for machines

- Collaboration and technology transfer

- Expanding to meet rising global demand.

- Investing in HRD by taking professional to meet the challenges of International market.

Pharmaceutical Machinery: Indian Market

Economic Scenario:

The Indian pharmaceutical industry is expected to maintain a steady growth rate of 8-10% in 2023 and is estimated to be worth USD 130 billion. Meanwhile, the global market size of pharmaceutical products is estimated to cross over the $1 trillion mark in 2023. The growth in this sector is likely to be supported by the government’s focus on healthcare, the rising trend of generics, and the increased investment in research and development. Therefore it provides tremendous scope for the machinery manufacturers to exploit the potential by providing necessary machinery by ensuring proper design, ease of user application, simple maintenance and also validation protocol for the new equipment that are essential for the pharmaceutical companies.

The sector this year was marked by a greater degree of collaboration between the government and industry, with both playing a pivotal role in helping the sector further strengthen its position in the global market. Owing to the COVID-19 pandemic, the entire landscape of the pharmaceutical industry has had a paradigm shift, with the collaboration between the government and the industry being increasingly seen in a positive light.This growth is likely to be supported by the government’s focus on healthcare, the rising trend of generics, and the increased investment in research and development. Despite geopolitical issues, India continued to supply medicines to over 200 countries, living up to its reputation as the ‘pharmacy of the world’.

Market Overview:

The Indian pharmaceutical machinery industry is currently catering to the segments of tableting, capsulation, powder processing, material handling, R&D equipment and instrumentation, coating, bulk drug plant installation etc.In India, there are around 800 pharmaceutical machine manufacturing and allied utility service units in the small and medium sector. Though only few companies have made a mark in the area of branded market, a majority of these units undertake job works and supply of custom-made machineries taking the location advantage of buyers.The manufacturing facilities in India are being upgraded to the standards of the regulated markets. Today, India has the highest number of FDA approved facilities outside USA.

Packaging technologies which show substantial potential for growth are horizontal and vertical form-fill-seal machines for different goods, be it solids, granules or liquids. Blister packing and Cartoning machines, form-fill-seal machines for flat-top-and -bottom models, bag-in-box systems, sterilization and filling technologies for vials and ampoules, as well as filling and sealing of metal containers are also technologies with rising local demand.

There are more than 350 facilities in India’s pharmaceutical-machine manufacturing industry, in categories like instrumentation and process control, lab equipment, pharma research and development (R&D) tools and techniques, pharmaceutical machinery, packaging material and machines, plant design and engineering, pharmaceutical process technology, and software.India’s pharmaceutical industry has approximately 3000 active pharmaceutical ingredient-manufacturing facilities, nearly 5000 formulation facilities, and 2000 other pharmaceutical facilities. Out of these, 300 facilities are in the medium to large range.

An increasing number of foreign pharmaceutical-machine manufacturers also have recognized India’s achievements and evolution in the industry. Indian machines are manufactured and used in accordance with international standards and do not hazard the inspection and approval of their facility. This is one of the many reasons that India has the most FDA-approved facilities in the world.

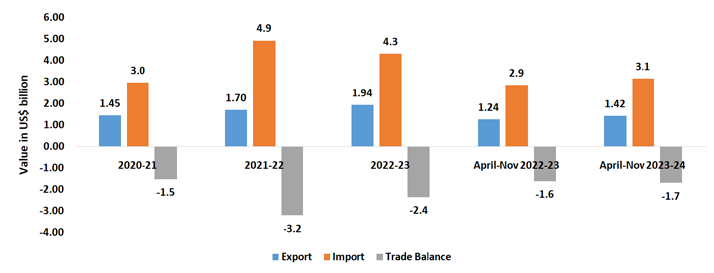

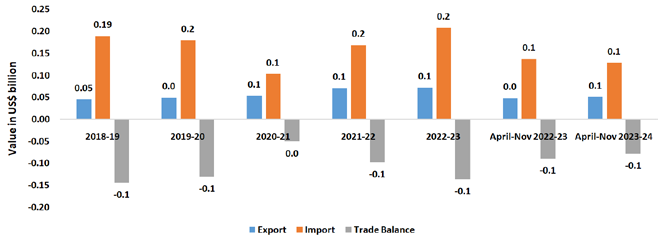

Trade Scenario of Indian Pharma Machinery Sector:

$25 billion of the value coming from exports..

