VOL. 19, ISSUE NO. 1 | April 2026

Oversight

FOR FEBRUARY 2026

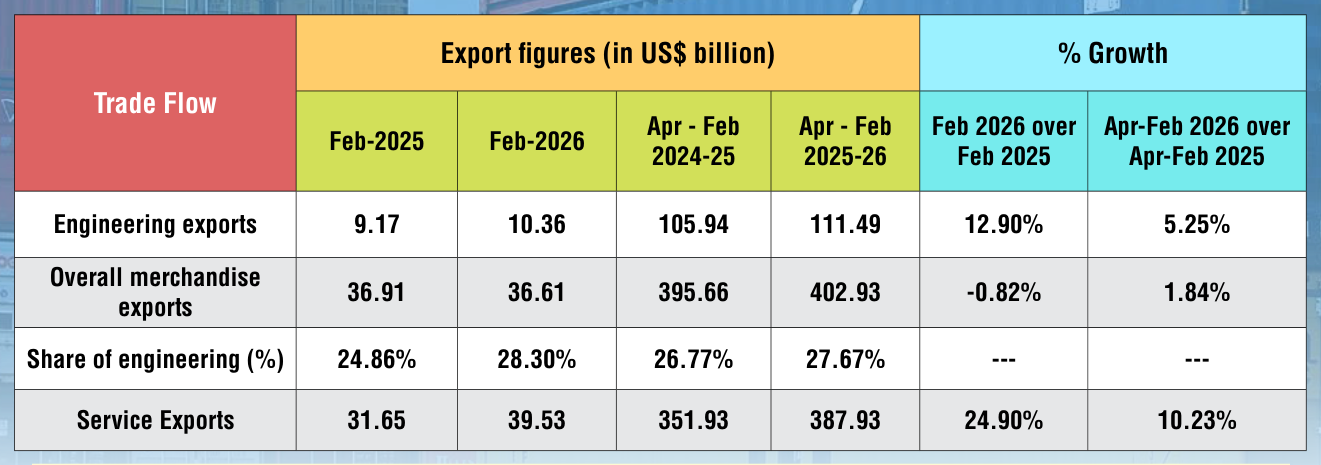

Engineering exports continued its growth run for the fourth straight month with double-digit year-on-year growth in February 2026

Source: Compiled from data by DGCI&S and Quick Estimates published by the Government of India.

After registering a marginal growth in the month of December 2025, India’s engineering exports recorded double-digit year-on-year (y-o-y) growth for the second month in a row to February 2026 and the overall growth-run is continued for the fourth straight month. The performance is quite impressive as engineering shipment from India was above USD 10 billion in the last four months despite of geo-political conflicts and economic slowdown in several regions of the world. During February 2026, India’s engineering exports achieved 12.9 percent y-o-y growth as it went up to USD 10.36 billion from USD 9.17 billion in February 2025. On a cumulative basis, engineering exports recorded a 5.25 percent growth in April-February 2025-26 when it surged to USD 111.49 billion from USD 105.94 billion during the same period last fiscal.After a record breaking figure in 2024-25, engineering exports from India is probably going to see another all-time high export figure in 2025-26. As per the quick estimates of the government, the share of engineering in total merchandise exports was recorded at 28.3 percent in February 2026 as against 28.5 percent in January 2026. The share was recorded at 27.7 percent on a cumulative basis during April – February 2025-26. The growth in engineering exports during the first eleven months of the current fiscal has mainly been driven by significant growth in exports of Metal and metal products, Machineries and Automotive. Among metals, Copper and products recorded a growth of 52.53 percent, Iron and steel recorded a growth of 11.54 percent, and aluminium and products recorded a growth of 2.61 percent. Industrial machinery registered a growth of 10.47 percent, and electrical machinery registered a growth of 7.9 percent.Within automotive, Motor vehicles and cars registered a growth of 24.72 percent. Region-wise analysis showed that North America continued to account for the largest share of Indian engineering exports with 20 percent share followed by EU at 18 percent, WANA at 15 percent, and ASEAN at 11 percent. During April-February 2026, exports to all regions recorded positive growth except WANA, Other Europe and CIS.

HIGHLIGHTS

- India’s engineering exports recorded double‑digit year‑on‑year (y‑o‑y) growth for the second month in a row to February 2026 and the overall growth‑run is continued for the fourth straight month.

- During February 2026, India’s engineering exports achived 12.9 percent y‑o‑y growth as it went up to USD 10.36 billion from USD 9.17 billion in February 2025.

- The performance of Indian engineering exports is quite impressive as it remained above USD 10 billion in the last four months to February 2026 despite of geo‑political conflicts and economic slowdown in several regions of the world.

- On a cumulative basis, engineering exports recorded a 5.25 percent growth in April‑February 2025‑ 26 when it surged to USD 111.49 billion from USD 105.94 billion during the same period last fiscal.

- As per the quick estimates of the government, the share of engineering in total merchandise exports was recorded at 28.3 percent in February 2026 as against 28.5 percent in January 2026. The share was recorded at 27.7 percent on a cumulative basis during April – February 2025‑26.

- In February 2026, 27 out of 34 engineering panels witnessed positive year‑on‑year growth. While 7 engineering panels including IC Engines, Machine Tools, Aircraft and Spacecraft, Medical and Scientific Instruments, Cranes, Lifts and Winches, prime mica and project goods witnessed year‑on‑year decline in exports.

- On a cumulative basis too, 27 out of 34 engineering panels recorded growth and remaining 7 engineering panels including Nickel and its products, Aircraft and Spacecrafts, Ships, boats and floating structures, hand tools and cutting tools, Medical and Scientific Instruments, Prime mica and project goods recorded negative growth during April‑February 2025‑26.

- During April‑February 2026, all regions recorded export growth barring WANA (3.8% decline), Other Europe (4.2% decline) and CIS (5.4% decline).

- North America continued to account for the largest share of Indian engineering exports (20% share) followed by EU (18%), WANA (15%), ASEAN (11%) and North East Asia (8%).

- Country‑wise, USA continued to remain the top destination for Indian engineering exports in April‑February 2026 as it recorded an export of 17.77 billion. The y‑o‑y growth from USA is recorded at 2.9%.