Observation: The above figure depicts India’s overall trade scenario in pharma machinery segment during the last 3 years as well as the current fiscal. From the figure it is evident that exports of pharma machinery in India have increased during the last 3 years. The CAGR of exports during this time period registered16 percent whereas imports increased by 20 percent. Overall, India has a negative trade balance in this sector for the last three fiscal as well as during the current fiscal of April-Nov 2023-24.

Country-wise Analysis

Observations:

- Figure 10 above depicts the top importers of pharma machinery from India during 2022. USA is the top importer from India importing with a share of 23 percent in India’s total pharma machinery exports.

- It is followed by China, Germany, France, Brazil all of which have a share of 4 to 6 percent in India’s pharma machinery exports

- Together the top 5 export destinations account for more almost 42percent of India’s export basket

Figure 10: Share of Top export destinations for Pharma machinery export

Observations:

- Figure 11 depicts the top exporters of pharma machineryto India during 2022.

- China is the top exporter to India exporting with a share of19.1 percent in India’s total pharma machinery imports.

- It is followed by USA< Germany, Netherlands and Singapore all of which together contribute more than 41 percent share in India’s import basket

- Together the top 5 import partners account for 61.1 percent of India’s import basket

Figure 11: Share of Top Import Partners in India’s Pharma Machinery Import

Despite the significant presence of domestic players in the industry, the Indian pharma machinery market is still largely dependent on imports. Challenges across multiple dimensions that were disablers to the growth of indigenous pharma machinery manufacturing in India need to be addressed. These include aspects around the macro economic environment, the pharma machinery ecosystem and, those specific to the pharma machinery industry.

Road Ahead

While the Government’s Make in India initiative is directionally right, its impact on improving access to affordable quality healthcare depends on how it is framed, developed and implemented over the next few months. A ‘step change’ is possible through collaborative transformation, with key levers being suitable policy initiatives, focus on fostering local innovation and making India a global hub for medical device manufacturing

Lab Equipment Industry of India:

The laboratory equipment market in India is expected to reach a projected revenue of US$ 3,348.0 million by 2030. A compound annual growth rate of 6.7% is expected of India laboratory equipment market from 2024 to 2030.

India laboratory equipment market highlights

The India laboratory equipment market generated a revenue of USD 2,126.7 million in 2023 and is expected to reach USD 3,348.0 million by 2030.

The India market is expect

The Indian laboratory equipment market demonstrates impressive sectoral diversity, with the general equipment segment commanding the largest revenue share at 26.91% in 2023. However, the support equipment segment is emerging as the fastest-growing category, indicating laboratories’ increasing focus on infrastructure modernization and operational efficiency.

- In terms of segment, general was the largest revenue generating product in 2023.

- Support is the most lucrative product segment registering the fastest growth during the forecast period.

Growth of Indian Laboratory Equipment Market

India’s significance in the global context cannot be understated. The country accounts for 7.1% of the global laboratory equipment market, and is projected to lead the Asia-Pacific regional market by 2030. This positioning reflects not only domestic demand but also India’s emerging role as a manufacturing and export hub for laboratory technologies. The laboratory automation sector specifically is experiencing even more pronounced growth, with the Indian market valued at USD 101.8 million in 2024 and expected to reach USD 203.8 million by 2033, exhibiting a CAGR of 7.62%. This acceleration is driven by healthcare infrastructure expansion, rising adoption of robotics, and the increasing need for high-throughput screening in drug discovery.

Government Policy to Support India’s Laboratory Sector

India’s laboratory sector transformation is significantly supported by comprehensive government initiatives. The Science and Engineering Research Board (SERB) provides crucial funding through multiple schemes, including the Core Research Grant (CRG), SUPRA scheme, and the innovative Fund for Industrial Research Engagement (FIRE) program, which facilitates 50% monetary fund matching between government and industry.

The Prime Minister Early Career Research Grant (PM ECRG) under the Anusandhan National Research Foundation (ANRF) represents a strategic investment in nurturing early-career researchers, while the SERB-POWER Research Grants specifically target women researchers, promoting diversity in scientific leadership.

Sector-specific initiatives further strengthen the ecosystem. The Food Safety and Standards Authority of India (FSSAI) has announced a Rs. 482-crore scheme for strengthening food testing infrastructure, focusing on state food labs, referral labs, and mobile food laboratories across all states and union territories.