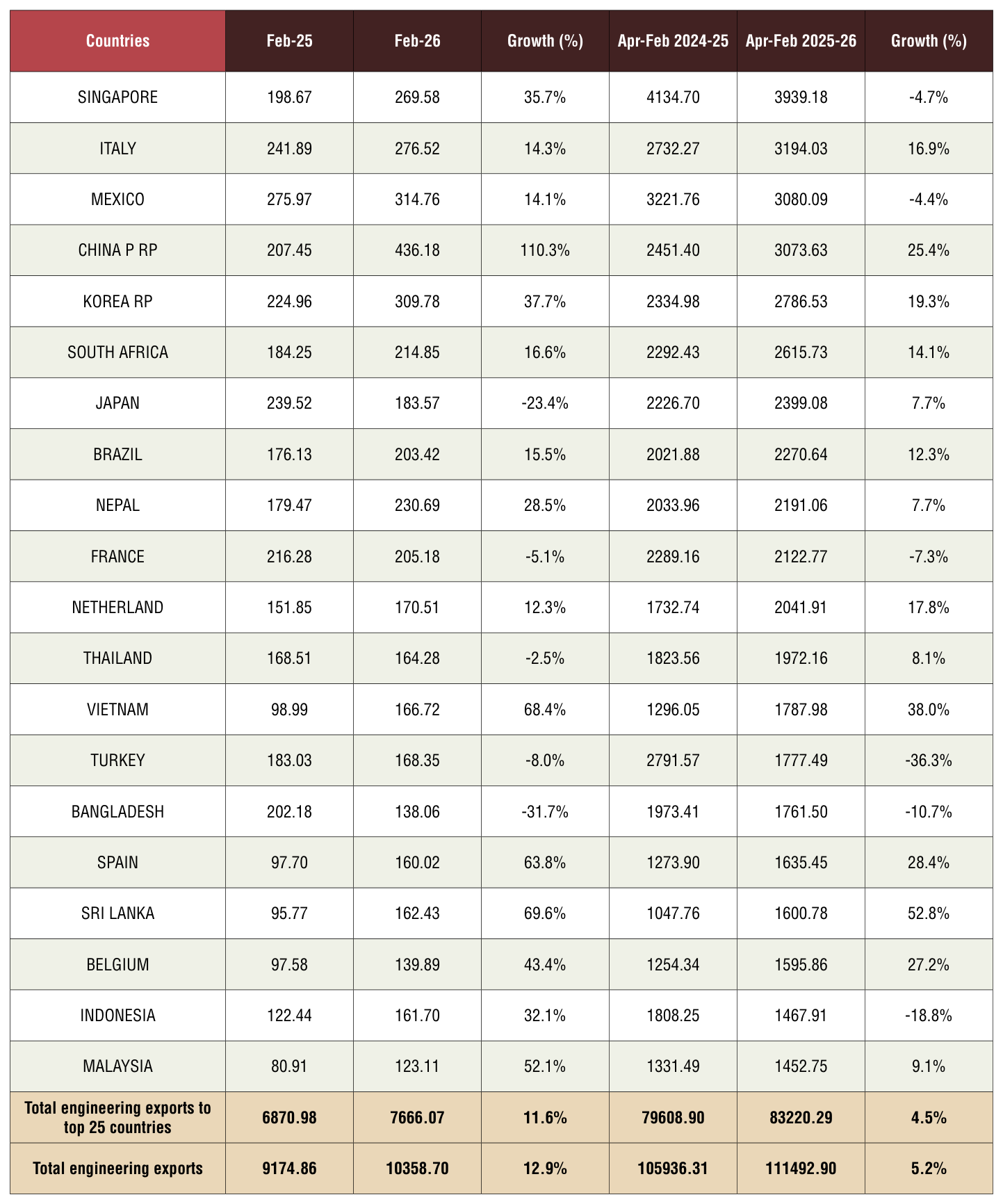

- Significant double‑digit export growth on a cumulative basis was noted in Vietnam (38%), China (25.4%), South Korea (19.3%), UK (20%) and European countries including Netherlands (17.8%), Italy (16.9%) and Spain (28.4%)

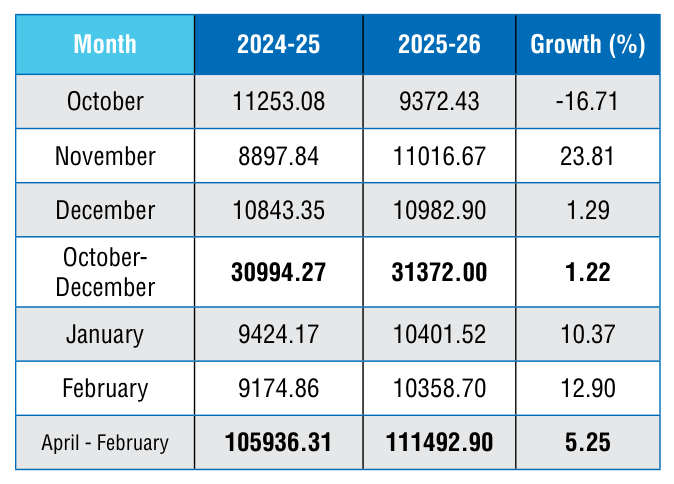

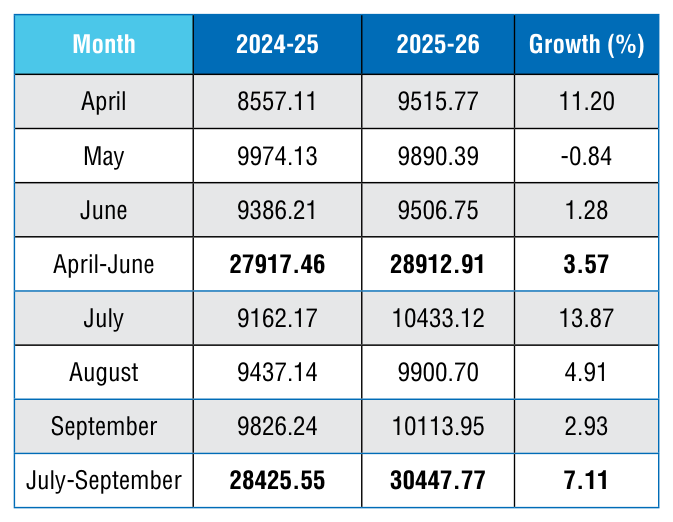

ENGINEERING EXPORTS: MONTHLY TREND

Source: DGCI&S, Govt. of India

The monthly engineering export figures for 2025‑26 vis‑à‑vis 2024‑25 are shown below as per the latest DGCI&S estimates:

Table 1: Engineering Exports: Monthly Trend in 2025-26 (Values in US$ million)

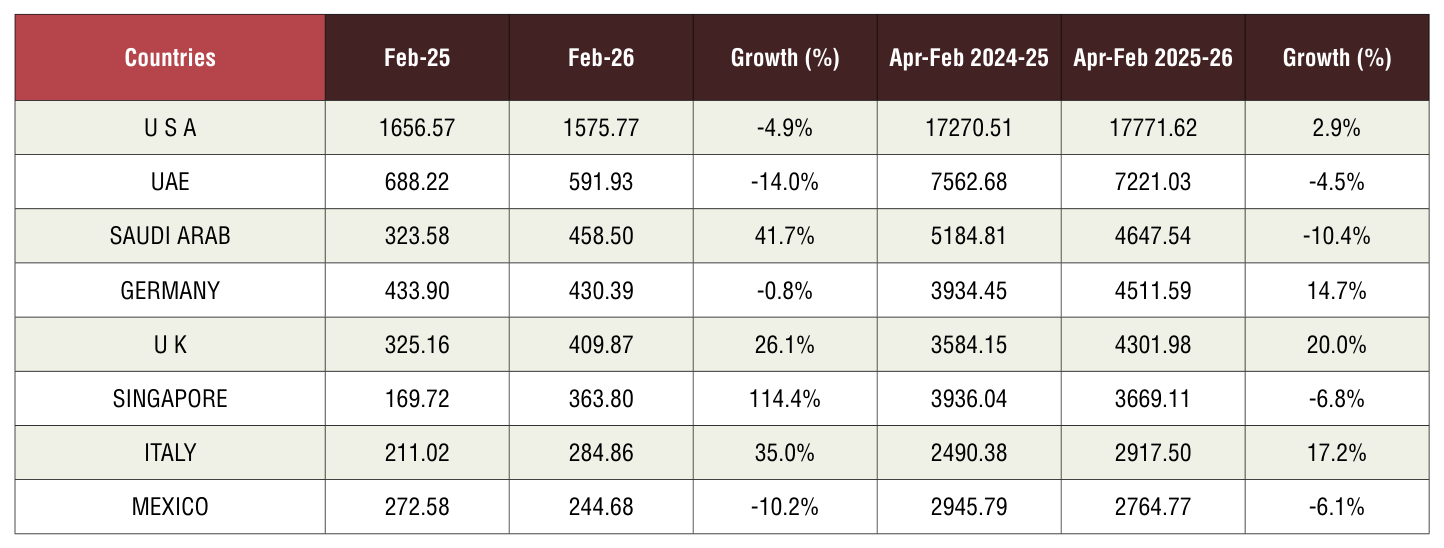

TOP 25 ENGINEERING EXPORT DESTINATIONS IN FEBRUARY 2026

We now look at the export scenario of the top 25 nations that had highest demand for Indian engineering products during February 2026 over February 2025 as well as in cumulative terms during April‑February 2025‑26 vis‑à‑vis April‑ February 2024‑25. The data clearly shows that top 25 countries contribute more than 74% of total engineering exports.

Table 2: Engineering exports country-wise (Values in US$ Million)

Source: DGCI&S

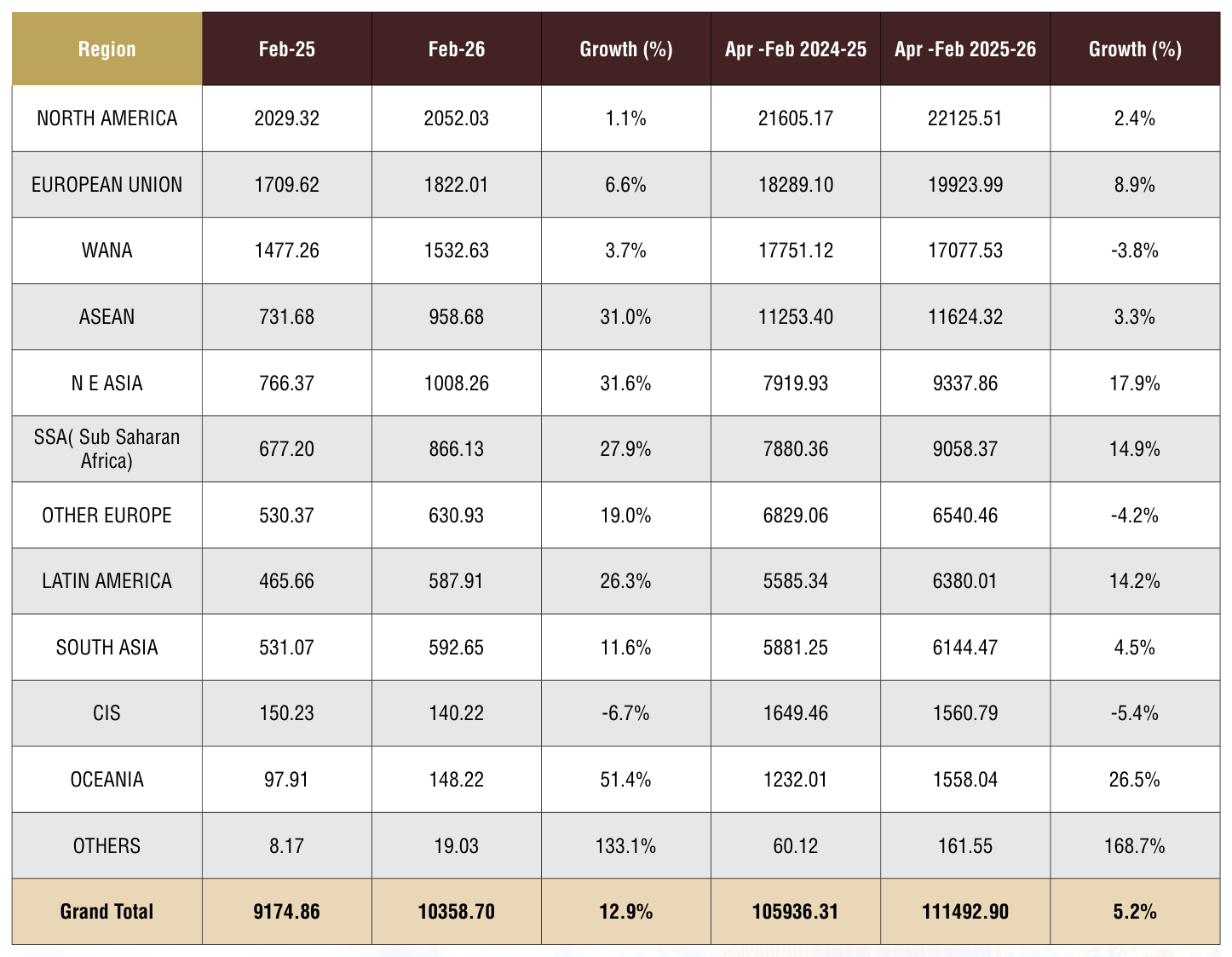

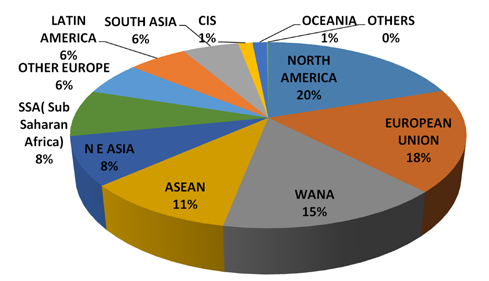

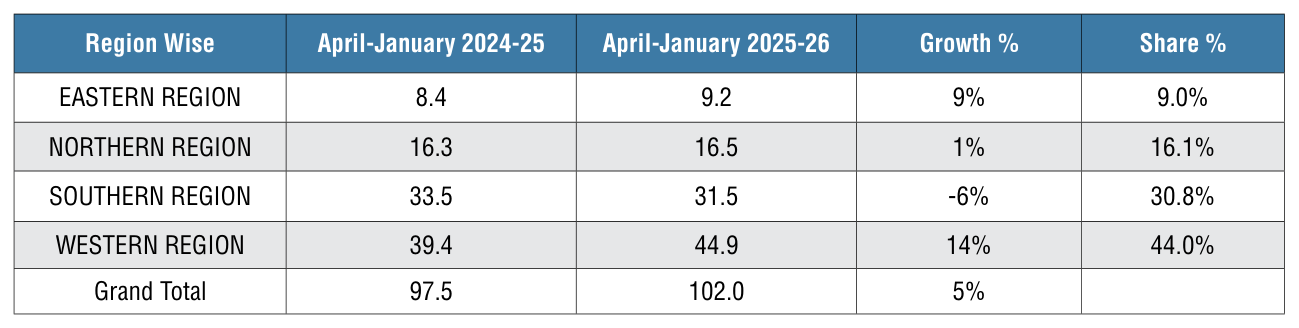

REGION WISE INDIA’S ENGINEERING EXPORTS

The following table depicts region wise India’s engineering exports for April‑February 2026 as compared to April‑February 2025

Table 3: Region wise engineering exports in April-February 2025-26 vis-à-vis April-February 2024-25 (Values in US$ Million)

Source: DGCI&S

Note: Myanmar has been included in ASEAN and not in South Asia, since ASEAN is a formal economic grouping.

Figure 1: Region-wise shares of India’s engineering exports during April-February 2025-26

Source: DGCI&S

Region-wise observations for April- February 2025-26:

- In April‑February 2026, all regions recorded export growth barring WANA (3.8% decline), Other Eu‑ rope (4.2% decline) and CIS (5.4% decline).

• WANA

- Also, it needs to be noted here exports in both WANA be‑ came positive in February 2026 – during this time, exports to WANA grew by 3.7%

- The West Asia Crisis has created serious disruptions for Indian ex‑ porters exporting to the WANA region – future exports to the region may get significantly affected

• Other Europe:

- The decline is mainly due to de‑ clining exports to Turkey – in April‑February 2025‑26, India’s exports to Turkey came down by 36% from USD 2.79 billion to USD 1.77 billion

- Needs to be noted here, in February 2026, exports to Other Europe became positive – this is due to significant export growth to the UK especially since the FTA. In April‑February 2025‑26, India’s engineering exports to UK rose by 20% from USD 3.5 billion to USD 4.3 billion

• CIS:

- The decline in exports to the CIS region is mainly due to decline exports to Russia, the largest export destination in the region. Apart from the issue with sanc‑ tions, depressed domestic de‑ mand in Russia is also another reason for declining exports

- Other observations:

- North America continued to ac‑ count for the largest share of In‑ dian engineering exports (20% share) followed by EU (18%), WANA (15%), ASEAN (11%) and North East Asia (8%)

- Country‑wise, USA continued to remain the top destination for Indian engineering exports in April‑February 2026 as it re‑ corded an export of 17.77 billion. The y‑o‑y growth from USA is re‑ corded at 2.9%

- Decline in exports was majorly noted in UAE and Saudi Arabia – the decline can be attribut‑ ed to significant fall in exports of aircraft, spacecraft and parts (‑98%)

- Decline in exports was also not‑ ed in Mexico (‑4.4%), France (‑7.3%), Turkey (‑36.3%), Ban‑ gladesh (‑10.7%) and Indonesia (‑18.8%)

- The decline in Mexico can be explained by their recently an‑ nounced trade reforms under which tariffs on over 1,400 prod‑ ucts rose sharply—ranging from 5% to 50%—for imports from countries without a Free Trade Agreement (FTA) with Mexico effective from 1st January 2026

- The decline in Bangladesh can also be explained by recent tax reforms whereby Bangladesh has withdrawn the existing im‑ port duties on steel raw materi‑ als and replaced it with a com‑ bination of VAT and Advanced Income Tax (AIT) which has increased the effective tax bur‑ den on manufacturers using im‑ ported steel for further process‑ ing by upto 40%. Even in cases of products with zero customs duty, the additional duties in‑ crease the cost burden.