Growth of Healthcare and Medical Device Industry

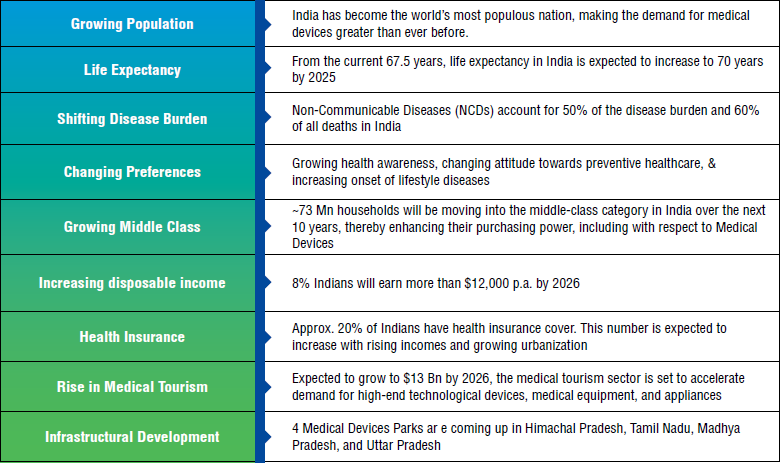

The Indian Healthcare and Medical Device Industry has been growing at double-digit rates and has evolved significantly in the last decade. The medical device market has been identified as a sunrise sector by the Government of India (GOI). The size of the Indian medical devices market is estimated at Rs. 90,000 crore (US$ 11 billion) in 2022 and is expected to grow to US$ 50 billion by 2030 with a CAGR of 16.4 %. The Indian medical device market share in the global market is estimated to be 1.65%. India is the fastest growing medical devices market amongst the emerging markets. It is the 4th largest Asian medical devices market after Japan, China, and South Korea, and among the top 20 medical devices markets globally. Between 2020-30, the diagnostic imaging market is likely to expand at a CAGR of 16.4%. The export of medical devices sector has been growing at a CAGR of 9-11% over the last 5 years. India’s expected export of medical devices will reach ~ $10 bn by 2025.

The medical devices sector has also grown considerably during this period and plays a critical role at each stage of the healthcare continuum. The Government of India’s ‘Make in India’ initiative presents a platform for the sector to revisit the operating model, identify key imperatives for growth and explore possibilities for creating a step change in the medical devices sector. However, there is still a huge gap in the current demand and supply of medical devices in India, as India has an overall 70-80% import dependency on medical devices. At present, many medical device manufacturers (domestic and international) are chasing this massive under penetration of medical devices in India as a significant growth opportunity.

India, with its ambitious National Medical Device Policy 2023, is poised to become a global leader in the manufacturing and innovation of medical devices. This forward-thinking policy sets out a comprehensive roadmap to achieve a 10-12% share in the expanding global market over the next 25 years.

What is a Medical Device?

A medical device is an instrument, apparatus, implant, machine, tool, in vitro reagent, or similar article that is to diagnose, prevent, mitigate, treat, or cure disease or other conditions, and, unlike a pharmaceutical or biologic, achieves its purpose by physical, structural, or mechanical action but not through chemical or metabolic action within or on the body.

Classifications:

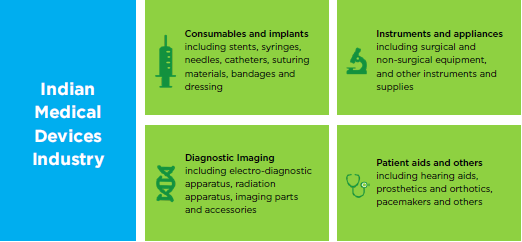

The medical devices industry comprises of five segments:

- Electronic Equipment: pacemakers, defibrillators, drug-releasing pumps, hearing aids, etc.