- Significant double‑digit export growth was noted in Vietnam (38%), China (25.4%), South Ko‑ rea (19.3%), UK (20%) and Euro‑ pean countries including Neth‑ erlands (17.8%), Italy (16.9%) and Spain (28.4%)

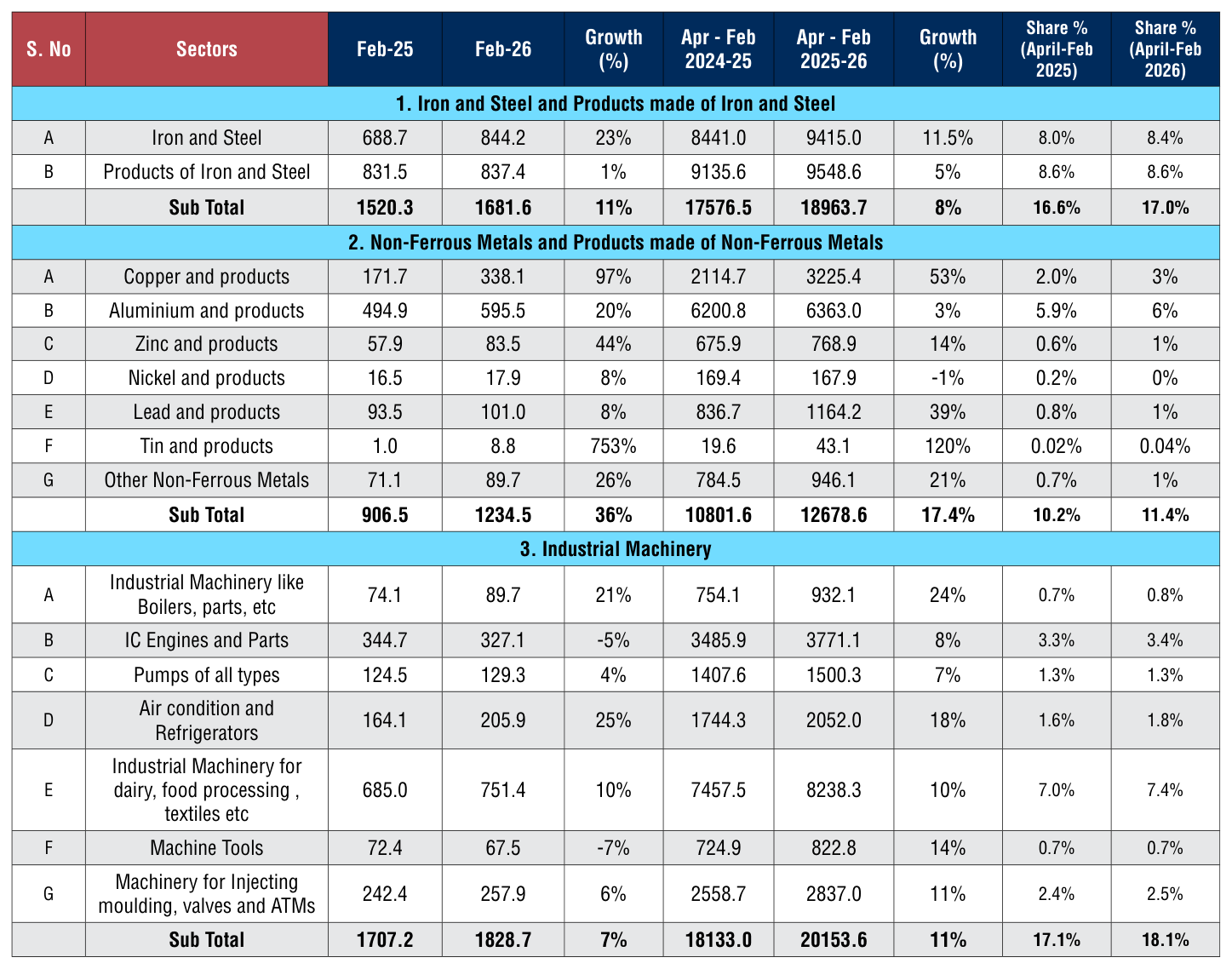

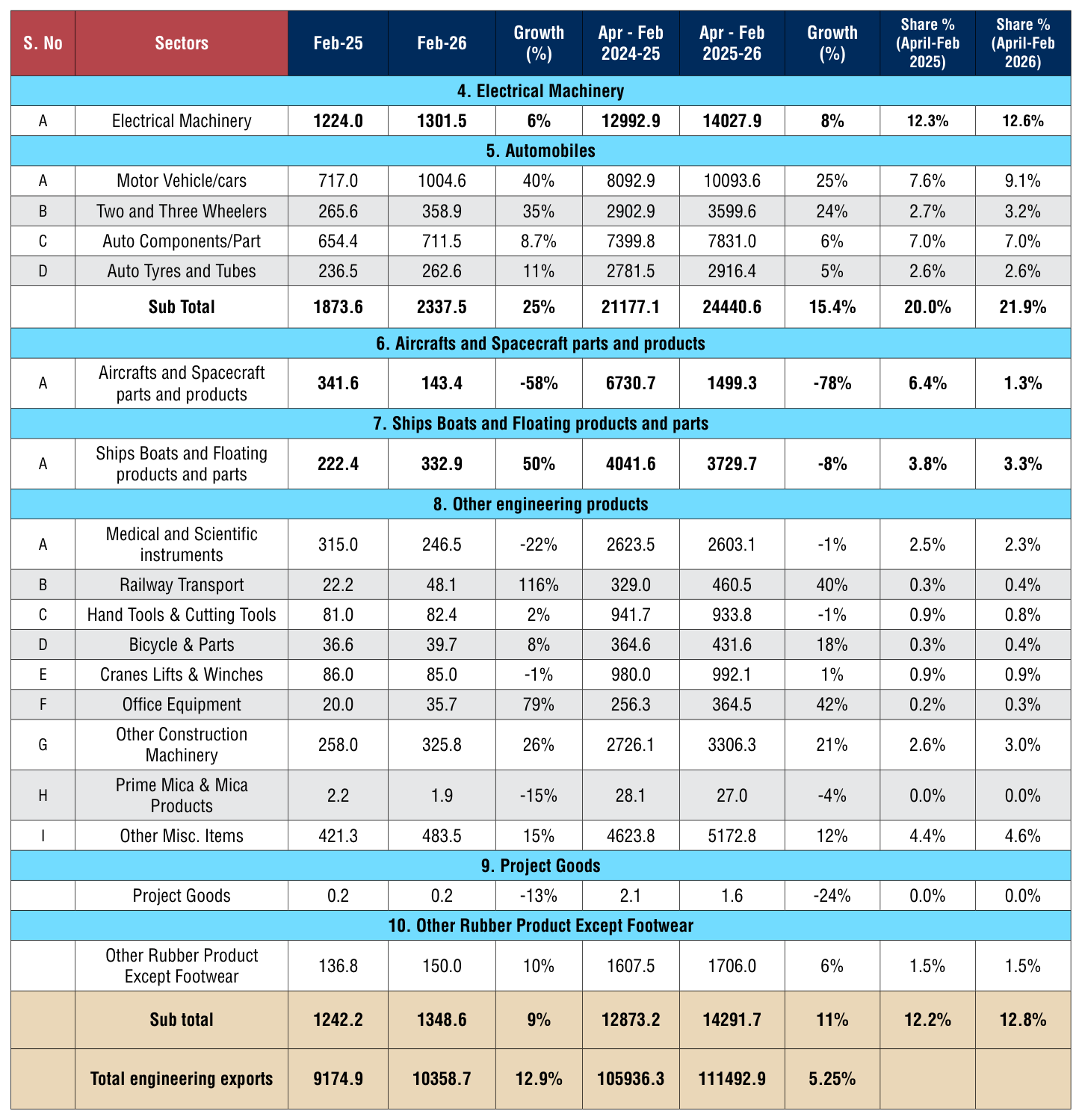

PANEL WISE INDIA’S ENGINEERING EXPORTS

The following table depicts region wise India’s panel wise engineering exports for April‑February 2026 as compared to April‑February 2025

- Table 4: Panel wise engineering exports in April-February 2025-26 vis-à-vis [US$ Mn] April-February 2024-25

Sectoral Observations:

India’s engineering exports grew by about 5.25% in April–February 2025‑26 to around US$111.5 billion, with mixed performance across panels:

I. Exports of iron and steel rose by 11.5% during April–February 2025 26, supported by higher shipments of primary steel, while products of iron and steel grew at a slower 5%. Overall, India’s steel exports rose 8% to US$18.96 billion during April–February 2025 26, supported by strong demand from the USA, UAE, EU markets (Italy, UK, Belgium, Germany, Netherland, Spain), Nepal and select WANA desti‑ nations (Saudi Arabia, Oman), Turkey from other Europe, etc.

As reflected in the Ministry of steel figures, India’s crude steel production rose sharply by 11.2% year on year during April‑Feb 2025‑26, supported by a 10.4% increase in finished steel pro‑ duction as well as 7.2% increase in finished steel consumption. Therefore consumption grew at a slower pace due todisrupted construction and infrastructure activity—the country’s largest steel consuming segments. The growth figures highlights In‑ dia’s resilience and continued strength in steel production de‑ spite global fluctuations.

b. The non‑ferrous metals pan‑ el emerged as a major growth driver, with exports rising by 17.4% to US$12.67 billion during April–February 2025 26. Among which,

i. Aluminium and aluminium products witnessed a growth of 3% to US$6.36 billion in April‑Feb 2026 from US$6.2 billion during April‑Feb 2025. Export performance was supported by stronger ship‑ ments to USA, Korea Rp, Viet‑ nam, China, Japan, Italy and Malaysia although declines were observed in markets such as Korea (Rep.), Mex‑ ico, Netherland and Turkey. On the pricing front, BigMint data indicates that domes‑ tic aluminium prices in India firmed up week‑on‑week, reflecting the rise in LME and MCX aluminium futures amid ongoing global supply concerns.Aluminium P1020 prices in India are expected to remain muted in the near term due to steady demand, moderated premiums, while global premium negotiations and easing LME volatility may continue to influence market sentiment.

ii. Copper and copper prod‑ ucts registered a robust 53% increase, rising to US$ 3.22 billion from US$ 2.11 billion. Export growth was sup‑ ported by strong demand from Saudi Arabia, China, USA, Korea (Rep.), the UAE, key EU markets,Malaysia and Nepal, although de‑ cline observed in Malaysia.

On the pricing front, BigMint data shows that India’s cop‑ per scrap imports fell 27% m‑o‑m in February 2026 from January 2026, mark‑ ing the lowest level in nearly a year. The decline could be attributed to holiday‑related slowdowns in major supply‑ ing countries, which tempo‑ rarily constrained shipments to India.Notably, with scrap availability tightening, Indian buyers shifted towards sourc‑ ing refined copper cathodes, resulting in a sharp increase in imports. India’s copper cathode imports doubled in February compared to that of January. Shipments from China surged, marking an in‑ crease of over 2,500%, mak‑ ing the country the largest supplier of cathodes to India this month. The surge was driven by competitive pric‑ ing from Chinese smelters amid ample domestic refined copper availability.End‑user demand is set to improve‑ from April, which could lift procurement of copper prod‑ ucts despite elevated freight and insurance costs. How‑ ever,if logistics costs remain high, Indian buyers maypre‑ fer sourcing copper cathodes if they are competitively priced.

iii. Lead and lead products rose significantly to US$1.16billion (+39%), while tin products expanded to US$43 million (+120%), albeit on a low base.

c. Exports of industrial machinery increased by 11% to US$20.15 bil‑ lion during April–February 2025 26, driven by strong demand for Industrial Machinery like Boilers, Air‑condition and Refrigeration machinery, Machine tools, re‑ flecting rising global investment in automation and manufactur‑ ing. However, exports of IC engines and parts grew only moderately.

d. Exports of electrical machinery grew by 8% to US$14.03 billion, supported by demand for pow‑ er equipment, switchgear, and transmission‑related products.

e. The automobile sector recorded robust growth of 15.4%, with ex‑ ports reaching US$24.44 billion, led by South Africa, Mexico,‑ Saudi Arabia, UAE, Japan, Bra‑ zil, Germany and Colombia and, reflecting sustained demand for vehicles and components. In South Asia, a strong rebound in Bangladesh, Sri Lanka and Nepal boosted exports. However, ship‑ ments to USA, Turkey and Indo‑ nesia decelerated

f. Exports of other engineering products rose by 11% to US$14.29 billion, supported by strong growth in office equipment, railway transport equipment, construction machinery, bicycle parts. In contrast, medical and scientific instruments witnessed a decline of 1% during April‑Feb‑ ruary 2025‑26.

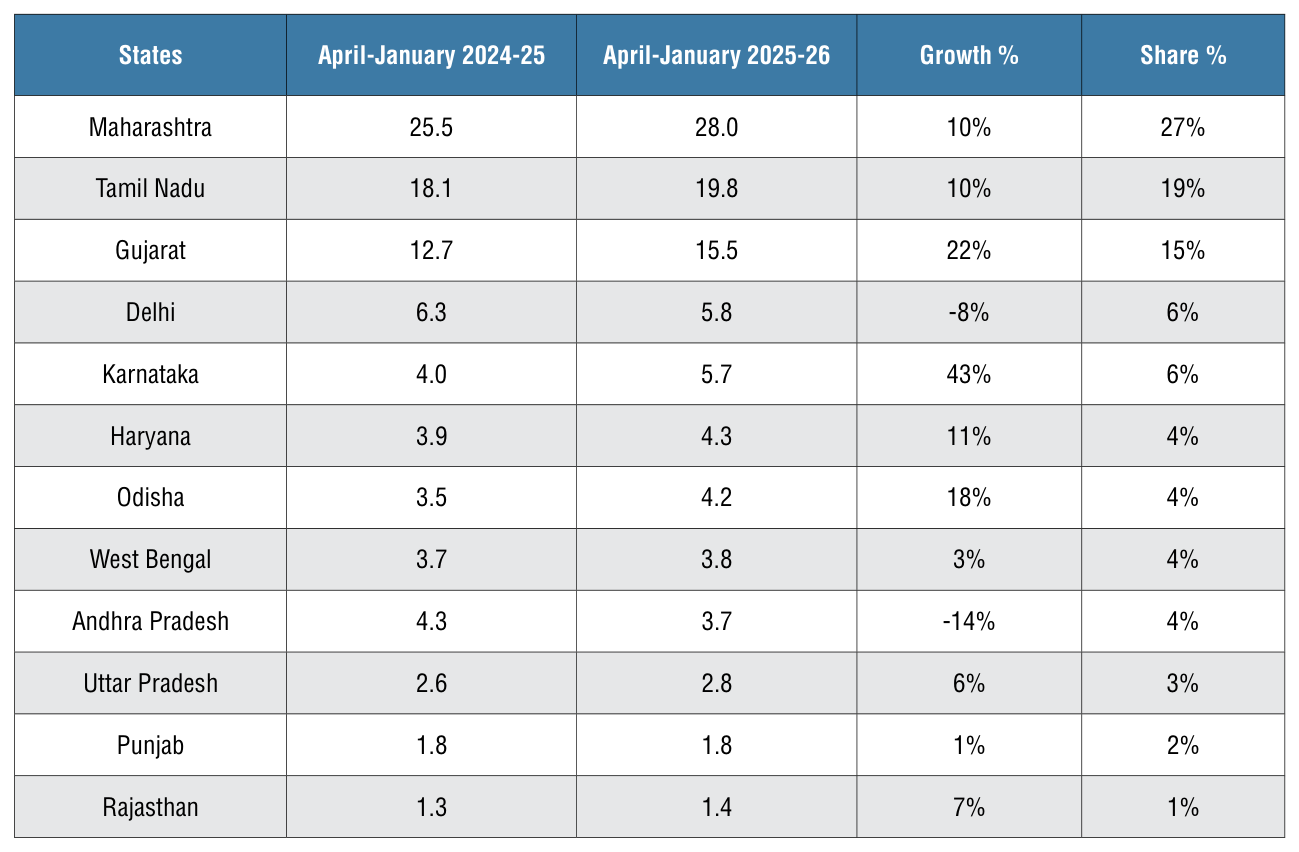

ENGINEERING EXPORTS – STATE-WISE ANALYSIS

State wise engineering export performance- Data as on 2025-26

Note: DGCI&S State figures are updated till the month of January 2026

The table below indicates the exports from top Indian states. It is evident from the table that almost 95% of India’s exports is contributed by the listed 12 states. Within this almost more than 60 percent of exports is done by Maha‑ rashtra, Tamil Nadu and Gujarat together during April‑January 2025‑26