- Surgical instruments: Cutting instruments, grasping instruments and retractors used during surgery

- Consumables and disposables: stents, syringes, needles, catheters, suturing materials, bandages and dressing

- IVD Reagents: In vitro diagnostics (IVDs) are tests that can detect disease, conditions and infections

- Implants: dental implants or other body implants

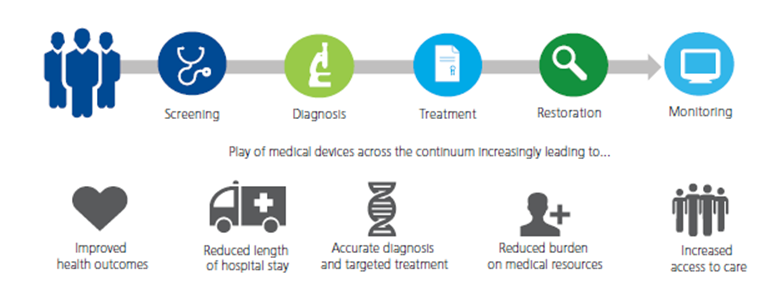

The various components of medical devices sector area follows:

a. Screening and Diagnosis: To increase the accuracy and cope with the complexity of screening methods. Nee for point of care/portable diagnostic devices increasing

b. Treatment/ care: Use of advance equipment enabling solution to critical and complex cases

c. Restoration: Physiotherapy and Rehabilitation centres are using advance assistive and rehabilitative devices for better service

d. Monitoring: Use of advanced devices to monitor patients effectively and even remotely

Indian Medical Devices Industry viz-a-viz Global Medical Devices Industry

The global medical devices market size was valued at $512.29 billion in 2022 & is projected to grow from $536.12 billion in 2023 to $799.67 billion by 2030, exhibiting a CAGR of 5.9% during the forecast period. North America accounted a maximum share with a market value of US$ 196.2 billion during 2022.

Globally the industry is controlled by a handful of enterprises. Among the top 30 companies in 2020, more than 60 percent (19) belong to USA followed by 4 firms from Japan, 3 from Germany, 1 each from Switzerland, UK, Sweden, and Netherlands and together they command around 58 percent of the global medical device market in 2020. It is interesting to note that 19 of the top 30 medical device companies in the world belong to USA and together they contribute about 42 per cent of the overall market. Overall, USA continue to remain the largest medical devices market globally.

Scenario of Global Clusters: Clusters Medical device firms are many a times operating in clusters. This is necessitated due to the various cross-functional support required by the units, including the presence of hospitals and doctors for conceptualizing and testing and quality raw materials. USA has over ten clusters. Europe too has a number of medical device clusters in Germany Netherlands, France, Italy, Switzerland, etc. India has over ten clusters. Medical devices clusters are also present in Japan, China, South Korea, Brazil, Australia etc.

Government Initiatives

The Government of India has commenced various initiatives to strengthen the medical devices sector, with emphasis on research and development (R&D) and 100% FDI for medical devices to boost the market.

- The Union Cabinet approved the National Medical Devices Policy, 2023 on April 26, 2023. The National Medical Devices Policy, 2023 is expected to facilitate an orderly growth of the medical device sector to meet the public health objectives of access, affordability, quality, and innovation. The policy is expected to help the Medical Devices Sector grow from the present US$ 11 billion to US$ 50 billion by 2030.

- Under the PLI scheme for Medical Devices, till now, a total of 26 projects have been approved, with a committed investment of Rs. 1,206 crore (US$ 147 million) to enable growth and innovation in the MedTech industry and make India as the global hub for manufacturing and innovation in the coming years.

- In September 2022, the government of India approved the setting up of an export promotion council for medical devices, under the Department of pharmaceuticals, with its headquarters in Noida.

- In August 2022, the Department of Pharmaceuticals greenlit the “Promotion of Medical Device Parks” programme from FY21-25 with a total financial investment of Rs. 400 crore (US$ 48.97 million), with a maximum support under the programme of Rs. 100 crore (US$ 12.24 million) for each Medical Device Park.

- In the Union Budget 2022-23, Rs. 86,200 crore (US$ 11.3 billion) was allocated as a budget for the pharmaceutical and healthcare sector.

- To boost domestic manufacturing of medical devices and attract huge investments in India, the department of pharmaceuticals launched a PLI scheme for domestic manufacturing of medical devices, with a total outlay of funds worth Rs. 3,420 crore (US$468.78 million) for the period FY21-28.

- There is a huge gap in the current demand and supply of medical devices in India and this provides a significant opportunity for manufacturing devices in India. At present, many medical device manufacturers (domestic and international) are chasing this massive under penetration of medical devices in India as a significant growth opportunity.