Table 5: State Wise Engineering Exports (Value in US$ billion) (Value in US$ million)

Source: DGCIS Portal

Maharashtra leads with 28 billion USD in engineering exports (April‑ Jan 2025‑26), up by10% from 25.5 billion USD, securing a 27% national share through its robust ecosystem in engineering goods. West Bengal recorded marginal 3% growth reaching US$ 3.8 billion, holding a 4% share. Odisha achieved 18% growth to 4.2billion USD (4% share) during April‑January 2025‑26. Karnataka achieved the highest growth of 43% during April‑January2025‑26 reaching US$5.7 billion holding a share of 6%. Delhi contracted 8% to US$5.8 bn (6% share) and Andhra Pradesh fell 14% to US$ 3.7 bn (4% share), while Punjab was flat. Overall, growth remains concentrated in the western–southern hubs.

INDIA’S REGION WISE ENGINEERING EXPORTS

Table 6: Region Wise Engineering Exports (Value in US$ billion)

Source: DGCIS Portal

India’s region‑wise engineering exports (DGCIS) rose approximately 5% to US$102 bn in Apr–Jan 2025 26, led by the Western Region at US$44.9 bn (+14%, 44% share), which more than offset a contraction in the Southern Region to US$31.5 bn (–6%, 30.8% share). The Northern Region inched up marginally by 1% to US$16.5 bn (16.1% share), while the Eastern Region posted steady growth of 9% to US$ 9.2 bn (9% share). Overall, exports remain highly concentrated in the West and South (~75% share), with the West acting as the primary growth engine this period.

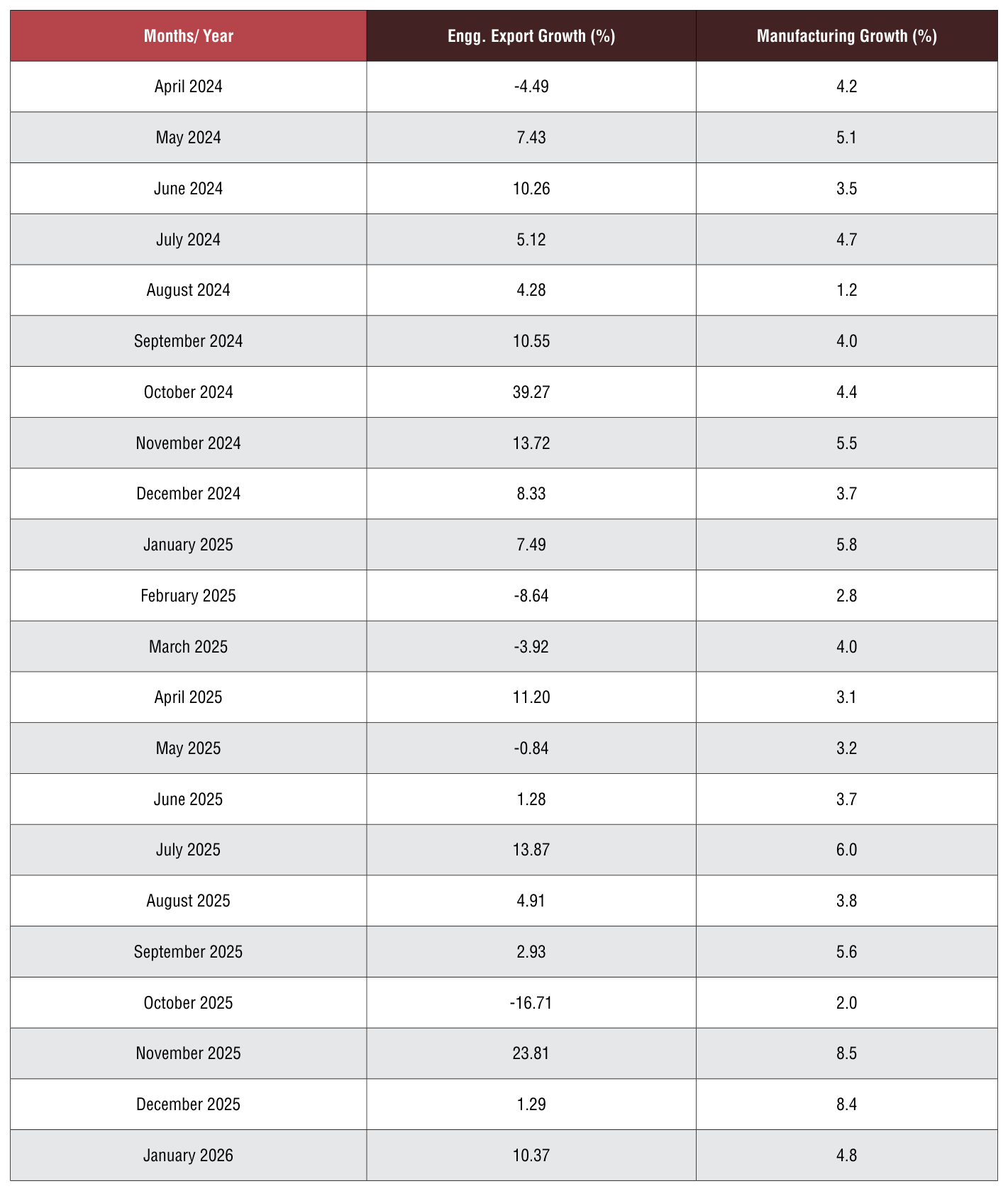

CORRELATION BETWEEN MANUFACTURING OUTPUT AND ENGINEERING EXPORTS

Engineering forms a considerable part of the broader manufacturing sector and the share of engineering production in overall manufacturing output is quite significant. As exports generally come from what is produced within a country, some correlation between manufacturing production growth and engineering export growth should exist. We briefly look at the trend in manufacturing growth as also engineering export growth to see if they move in tandem. It may be mentioned that manufacturing has 77.63% weightage in India’s industrial production.

Engineering export growth and manufacturing output growth moved in the same direction in as many as nine out of twelve months in each of the fiscal years 2019-20 and 2020-21. During fiscal 202122, engineering export growth and manufacturing growth moved in the same direction in seven out of twelve monthswhile in each of fiscal 2022-23 and 2023-24, as many as 10 out of 12 months saw engineering exports and manufacturing output moved in the same direction. In 2024-25, both moved in the same direction in eight out of 12 months.

The first two month of fiscal 2025‑ 26 saw engineering export growth and manufacturing output growth moved in the opposite direction. In April, engineering export growth surged to double digit and manufacturing growth decelerated, while in May engineering export declined and manufacturing output growth inched up over the month. Then, In June, July and August 2025 however, both moved on the same direction. In June and July, both witnessed improvement in growth while in Aug 2025, both conceded moderation in growth. In September 2025 however, engineering growth continued to slowdown but manufacturing growth accelerated. Both engineering growth and manufacturing growth moved in the same direction during October to December 2025. October 2025 saw both going down with decline in engineering exports while Novbemebr 2025 witnessed surged in both with substantially higher growth. In December 2025 however, while engineering exports grew, the growth rate slowed down whereas the manufacturing growth rate was maintained. The month of January 2026 however saw scceleration in engineering export growth but moderation in manufacturing output growth.

The link between these two may not be established in one or two months, but a positive correlation may be seen if medium to long term trend is considered.

Table 7: Engineering exports growth vis-à-vis manufacturing growth from April 2024

Source: Department of Commerce and CSO

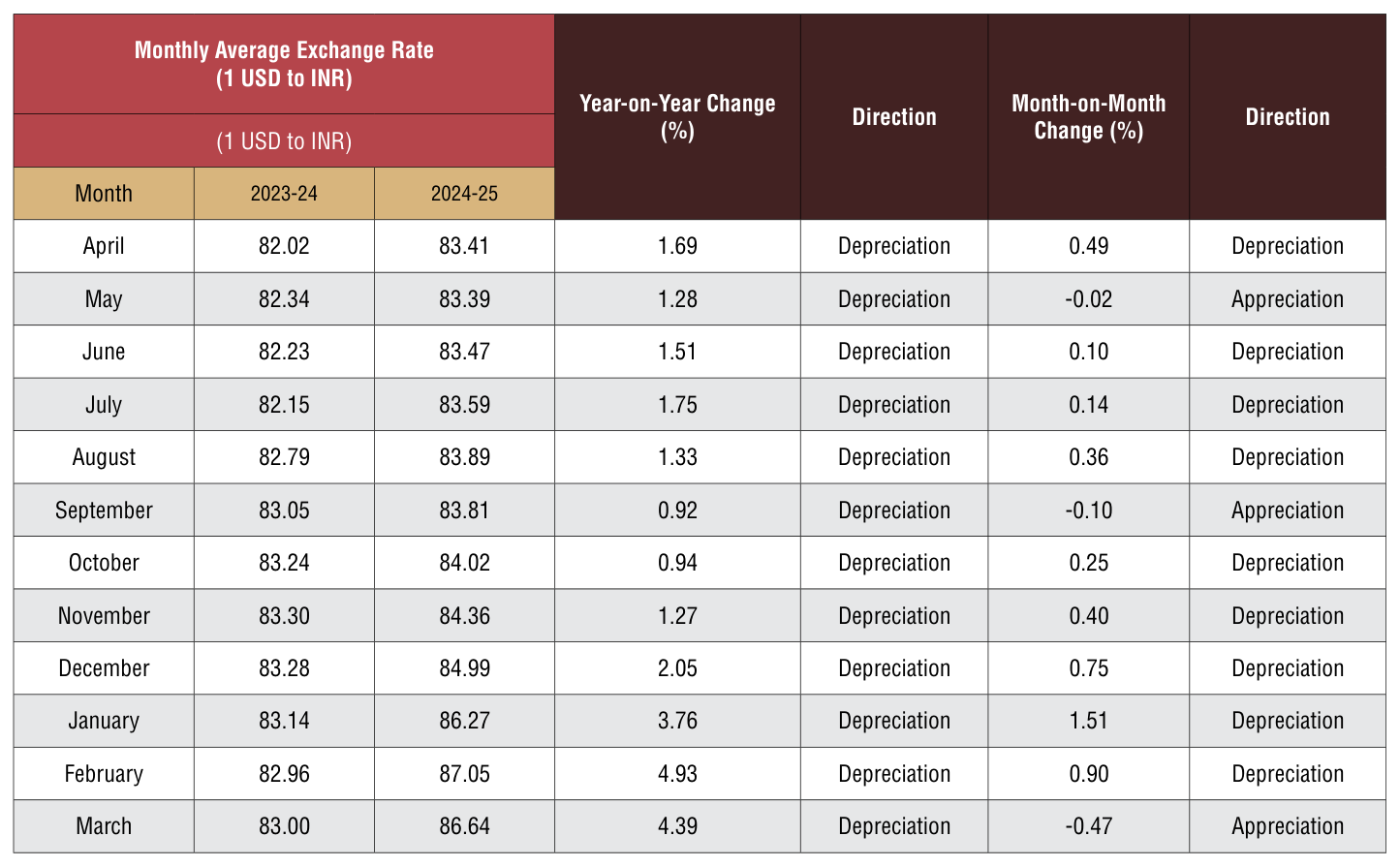

IMPACT OF EXCHANGE RATE ON INDIA’S EXPORTS

How did the exchange rate fare during February 2026 and what was the recent trend in Re-Dollar movement? In order to get a clearer picture of the recent Re-Dollar trend, not only we took the exchange rate of February 2026, but also considered monthly average exchange rate of Rupee vis-à-vis the US Dollar for each month of fiscal 2023-24, 2024-25 and fiscal 2025-26 as per the latest data published, as mere one-month figure does not reflect any trend. The following two tables clearly depicts the short-term trend.

Table 8: USD-INR monthly average exchange rate in 2025-26 vis-à-vis 2024-25 (As per latest data released by FBIL)

Indian Rupee continued to remain below 90 per US Dollar but remained stable over the month for the first time after May 2025: The Indian rupee ended February 2026 with a very feeble appreciation over the previous month butdepreciation continued vis-à-vis the US Dollar for the ninth straight month to February 2026. After a downfall to record low, rupee witnessed significant boost over the greenback with the announcement of a bilateral trade deal on February 3, 2026 that included reducing import tariffs of Indian goods to 18 percent from 50 percent. However, War between Iran and US-Israel and subsequent closure of strait of Hormuz strengthened dollar and rupee weakened again towards the end of February 2026.

Table 9: USD-INR monthly average exchange rate in 2024-25 vis-à-vis 2023-24 (As per latest data released by FBIL)

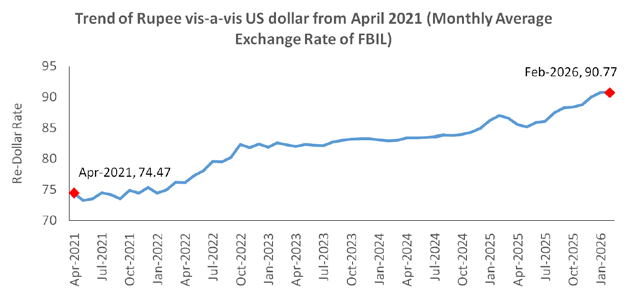

Fig 2: Trend of Rupee vis-a-vis US dollar from April 2021 (Monthly Average Rate of FBIL has been considered)

ANALYSIS OF INDIA’S ENGINEERING IMPORTS

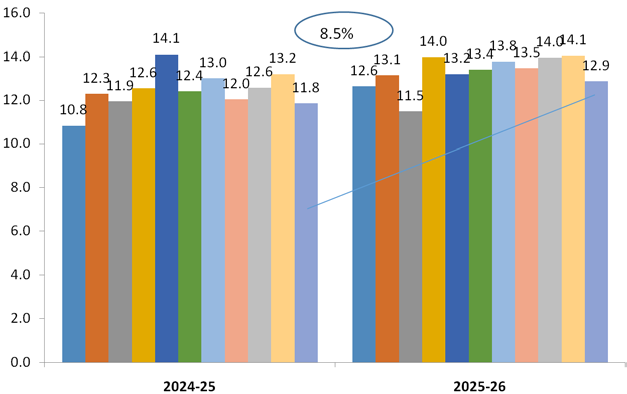

- India’s Engineering imports during February 2026 were valued at US$ 12.9 billion compared to US$ 11.8 billion in February 2025 registering a positive growth of 8.5 percent in dollar terms. In cumulative terms (Apr-Feb 2026), India’s imports increased by 9.4 percent.

- In February 2026, imports increased sharply for Two and Three Wheelers ,Copper and its products along with increase in, Other Construction Machinery, Aluminium and its products, Electric machinery &equipments, Industrial Machinery for dairy, Medical & Scientific and etc.

- In February 2026, import increase was mainly noted from NE Asia ,ASEAN, WANA, SSA(Sub Saharan Africa), South Asia, Latin America and Others. In cumulative terms, imports increased from all regions barring North America, Oceania and Latin America.

- The share of engineering imports in India’s total merchandise imports in Apr-Feb 2026 was estimated at 21 percent.

- 41.7 % of India’s engineering imports come from N E Asia and 21.0 % from the EU. The next major suppliers are ASEAN (12.6%), North America (7.6%) and WANA (7.1%) during Apr-Feb 2026.