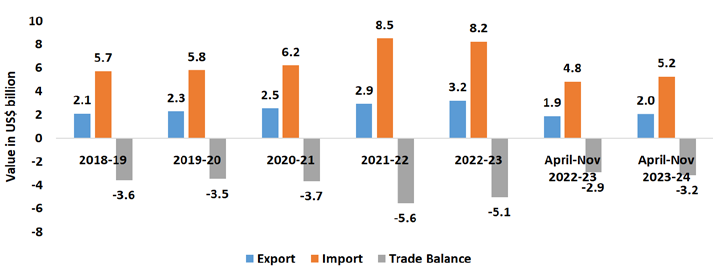

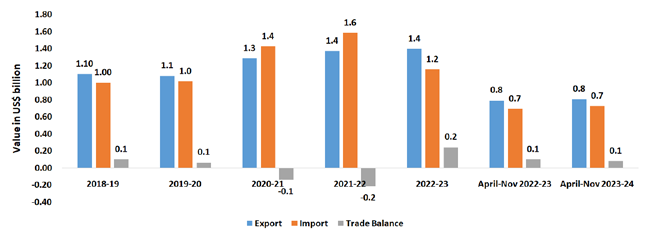

Trade Scenario of Indian Medical Devices Sector

Figure 1: Overall Trade data for India’s Medical devices Sector (in USD Bn.) during last five fiscal as well as current fiscal

Source: DGCI&S

Observation: The above figure depicts India’s overall trade scenario in medical devices segment for the last 5 years as well as during the current fiscal 2023-24. From the figure it is evident that both exports and imports of medical devices in India increased during the last 5 years. However the CAGR in Exports has increased by 11 percent whereas Imports increased by 10 percent during the last 5 years. Thus despite an outweighing increase in exports, India has a heavy negative trade balance in this sector which is evident even in its various components as in indicated below:

Category-wise export and import of medical devices in India

The below two tables indicate category-wise export and import of medical devices from India for the last 5 years as well as during the current fiscal

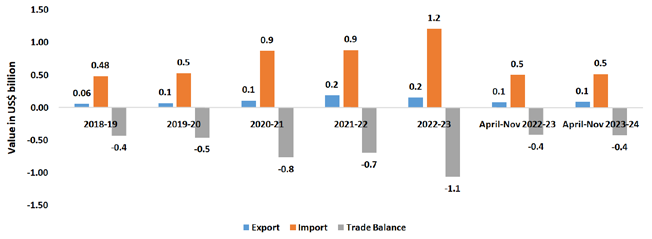

a) Electronic Equipment

Figure 2: Trade Scenario for Electronic Equipment Segment (in USD bn.)

Observations: From the above figure it is noted that while exports grew at 11.3 percent CAGR, imports at the same time of electronic equipment increased in India in the last five years at 8.3 percent CAGR. Thus, India continued to have a negative trade balance in this segment.

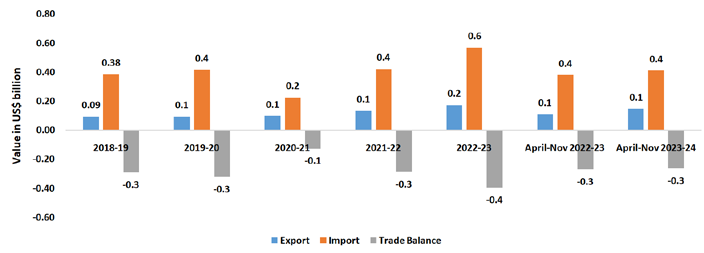

b) Surgical Instruments

Figure 3: Trade Scenario for Surgical Instruments Segment (in USD Bn.)

Observations: The above figure indicates that in the last five years while exports of surgical instruments grew by 11.9 percent, imports during that time increased by merely 2.3 percent. Inspite of this India continued to have a negative trade balance in this segment.

c) Consumables and Disposables

Figure 3: Trade Scenario for Consumables and Disposables (in USD Bn.)

Observations: In this segment, India’s exports in the last five years grew at a much higher rate (6.2 percent) compared to its imports (3.7 percent). While India had a positive trade balance between in 2018-19 and 2019-20, in 2020-21 and 2021-22 India’s trade balance in became negative, while the trade balance once again witnessed positive figures during 2022-23 as well as during the current fiscal April-Nov 2023-24.

d) IVD Reagent

Figure 3: Trade Scenario for IVD Reagents (in USD Bn.)

Observations: In this segment India’s exports (29 percent) rose at more than imports (25.9 percent). But even then India’s trade balance remained negative in the last five years as well as during the current fiscal.

e) Implants

Figure 3: Trade Scenario for Implants (in USD Mn.)