Fig 3: Monthly Engineering Imports for April-February 2025-26 vis-a-vis April-February 2024-25

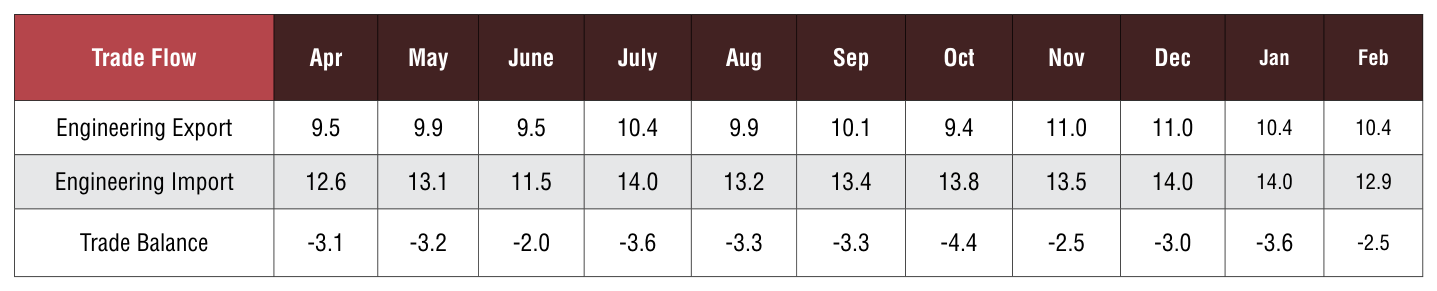

TREND IN ENGINEERING TRADE BALANCE

We now present the trend in two-way yearly trade for the engineering sector for the 2025-26 depicted in the table below:

Table 10: Monthly Trend in Engineering Trade Balance for the current FY 2025-26 (Values in US$ Billions)

Source: DGCI&S, EEPC India Analysis

CONCLUSION:

Indian engineering exports continued its growth journey in February 2026 as it recorded 13% growth. In cumulative terms, the growth is recorded at 5.2%. This is a silver lining at a time as the global trade faces serious disruptions due to growing geopolitical issues affecting logistics including shipping routes, freight costs and supply chains. The recent conflicts noted in the Hormutz Straits, a very significant maritime route carrying almost a quarter of global seaborne oil trade and significant volumes of liquefied natural gas and fertilizers has been a cause of significant concern for the exporters. Exporters have complained of escalating financial burdens including War-risk surcharges, high insurance premiums, extraordinary levies that escalating freight cost. Apart from that energy prices have skyrocketed and even in many cases exporters have faced critical raw materials shortage. The UNCTAD in a recent statement has specifically mentioned that the impact of the shock corroborate that of the earlier trends including COVID-19 pandemic. Let me also take this opportunity to thank the Government of India who has recently launched the RELIEF Scheme to alleviate the pain faced by exporters due to the West Asia crisis. We are hopeful of the continued government support in future to help in the growth journey of the industry

WEST ASIA CRISIS

IMPACT ON INDIAN ENGINEERING EXPORTS IS LARGELY NEGATED BY A SUPPORTIVE GOVERNMENT

The War between US-Israel and Iran, started in Feb 2026, have deeply impacted the global trade by disrupting the supply chain as Iran closed the Strait of Hormuz waterway between the Persian Gulf and the Gulf of Oman, which is strategically one of the most important passage for global trade, especially for export of Oil & Gas from the middle-east countries to the rest of the world. This critical global maritime chokepoint handles roughly 20% to 25% of the world’s total seaborne oil trade. As of 2025, approximately 20 million barrels of oil and significant volumes of liquefied natural gas (LNG) and fertilizers pass through this waterway daily, making it crucial for global energy supply.

Economic impact on India

- Sharp rise in energy prices: Usually, net importers of oil and gas have been suffering the most due to the Iran War and subsequent closure of the Strait of Hormuz. India imports around 80% of its crude oil requirement while for Natural gas and LPG, the import is around 50% and 60% respectively. A significant share of these imports are traded through Hormuz Straight. Increase in energy price therefore, is the major adversity being faced by Indian industries. In addition, costlier shipping, possibility of output drop, high inflation and financial-market pressure are also being counted as the result of West Asia crisis. Price of Brent crude rose from the pre-war level of USD 65/bbl to USD 110/bbl as on 16th April 2026.

- Shipping & Logistics Disruptions: Key trade routes through the Strait of Hormuz are experiencing severe disturbances, leading to stalled shipments to Gulf nationswith substantial amounts of cargo stranded at ports.

- Shipping cost gone up exorbitantly: Container shipping lines raising rates by as much as 40% in most cases to compensate for rising fuel costs and higher insurance premiums. The combination of base increases, ECS (emergency conflict surcharge) and war-risk surcharges are real burden for the exporters.

- Weakening of local currency: Surge in import price following higher energy prices and uncertainty on economic stability following the war weighed on Indian rupee that depreciated to a level of 93.5 per USD by the end of March 2026. India’s forex reserves also dropped from a record high USD 728.5 billion in the week ended 27th February to USD 697.1 billion as on 3rd April, keeping pressure on India’s current account.

- High inflation: As oil and gas is a major constituent of production across industries, sharp rise in prices of oil and natural gas will lead to inflation. According to an RBI research paper, a 10% increase in global crude oil prices can raise India’s headline inflation by approximately 20 basis points (0.20%) on a contemporaneous basis.

- Decline in exports: India’s merchandise exports dropped by 7.44% in March 2026 to USD 38.92 billion, the steepest year-on-year drop in five months. Exports to the Middle East plunged by nearly 58 percent in that very month, with further challenges expected in April due to ongoing logistical disruptions arising from the West Asia crisis. Trade deficit however eased as imports also declined.

Measures adopted by the Government

The Indian government has been quick to realize the concern of the Indian exporters and have adopted a series of quick measures to compensate the exporters and keeping the pace of India’s export intact. Following are some of the steps taken by the government:

- Launch of RELIEF Scheme

- The government introduced the Resilience & Logistics Intervention for Export Facilitation (RELIEF) scheme with an approved outlay of Rs. 497 crores to offset extraordinary freight costs, war-risk insurance premiums, and logistics disruptions caused by the crisis.

- Implemented by ECGC, the scheme consists of three components. It provides up to 100% risk coverage, enhances insurance for upcoming shipments, and gives MSMEs partial reimbursement for freight costs.

- The scheme covers consignments destined to countries in the region such as United Arab Emirates, Saudi Arabia, Kuwait, Israel, Qatar, Oman, Bahrain, Iraq, Iran and Yemen and also to Egypt and Jordan.

- Restoration of RoDTEP rates and extension of RoDTEP scheme: Rates under RoDTEPhave been restored that have reduced in Feb 2026. In addition, the scheme has been extended till 30th September 2026.

- Extension in the export obligation period of specified Advance Authorisation and EPCG authorisations till 31.08.2026: This relief applies to authorizations where the original or extended EO/block-wise period expires between March 1 and May31,2026.

- Facilitating return of export cargo from international waters and similar situations to make them face least compliance burden: To facilitate the return of export cargo from international waters or foreign ports—particularly due to disruptions like the Strait of Hormuz closure—the Central Board of Indirect Taxes and Customs (CBIC) in India has implemented temporary, streamlined procedures. These measures are designed to minimize compliance burdens, such as eliminating the need for formal re-import duties and reducing documentation.

- Operationalization of InterMinisterial group (IMG) for supply chain resilience: The government has constituted an Inter-Ministerial group (IMG) for supply chain resilience. The IMG will monitor global developments affecting supply chain, assess the impact of crisis on exports and engage with stakeholders to take appropriate measures.

Outlook

Despite the crisis in West Asia that causes the most damaging supply chain disruption after the Pandemic, Indian engineering reached its new all-time high at USD 122.4 billion in 2025-26. While exports to directly crisis affected region declined, shipments to other regions expanded reflecting successful diversification strategy by the Indian government. The crisis once again demonstrated India’s inherent strength to wither any external shock and we believe that even if the crisis stays long or worsen, Indian exporting community will be able to shrug it off in the long run with the help of an immensely supportive government.

© Copyright , All rights reserved. Design by Andreal