Observations: The above figure indicates that in the last five years while CAGR exports of implants grew by 17 percent, CAGR for imports during that time increased by only10.3 percent. Inspite of this India continued to have a negative trade balance in this segment too.

Country-wise Analysis

Figure 7: Share of Top export destinations for Indian Medical devices export (2022)

Observations:

- Figure 7 above depicts the top importers of medical devices from Indiaduring 2022. USA is the top importer from India importing with a share of 21 percent in India’s total medical devices exports.

- It is followed by UAE (6%), China (4.4%), Germany (4.2%)and Netherlands (3.5%) all of which have a share of 3 to 6 percent in India’s medical devices exports

- Together the top 5 export destinations account for more than 39 percent of India’s export basket

Source: ITC, Trade map

Figure 8: Share of Top export destinations for Indian Medical devices export (2022)

Source: ITC, Trade map

Observations:

- Figure 8depicts the top exporters of medical devices to India during 2022.

- USA is the top exporter to India exporting with a share of 17.7 percent in India’s total medical devices imports.

- It is followed by China (16.6%), Germany (10.4%), Singapore (10.4%), Netherlands (6.7%) all of which have more than 6 percent share in India’s import basket

- Together the top 5 import partners account for almost 62 percent of India’s import basket

Source: ITC, Trade map

High Import Dependency of the Medical Devices Sector in India

- The medical devices sector in India is dominated by small and fragmented companies and some very large multinational players. The multinational players account for most of the market share. Almost all of the top multinational players have their establishment in India. However, most of them import the products from their production base outside India for the Indian market thus contributing to India’s import dependency in this segment. The domestic manufacturers are restricted to low value added products which do not have sufficient export value.

- The table below depicts the potential segments of the Indian medical devices market denoting India’s import dependency in these segments as on 2022-23.

- In 2022-23, import dependency on equipment and electronics is very high on India’s imports of overall medical devices estimated to be close to 62%, while segments including disposables and consumables and IVD reagents has an import dependency of 14-15%. On the other hand, very low import dependency was witnessed in surgical instruments as in fact that the trade for the related sector is almost negligible.

Table 1: Medical devices segments with high potential and their import dependency

Table 1: Medical devices segments with high potential and their import dependency

| Key Segment | Percentage of import share in overall India's import of medical devices | Overall attractiveness for Indian Manufacturers to invest in this segment |

|---|---|---|

| Consumables & Disposable (C/D) | 14% | Medium |

| Electronic equipment (EL/EQ) | 62% | Very High |

| Implants (I) | 7% | Low |

| IVD reagent (IVD) | 15% | Medium |

| Surgical Instruments (SI) | 3% | Low |

Challenges across the sector: Medical Devices Industry

- Unfavourable duty structure

- Inadequate domestic demand for certain segments/product categories

- Lack of comprehensive laws and lax enforcement mechanisms for IP protection

- Absence of indigenous ‘quality certification’ authority

Medical Devices Ecosystem

- Inadequate ecosystem support

- Limited focus on ‘Innovate in India’

Macro Environment

- Ease of doing business

- Limited availability of skilled workforce and restrictive labor laws

- High cost of financing

Growth in Medical Devices:

Although the Indian market being largely dependent on imports ‘Local innovation’ by MNCs as well as domestic players is expected to drive indigenous manufacturing and lead to rapid growth of exports. India’s export of medical devices have grown at a rate of around 10.9% over the past five years, reaching a value of USD 3.2 billion in 2022-23. The sector has an enormous potential to become self-reliant and to contribute towards the goal of universal health care.

The Government of India has already initiated implementation of PLI Scheme for medical devices and support for setting up of 4 Medical devices Parks in the States of Himachal Pradesh, Madhya Pradesh, Tamil Nadu and Uttar Pradesh. Under the PLI scheme for Medical Devices, till now, a total of 26 projects have been approved, with a committed investment of Rs.1206 Cr and out of this, so far, an investment of Rs.714 Cr has been achieved. Underthe PLI scheme, total of 14 projects producing 37 products have been commissioned and domestic manufacturing of high-end medical devices has started which include Linear Accelerator, MRI Scan, CT-Scan, Mammogram, C-Arm, MRI Coils, high end X-ray tubes, etc. Remaining 12 products will be commissioned in near future. Five projects out of total 26 projects have been approved recently, under Category B, for domestic manufacturing of 87 products / product components.

Building upon these measures, a holistic policy framework to accelerate this growth and fulfil the potential of the sector is the need of the hour.

Major Achievements:

FDI: Foreign Direct Investment (FDI) FDI per annum increased from Rs 942 crores in 2014-15 to Rs 1545 crores in 2021-22. In between it saw two peaks in the years 2016-17 (Rs 3212 crores) and 2019-20 (Rs 2196 crores). The cumulative FDI during these years stood at Rs 11157 crores during 2014-15 to 2021-22. However, there was a quantum jump in FDI in 2022-23. FDI during the first three quarters of the year was Rs 2,798 crores. The cumulative FDI during the years 2014-15 to December 2022 stood at Rs 13955 crores.

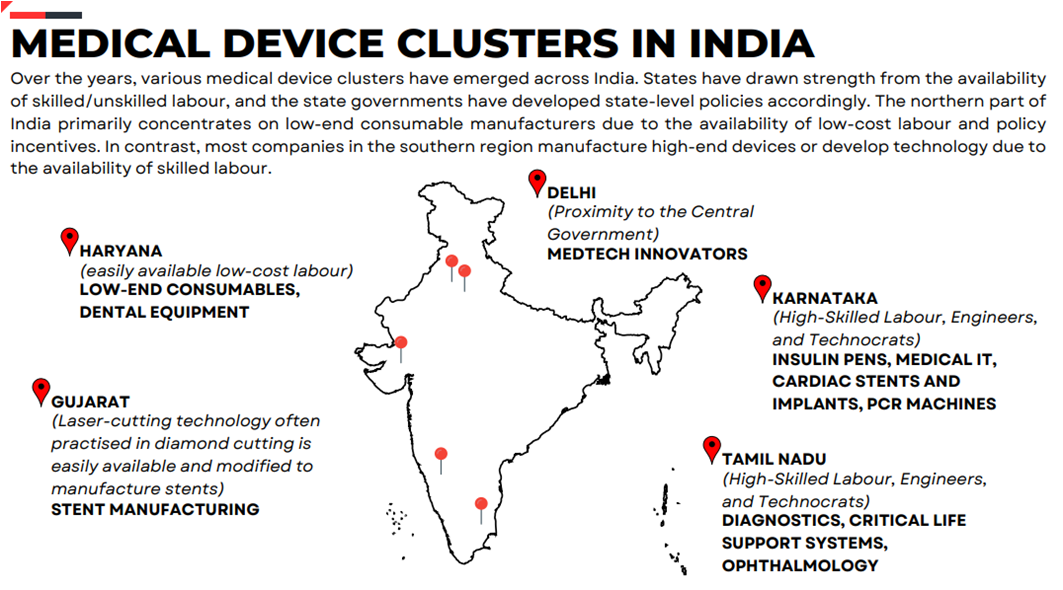

Clusters: Clusters and Parks 10 medical device clusters are present in Andhra Pradesh, Haryana, Gujarat, Karnataka, Tamil Nadu, Telangana, Maharashtra, and West Bengal. The Ahmedabad and Vadodara clusters in Gujarat manufactures a wide variety of implants, equipment, and disposables, with Surat cluster having most implant manufacturers. Faridabad cluster in Haryana produces an array of consumables and disposables. Bengaluru cluster in Karnataka majorly focuses on medical electronics. The Baruipur cluster in West Bengal specializes in manufacturing of surgical equipment. Implant and medical electronics manufacturers are clustered both in Chennai and Mumbai, with Mumbai cluster also having IVD and disposable production units. Both Hyderabad and Vishakhapatnam clusters manufactures a wide range of medical devices. Under the “Scheme for Promotion of Medical Device Parks” of the DOP, support of Rs 100 crore each has been approved for creation of common facilities in four medical devices parks in Uttar Pradesh, Tamil Nadu, Madhya Pradesh, and Himachal Pradesh.

Influence of High Impact Steps:

Also, as major schemes like Ayushman Bharat are making its presence felt through investment, need for machinery will increase. Schemes like PLI, Parks and above all the deep thrust and national interest of the Make in India effort will also necessitate more HR in medical devices.Also, as more doctors and nurses will get appointed, demand for medical devices will increase and so also the need for specialized staffs in different areas of medical devices.

© Copyright , All rights reserved. Design by Andreal